Monthly Market Commentary : Stocks retreat on news from the Fed and China.

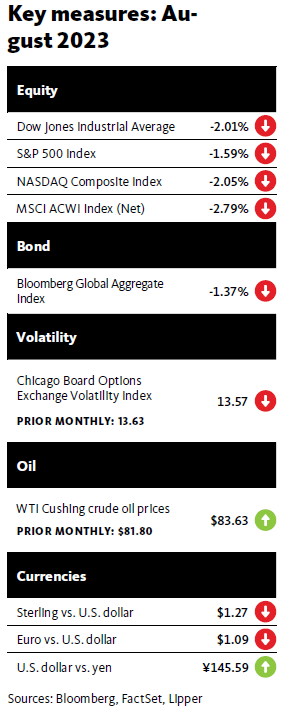

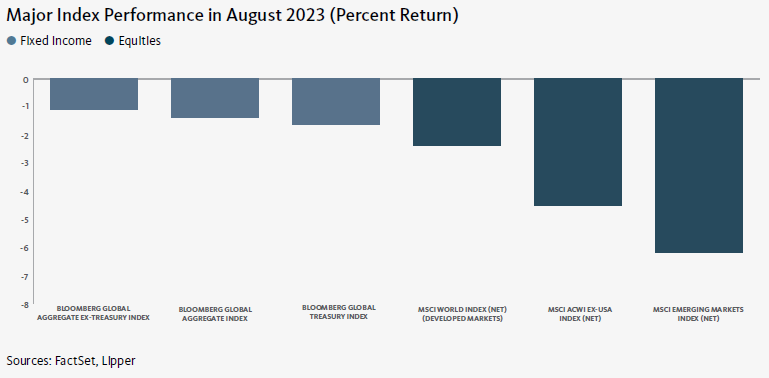

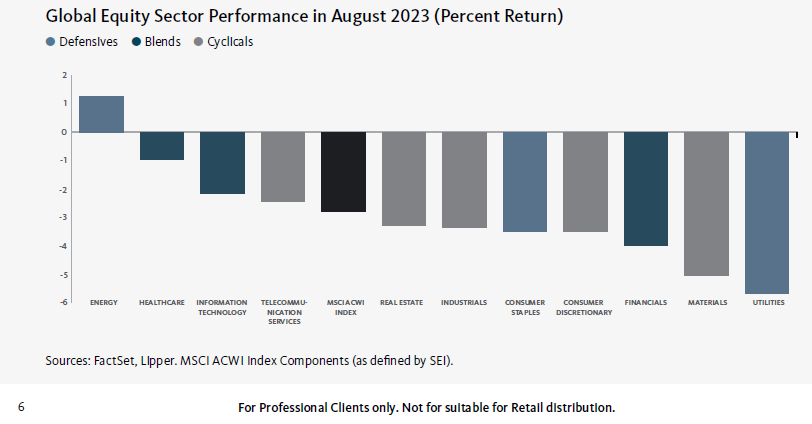

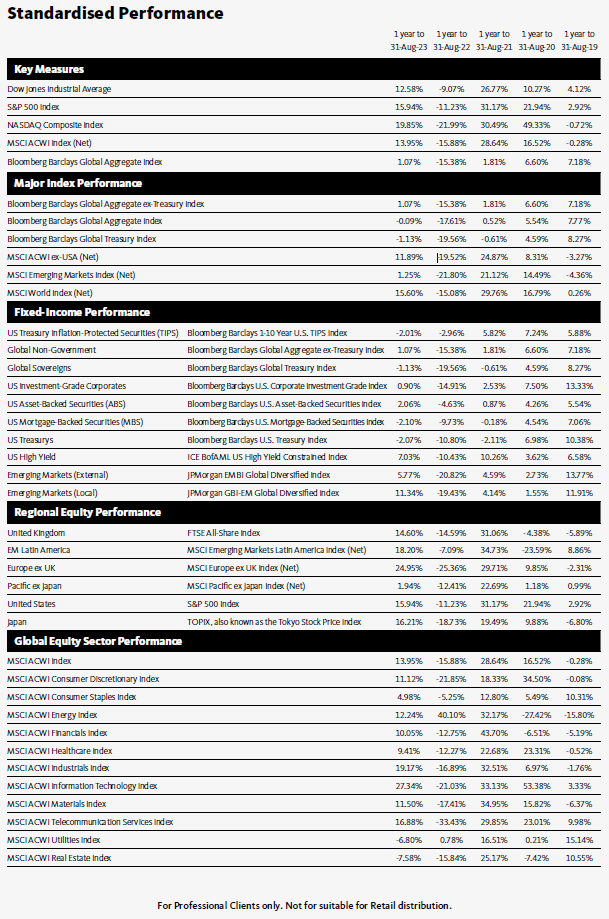

Global equity markets recorded losses in August–just the second monthly downturn thus far in 2023–due to investors' uncertainty regarding the direction of U.S. Federal Reserve (Fed) monetary policy, as well as worries about China's weakening economy. Developed markets outperformed their emerging-market counterparts during the month. The Nordic countries recorded comparatively smaller losses and were the top performers among developed markets in August, bolstered mainly by strength in Denmark. The Pacific ex Japan region was the primary market laggard due largely to significant weakness in New Zealand. Europe led the emerging markets during the month, benefiting from notable gains in Egypt and Turkey. Conversely, stocks in Colombia and South Africa experienced double-digit losses and were the weakest emerging-market performers in August.1

