Monthly Market Commentary: Stocks celebrate Fed’s interest in slowing rate hikes.

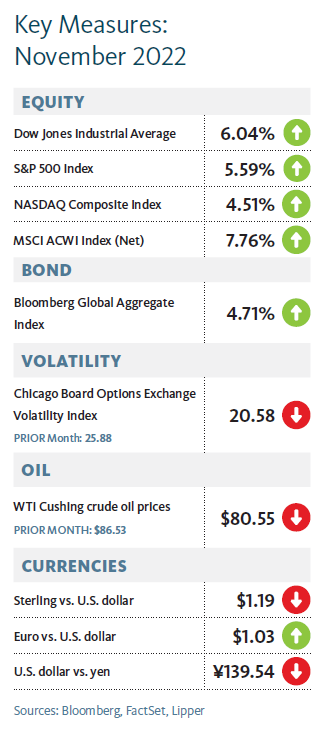

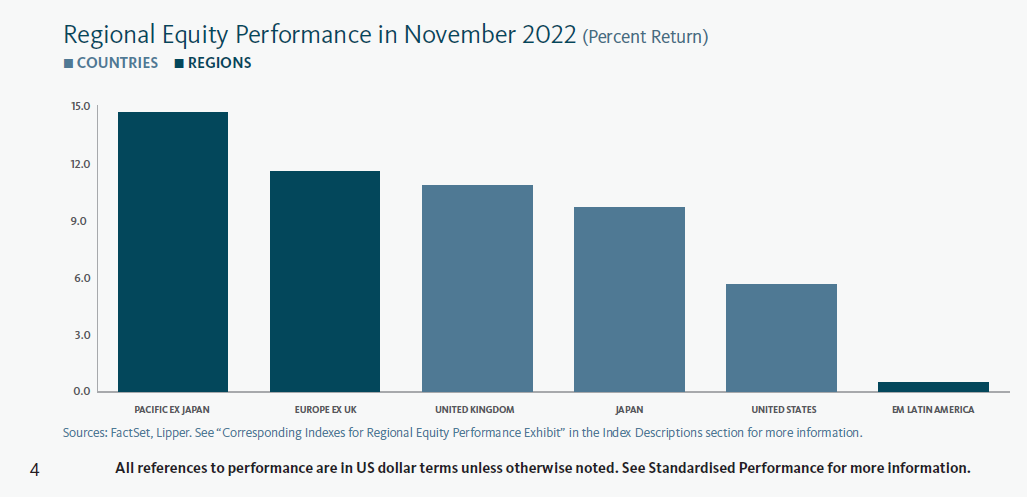

Most equity markets finished November in positive territory following a strong rally during the previous month.Emerging-market stocks outperformed their developed-market counterparts, led by mainland Chinese equities.2 Regionally, emerging markets in Asia and Europe generated the world’s strongest equity gains in November, while the Asia-Pacific region also performed well.3 Conversely, North America fared the worst due to notable losses in U.S. stocks.4

Yields on U.S. Treasury securities with maturities of two years or greater moved lower in November (yields and prices have an inverse relationship). However, the 2-to-10-year yield curve remained inverted (short-term rates exceed long-term yields) and widened by 0.29% to 0.70%. U.K. gilt yields declined in the intermediate and long segments of the curve but moved modestly lower for all maturities under three years during the month. Eurozone government bond rates decreased for all maturities of five years or greater, while yields rose for maturities of four years or less—thereby inverting the 2-to-10-year curve.

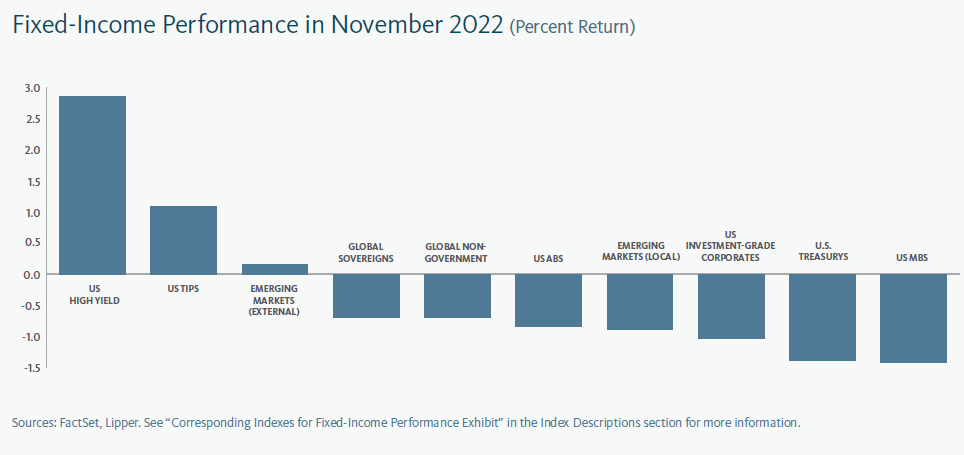

Fixed-income asset classes posted gains in November as intermediate- and long-term bond yields moved lower. U.S. investment-grade corporate bonds led the rally as investors turned to high-quality securities ; mortgage-backed securities (MBS) and U.S. Treasurys—the most rate-sensitive areas of the market—also garnered positive returns.5

Regarding the commodities market, Brent and West Texas Intermediate crude-oil spot prices were down in November by 6.3% and 6.9%, respectively, on fears that China may reinstate COVID-19 restrictions and trigger a decline in demand for oil in that country. The NYMEX natural gas price rose by 9.0% amid concerns that existing supply constraints caused by Russia’s ongoing aggression toward Ukraine will intensify once the colder winter weather sparks a surge in demand. Wheat prices decreased by 9.8% as Russia agreed to renew a deal brokered with the United Nations (UN), Ukraine, and Turkey that allows for the shipment of Ukrainian grain through the Black Sea, alleviating concerns about an international food shortage.6

Rishi Sunak faced his first domestic crisis as U.K. prime minister and Conservative Party leader just weeks after succeeding Liz Truss in late October, when tens of thousands of health care workers employed by the National Health Service (NHS) voted for industrial action. The Royal College of Nursing (RCN) trade union announced that nurses plan to strike on December 15 and 20—the union’s first such action in its century-long existence—over compensation, working conditions, and patient safety.7 This came as the U.K. government failed to meet their demands for pay increases of 5% over inflation (which surpassed 11% in October).8 Members of trade unions that represent ambulance workers—including emergency call handlers, technicians, and paramedics—voted to strike over similar issues.9 Negotiations with the unions have proven especially challenging given that U.K. Chancellor Jeremy Hunt is seeking to reduce the government’s £55 billion (roughly US$66 billion) deficit through drastic spending cuts. Under the government’s current deficit-reduction plan, a gross domestic product (GDP) growth rate of 2% would result in savings of approximately £23 billion (about US$27.6 billion) for the U.K. government by the 2027-to-2028 fiscal year.10

Ukraine’s military regained control of the southern city of Kherson as Russian Defense Mnister Sergei Shoigu ordered his troops to retreat from what had been the sole regional Ukrainian regional capital that Moscow held since invading earlier this year. This is a major setback for Russia’s Vladimir Putin.

Chinese President Xi Jinping’s administration faced anti-government demonstrations across the country in response to its zero-tolerance policy regarding COVID-19. Local police forces moved quickly to diffuse the protests,

which China’s National Health Commission (NHC) blamed on local governments; a spokesperson for the NHC stated that some local authorities “take a onesize- fits-all approach, and take excessive policy steps that have neglected the demands of the public.”11 Xi’s administration announced an initiative to accelerate vaccinations for elderly citizens in an effort to ease the COVID-19-induced restrictions.

In Latin America, Luiz Inácio Lula da Silva (Lula) of the progressive Workers’ Party won Brazil’s presidential election by a narrow margin over the conservative incumbent, President Jair Bolsonaro. Lula previously served two terms as Brazil’s president from 2003 to 2011.

Economic data

U.S.

- The Commerce Department’s Personal Consumption Expenditures (PCE) Index—the Federal Reserve’s (Fed) preferred inflation measure as it excludes volatile food and energy prices—slowed in October to 0.3% from 0.6% for the month and to 6.3% from 6.6% for the 12-month period.

- The U.S. employment situation remained robust. The Department of Labor reported that U.S. payrolls expanded by a larger-than-expected 263,000 during November, while the unemployment rate was unchanged at 3.7%. In October, average hourly earnings gained 0.6% for the month and 5.1% year over year.

- The U.S. economy continued to improve in the third quarter, expanding at an annualized rate of 2.9% (up from the Commerce Department’s initial estimate of 2.6%)—after contracting at annualized rates of 1.6% in the first quarter and 0.6% in the second quarter.

- The Institute for Supply Management’s manufacturing purchasing managers’ index (PMI) declined in November by 1.2% to 49.0%, ending 29 consecutive months of expansion as it reached its lowest level since May 2020. A PMI reading below 50% indicates contraction.12

U.K.

- Consumer prices in the U.K. increased in October by 2.0% for the month and by 11.1% for the 12-month period, the highest year-over-year inflation rate since the National Statistics series began in January 1997.13

- According to the Office for National Statistics, U.K. GDP decreased 0.2% over the three-month period ending September, up slightly from the 0.1% decline in the second quarter of this year.

- U.K. manufacturing activity contracted for the fourth consecutive month in October after growth began to slow in May.14

- Activity in the U.K. services sector contracted for the second straight month in November after expanding at a modest-but-healthy pace through the summer and leveling off in September.15

Eurozone

- Eurozone consumer prices dipped in November by 0.1%, the first decline since mid-2021, and slowed to a 10.0% year-over-year increase from a 10.7% gain in the 12-month period ending October.16

- A contraction in eurozone manufacturing activity that began in July continued in November, though there was modest improvement from the prior month.17

- Eurozone services activity declined for the fourth consecutive month in November after expanding for 17 straight months from March 2021 to July 2022.18

- Eurozone economic growth slowed in the third quarter to 0.2% from 0.8% over the three-month period and to 2.1% from 4.3% in the year over year.

Central banks

- In early November, the Federal Open Market Committee implemented another 0.75% increase in the federal-funds rate—bringing it to a range of 3.75% to 4.0%, which will result in higher borrowing costs for consumers and businesses. Fed Chair Jerome Powell indicated at the end of the month that he believes the central bank will likely begin to slow the pace of interest-rate hikes in mid-December as recent data point to easing inflation. However, he also said there remains uncertainty with regard to inflation and that “History cautions strongly against prematurely loosening policy.”19

- The Bank of England’s (BOE) Monetary Policy Committee raised its benchmark interest rate by 0.75% to 3.0% in early November, yet cited the need to reduce the U.K.’s historically high inflation rate. The BOE also noted, “The labor market remains tight and there have been continuing signs of firmer inflation in domestic prices and wages that could indicate greater persistence.”20

- The European Central Bank’s (ECB) applicable rates for its third targeted longerterm refinancing operation (TLTRO III) aligned with its deposit-facility rate on November 23. The lending facility was originally established to foster credit availability but has essentially enabled bank subsidies as interest rates have risen, prompting the ECB’s action.

- The Bank of Japan (BOJ) did not meet in November. At its meeting in late October, the central bank maintained its short-term interest rate at -0.1%, and the 10-year Japanese government-bond (JGB) yield target held near 0%. The BOJ has continued to offer purchases of 10-year JGBs at 0.25% in an effort to keep yields within its acceptable range.

SEI’s view

Russia’s assault on Ukraine and its energy blackmail against Europe (and, by extension, the rest of the world) and the aggressive response of central banks to high global inflation or the severe COVID-19-related slowdown in China are not new. All have simply increased in intensity. Most importantly (from an economic perspective) is that monetary-policy makers are finally acknowledging the major inflation problem on their hands, one that is neither transitory nor likely to be resolved without pain.

In our opinion, investors should be prepared to see a federal-funds rate that could exceed 5%. Other central banks globally are following the Fed’s lead, talking tough and implementing outsized policy-rate increases.

Europe will continue to be the area most under pressure due to the possibility that Russia again will suspend natural-gas exports after agreeing to restart shipments under a deal brokered by the UN and Turkey. Although storage facilities within the EU are now nearly 95% full—aided by unusually warm autumn weather, which reduced demand—the continent still needs a steady flow of gas to get through the high-usage winter months.21 Governments may be forced to impose disruptive energy-saving restrictions on businesses and citizens. Heavy users of electricity, from aluminum smelters to glassmakers, have already been shutting down.

The U.K. announced plans to cap electricity costs that amount to 6.5% of GDP. Other countries that allocated funds for energy-related aid in excess of 3% of GDP include Croatia, Greece, Italy, and Latvia. It would not be surprising to see more energy-related fiscal relief. Deficits could balloon in the same way as they did in the early months of the COVID-19 crisis as policy makers do what they must to protect their populations.

Central bankers globally are mandated to lean hard against the rising trend in prices—even though doing so goes against their own governments’ stimulus efforts. Unfortunately, they’re running just to keep up with the Fed. Interest-rate differentials versus the U.S. are still wide, with only Canada’s yields on par with those in the U.S.22

The large differential in favor of the U.S. and the perception that the country is better positioned economically are two major reasons behind the U.S. dollar’s extraordinary appreciation this year. Although a declining currency may give a competitive boost to domestic firms that export goods and services to the U.S. market, it exacerbates inflationary pressures stemming from imports priced in U.S. dollars—most importantly, oil and liquefied natural gas.

Several large U.S. multinational companies have warned that U.S. dollar strength is beginning to exert a negative impact on revenues, suggesting that the currency’s value has risen well beyond its purchasing-power parity (PPP) level. But discrepancies can last for a long time between PPP and market-based exchange rates.

Still, it would not be surprising to see at least a temporary reversal in the U.S. currency’s trend. Indeed, the greenback declined versus many major currencies following the U.S. government’s release of generally encouraging inflation data in November. Given a catalyst—coordinated government action to weaken the dollar or a surprisingly weak U.S. unemployment report, for example—traders might cover their long positions in a major way, causing the dollar to fall further.

After lagging the inflation rate for several years, U.S. hourly compensation rose at an annualized rate of 5% over the three-year period ending November 30, 2022—virtually matching the increase in the U.S. Consumer Price Index during the same period.23 Similar to the 1970s experience, compensation gains have been accelerating despite slowing productivity growth. This divergence is concerning. The difference between the change in compensation and the change in productivity equals the change in unit labor costs.

Although unit labor costs are more volatile than inflation, there is still a strong positive correlation between the two. Unfortunately, history shows that it usually takes an outright recession to tame inflation, especially when it gets this intense.

Fed Chair Jerome Powell’s hope for a soft landing appears to be an exercise in wishful thinking. Unit labor costs jumped in the year over year through August at a rate that far exceeded inflation—and we see no reason to expect a major reversal in the near term, even if the economy stumbles into a bona fide recession.

U.S. companies have been able to push their higher employment and supply costs onto consumers. While economy-wide profit margins have remained above almost all cyclical peaks since 1947, we suspect that margins are on the cusp of a substantial erosion. It’s typical for profit margins to decline well before an economic recession materializes.24

If the economy does fall into recession and profits decline, it will probably force analysts to mark down earnings estimates aggressively in order to catch up with reality. Investors are not waiting for those earnings revisions. They have been pushing equities lower in reaction to the Fed’s aggressive shift and in anticipation of a recession, both in the U.S. and globally.

Fed policymakers project a federal-funds rate in the 4.4%-to-4.9% range in 2023, but the actual result may still be higher. Unless the central bank is ready to engineer a severe recession, we think PCE price inflation could run in a 3%-to-4% range instead of the pace of less than 2% recorded over much of the past 25 years.

Several asset classes looked extremely oversold by the end of the third quarter, including equities, bonds, currencies, and commodities. The U.S. dollar’s sharp climb has reversed most of this year’s appreciation in the commodities complex. If the currency breaks to the downside, commodities should break to the upside.

We maintain a positive outlook on commodities despite the demand destruction occurring in Europe and other parts of the globe. Years of underinvestment in fossil fuels and metals mines will likely lead to periodic shortages over the next few years.

The Chinese central government has allowed Hong Kong and Macau to open up. This might be a harbinger of what will happen on mainland China as President Xi serves his unprecedented third term as General Secretary of the Communist Party National Congress. Xi’s position may seem unassailable, but we suspect he is looking for a way out of his zero-COVID-19 policy. The loosening of restrictions and return to stronger economic growth is the only logical way out.

Other emerging economies would be big beneficiaries of a revival in Chinese economic activity, yet U.S. dollar strength is a central factor for investors in emerging-market equities. The relative total-return performance of the MSCI Emerging Market Index versus the MSCI World Index peaked in 2010, more-or-less concurrent with the trough in the trade-weighted value of the U.S. dollar. (Trade-weighting measures the value of the dollar versus other major currencies.) As the U.S. currency grew stronger, emerging-market equities weakened further and, as of the end of the third quarter, surrendered almost all the gains achieved between 2000 and 2010 versus advanced-country stock markets.

The rate-hiking cycle began far sooner in less-developed economies—during the latter months of 2020. It was not until this year that advanced economies began a general up-cycle in policy rates; in response, interest-rate hikes in the emerging world have accelerated significantly, in both frequency and magnitude. Threemonth government bond yields are in double digits in Brazil, Colombia, Hungary, and Turkey, with only Brazil’s yield comfortably above the inflation rate. Turkey, by contrast, is facing an inflation rate of more than 85%.25 Nonetheless, the Central Bank of the Republic of Turkey cut its benchmark interest rate by 1.5% to 9.0% in November. This action appears to reflect President Erdogan’s efforts to spur economic and employment growth amid skyrocketing inflation. Little wonder that the value of the Brazilian real has fallen modestly against the U.S. dollar this year while the Turkish lira has declined by nearly 30%.

While the collective effort of major central banks to tame inflation may prove successful, a global recession will likely result—with Europe and the U.K. more vulnerable than the U.S. to a downturn.

Short-term gyrations notwithstanding, the primary trend in risk assets still appears negative. Inflation in the U.S. probably has peaked, as indicated by the relatively smaller increase in the PCE Index in October, but we do not expect it to fall as rapidly or as far as the Fed’s projection of an annualized inflation rate of 2.8% to 3.5% for 2023.26 The central bank may still be underestimating the extent to which it needs to tighten policy in order to slow the economy and produce slack in the labor markets.

Glossary of Financial Terms

Anti-fragmentation tool: An anti-fragmentation tool refers to the ECB’s plans to mitigate widening spreads between German government bond yields and those of economically weaker EU members.

Asset Purchase Programme (APP): The ECB’s APP is part of a package of non-standard monetary policy measures that also includes targeted longer-term refinancing operations, and which was initiated in mid-2014 to support the monetary policy transmission mechanism and provide the amount of policy accommodation needed to ensure price stability.

Balance sheet: The balance sheet, as it relates to a central bank, refers to assets—for example, government bonds or mortgagesbacked securities—that it has accumulated to support the transmission of monetary policy.

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor

confidence is low.

Commercial paper: Commercial paper is a type of short-term loan that is not backed by collateral and does not tend to pay interest.

European Commission: The European Commission is the executive branch of the European Union. It operates as a cabinet government, with 27 members of the Commission headed by a President.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Gilt: Sovereign debt securities issued by the U.K. government.

Group of 7 (G7): The G7 is an inter-governmental forum for the leaders of major advanced democratic nations that includes Canada, France, Germany, Italy, Japan, the U.K. and the U.S.

Hawk: Hawk refers to a central-bank policy advisor who has a negative view of inflation and its economic impact, and thus tends to favor higher interest rates.

Inflation: Inflation refers to rising prices.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Mortgage-backed securities: Mortgage-backed securities (MBS) are pools of mortgage loans packaged together and sold to the public. They are usually structured in tranches that vary by risk and expected return.

NATO: The North Atlantic Treaty Organization (NATO) is an intergovernmental military alliance among 28 European countries and 2 North American countries.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset-purchase program of private and public sector securities established by the European Central Bank to counter the risks to monetary-policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Politburo Standing Committee: The Politburo Standing Committee of the Chinese Communist Party is the top leadership group of the Communist Party, which controls the People’s Republic of China under one-party rule.

Price-to-earnings (PE) ratio: The PE ratio is equal to the market capitalization of a stock or index divided by trailing (over the prior 12 months) or forward (forecasted over the next 12 months) earnings. The higher the PE ratio, the more the market is willing to pay for each dollar of annual earnings.

Purchasing power parity (PPP): Purchasing power parity is the exchange rate at which the currency of one country would have to be converted into that of another country to buy the same amount of goods and services in each country.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Recession: Recession refers to a period of economic decline and is generally defined by a drop in GDP over two successive quarters.

Summary of Economic Projections: The Fed’s Summary of Economic Projections (SEP) is based on economic projections collected from each member of the Fed Board of Governors and each Fed Bank president on a quarterly basis.

Targeted longer-term refinancing operations (TLTRO): The TLTROs are Eurosystem operations that provide financing to credit institutions. By offering banks long-term funding at attractive conditions they preserve favorable borrowing conditions for banks and stimulate bank lending to the real economy.

Transmission Protection Instrument (TPI): The European Central Bank established the TPI to ensure the smooth transmission of monetary policy normalization across eurozone countries. According to the ECB, the TPI “can be activated to counter unwarranted, disorderly market dynamics” by making “secondary market purchases of securities issued in jurisdictions experiencing a deterioration in financing conditions.”

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Index Descriptions

Consumer price indexes measure changes in the price level of a weighted-average market basket of consumer goods and services purchased by households. A consumer price index is a statistical estimate constructed using the prices of a sample of representative items whose prices are collected periodically.

The Bloomberg Commodity Index is composed of futures contracts and reflects the returns on a fully collateralized investment in the Index. This combines the returns of the Index with the returns on cash collateral invested in 13-week (3-month) U.S. Treasury bills.

The Bloomberg Global Aggregate Index is an unmanaged market capitalization-weighted benchmark that tracks the performance of investment-grade fixed-income securities denominated in 13 currencies. The Index reflects reinvestment of all distributions and changes in market prices.

The MSCI ACWI Index is a market capitalization-weighted index composed of over 2,000 companies, and is representative of the market structure of 46 developed- and emerging-market countries in North and South America, Europe, Africa and the Pacific Rim. The Index is calculated with net dividends reinvested in U.S. dollars.

The MSCI China Index captures large and mid-cap representation across China H shares, B shares, Red chips and P chips. The index’s 151 constituents, comprise about 85% of this China equity universe.

The MSCI Emerging Markets Asia Index comprises large- and mid-cap stocks representing approximately 85% of the free floatadjusted market capitalization of China, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

The MSCI Emerging Markets Europe Index is a free float-adjusted (i.e., including only shares that are available for public trading) market capitalization-weighted index that tracks the performance of large- and mid- cap representation across 14 developed-market countries in Europe.

The MSCI Emerging Markets Index is a free float-adjusted (i.e., including only shares that are available for public trading) market capitalization-weighted index that tracks the performance of emerging-market equities.

The MSCI North America Index tracks the performance of the large- and mid-cap segments of the U.S. and Canada markets. With 712 constituents, the index covers approximately 85% of the free float-adjusted (i.e., including only shares that are available for public trading) market capitalization in the U.S. and Canada.

The MSCI USA Index tracks the performance of the large- and mid-cap segments of the U.S. market. With 624 constituents, the index covers approximately 85% of the free float-adjusted i.e., including only shares that are available for public trading) market capitalization in the U.S.

The MSCI World Index is a free float-adjusted market- capitalization-weighted index that is designed to measure the equity market performance of developed markets.

The Personal Consumption Expenditures (PCE) Price Index is the primary inflation index used by the U.S. Federal Reserve when making monetary-policy decisions

The S&P 500 Index is a market capitalization-weighted index that consists of 500 publicly traded large U.S. companies that are considered representative of the broad U.S. stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments.

Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.

Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document, Summary of UCITS Shareholder rights (which includes a summary of the rights that shareholders of our funds have) and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents. And you should read the terms and conditions contained in the Prospectus (including the risk factors) before making any investment decision.