During a speech at the Kansas City Fed’s annual economic symposium at Jackson Hole, Wyoming, in late August, Fed Chair Jerome Powell reiterated the central bank’s goal of reducing the annual rate of inflation to 2%, and said that the Fed would consider additional interest-rate hikes if needed. Powell commented, “We are committed to achieving and sustaining a stance of monetary policy that is sufficiently restrictive to bring inflation down to [2%] over time.” He also noted that the central bank “will assess our progress based on the totality of the data and the evolving outlook and risks.”

China, the world’s second-largest economy, has recently experienced relatively weak credit growth, a downturn in exports, and a year-over-year decline in consumer prices. Lower demand for goods and services from Chinese consumers could have a negative impact on other countries’ exports of iron ore, crude oil, factory equipment, and luxury goods into the country. U.S.-based manufacturers of chemicals and heavy machinery have cautioned that they may experience a slowdown of sales in China. Additionally, a large property developer filed for protection under Chapter 15 of the U.S. bankruptcy code, which safeguards non-U.S. companies that are undergoing debt restructurings from creditors seeking to sue the firms or to freeze their assets in the U.S.

Most global fixed-income asset classes lost ground in August. However, U.S. high-yield bonds registered positive returns and were the top performers within the U.S. market for the period. 2 U.S. corporate bonds, mortgage-backed securities (MBS) and U.S. Treasurys declined.3 Treasury yields moved modestly higher in the intermediate and long segments of the curve, while the direction of yields was mixed in the short end (bond prices move inversely to yields). The yield on the 2-year Treasury note dipped 3 basis points (0.03%), and yields on 3-, 5-, and 10-year notes rose 0.03%, 0.05%, and 0.12%, respectively, in August. The spread between 10- and 2-year notes moved from -0.91% to -0.76% during the month, and the yield curve remained inverted.

Global commodity prices saw mixed performance in August. The West Texas Intermediate (WTI) crude-oil spot price and the Brent crude oil price gained 2.1% and 1.6%, respectively, in U.S. dollar terms, on expectations that production output cuts from the Organization of the Petroleum Exporting Countries (OPEC) would continue through the end of 2023. The gold spot price was down 4.1% for the month due to strength in the U.S. dollar. The New York Mercantile Exchange (NYMEX) natural gas price rose 5.1% in August, benefiting from forecasts for more hot weather in the U.S., which would increase demand. Wheat prices fell nearly 10% over the month due to Russia’s shipments of large quantities of cheaply priced grain.4

Economic data

U.S.

- According to the Department of Labor, the U.S. consumer-price index (CPI) rose 0.2% in July, matching the monthly increase in June. The CPI advanced 3.2% year-over-year—up modestly from the 3.0% annual rise in June, which was the lowest in more than two years. The government attributed the month-over-month increase in inflation to higher costs for housing and, to a lesser extent, motor vehicle insurance. Core inflation, as measured by the CPI for all items less food and energy, was up 0.2% in July, matching the rise in June, and advanced 4.7% over the previous 12 months.

- The Department of Labor reported that U.S. payrolls expanded by 187,000 in August, and the unemployment rate rose 0.3 percentage point to 3.8%. The health care and leisure and hospitality sectors added 71,000 and 40,000 jobs, respectively, during the month. In contrast, transportation and warehousing payrolls declined by 34,000 in August, while the information industry saw a loss of 15,000 jobs. Average hourly earnings rose 0.2% for the month and 4.3% year-over-year. The 12-month increase was slightly lower than the 4.4% annual rise in July.

U.K.

- According to the Office for National Statistics (ONS), consumer prices in he U.K. dipped 0.3% month-over-month in July—a sharp decline from the 0.6% increase in June. Inflation increased 6.4% over the previous 12-month period, down from the 7.3% annual upturn in June. Lower gas and electricity costs were the main contributors to the decrease in prices in July. Core inflation, which excludes volatile food prices, rose at an annual rate of 6.4% in July, unchanged from the year-over-year increase for the previous month.

- The ONS also reported that U.K. GDP grew 0.5% in June (the most recent reporting period), up from a 0.1% decrease in May, and increased 0.2% over the previous three-month period. Production output and the construction sector saw upturns of 1.8% and 1.6%, respectively, in June, versus corresponding 0.6% and 0.2% declines in May.

Eurozone

- Eurostat estimated that the inflation rate in the eurozone was unchanged at 5.3% for the 12-month period ending in August. Prices for food, alcohol and tobacco rose 9.8%, but the pace of acceleration slowed from the 10.8% annual rate in July. Energy prices decreased 3.3% year-over-year, following a 6.1% decline in July. Core inflation, which excludes volatile energy and food prices, rose at an annual rate of 5.3% in August, down 0.2 percentage point from July.5

- According to Eurostat’s second estimate, eurozone GDP grew 0.3% in the second quarter of 2023, improving from the flat growth rate in the first quarter, and increased 0.6% year-over-year. The economies of Ireland and Lithuania were the strongest performers for the second quarter, expanding 3.3% and 2.8%, respectively, while Poland’s economy contracted 3.7% during the period.

Central banks

The Fed’s next policy meeting is scheduled for September 19-20. Minutes from the Federal Open Market Committee’s (FOMC) meeting in July, which were released in August, revealed that the members remain focused on curbing inflation despite the steady downward trend in the U.S. personal consumption-expenditures (PCE) price index over the past year. Most committee participants maintained their belief that there are “significant upside risks to inflation, which could require further tightening of monetary policy.” However, several FOMC members expressed the view that the Fed should take a more measured approach, noting that, “with the stance of monetary policy in restrictive territory, risks to the achievement of the Committee’s goals had become more two-sided, and it was important that the Committee’s decisions balance the risk of an inadvertent overtightening of policy against the cost of an insufficient tightening.”

In a split 6-3 vote, the Bank of England (BOE) raised the Bank Rate by 25 basis points (bps) to a 15-year high of 5.25%. Two BOE members supported a 0.50% increase, while another favoured leaving the benchmark interest rate unchanged at 5.00%. In its announcement of the rate hike, the BOE noted that, while the overall inflation rate in the UK had slowed from 8.7% to 7.9% month-over-month in June, it remained well above the central bank’s 2% target. The BOE also commented, “Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance is restrictive. The [Monetary Policy Committee] will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including the tightness of labour market conditions and the behaviour of wage growth and services price inflation.

The European Central Bank’s (ECB) next monetary policy meeting is scheduled for September 14. The ECB increased its benchmark interest rate by 0.25% to 4.25% following its meeting in late July. The next monetary policy meeting for the Bank of Japan (BOJ) will be held on September 21-22. The central bank left its benchmark interest rate unchanged at -0.1% following its meeting on July 28. However, the BOJ set a rigid upper yield limit of 1.0% for the 10-year Japanese government bond (JGB). The 10-year JGB yield ended August at 0.65%. 6

SEI’s view

Economists have been spending much of their time this year arguing when or if economic growth, inflation, corporate profits, interest rates, and equities will peak. Optimists and pessimists alike have been confounded by the ebb and flow of the data and the gyrations of the financial markets.

In general, input-price inflation has decelerated significantly. Canada’s industrial product price index registered an outright decline in its price level, with a year-over-year change of -2.7% through July.7 The eurozone’s producerprice index (PPI) has witnessed the sharpest deceleration, falling from a peak year-over-year rate of 43% through August 2022 to a July 2023 reading of a 3.4% annual decline. By contrast, the improvement in producer prices has been less dramatic in Japan (still rising at a 3.6% year-over-year pace as of July). We believe that these year-over-year PPI inflation readings should continue to show improvement in the months immediately ahead owing to favourable base effects.

On a longer-term basis, we believe that demographic shifts are likely to keep labour markets tighter than has been the case at any point since the baby boomers–who were born between 1946 and 1964–first made their presence felt in the workforce in the 1970s. The new focus on supply-chain resiliency, reduced dependence on China as a manufacturing hub, the transition away from relatively cheap fossil-fuel energy to greener but more expensive sources of power, and the likelihood of significantly higher corporate taxes and financing costs in the years ahead, all suggest to us that inflation will tend to settle at 3% or more in advanced industrial economies instead of the previous norm of 2% or less.

Persistent inflation and ongoing labour-market tightness have forced most major developed-country central banks to keep raising their benchmark interest rates. The Fed, the Bank of Canada, and the ECB already have benchmark rates that match or exceed the peak recorded in 2008.8 We think it’s likely that the BOE will soon join this group. We continue to expect inflation to run structurally higher in the years ahead due to persistent labourmarket tightness, the need to increase the resiliency and diversity of supply chains, and the need to offset the depressive impact of higher taxes and financing costs on profit margins.

While U.S. equities experienced a downturn in August, the valuation in the market remains problematic. The price-to-earnings ratio of the broad-market S&P 500 Index had been on the rise this year, ending August at 18.6 times analysts’ estimated earnings for the next 12 months.9 The expansion in the price/earnings multiple on forward earnings for most of 2023 occurred despite the additional monetary tightening by the Fed and other central banks. The overall market also appears to be overvalued relative to today’s bond yields. If earnings experience a substantial contraction, history suggests that stock valuations also will fall.

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change. All information as of 31 August 2023.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments.

SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The views and opinions within this document are of SEI only and are subject to change. They should not be construed as investment advice.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document, Summary of UCITS Shareholder rights (which includes a summary of the rights that shareholders of our funds have) and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents.

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the “SFO”). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction.

The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents.