Monthly Market Commentary: Russian invasion rattles the world

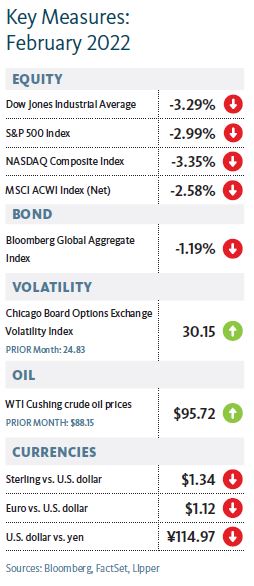

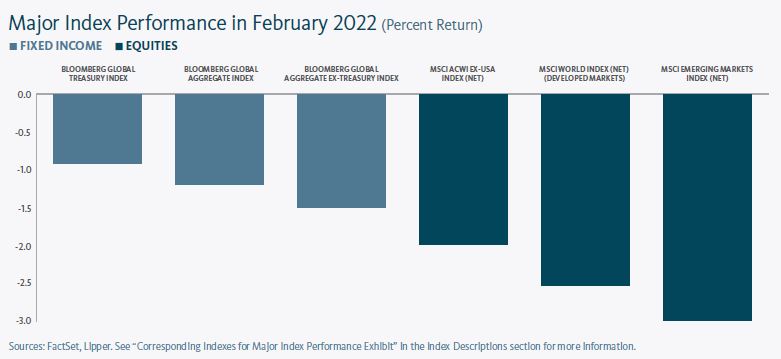

Global equities saw their 2022 losses deepen during February, although they fell by less than in January. Russia was unsurprisingly the worst-performing country, with the MSCI Russia Index plunging by 52.75% for the month; shares cratered as its invasion of Ukraine invited sanctions from around the world that crippled its financial markets.

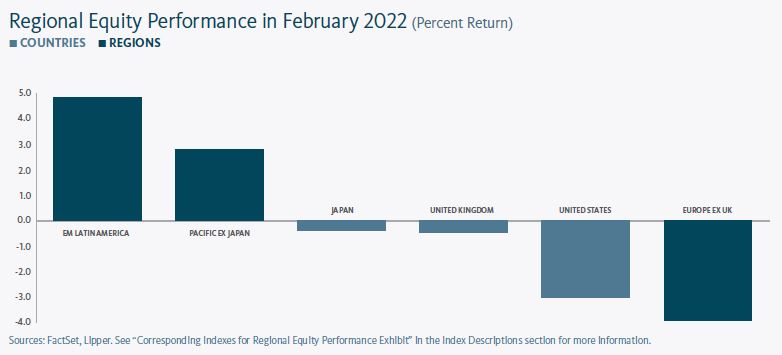

Russia (which accounted for roughly 3% of the MSCI Emerging Markets Index as at 31 January 2022) weighed on emerging markets, which slightly lagged developed markets in February. A boost from commodity exporters in Latin America helped to minimise the gap between emerging- and developed-market performances.

Among major equity markets, the UK was the best performer with a small gain. Japan declined but fared better than both Europe and the US, while Hong Kong and China had steeper selloffs.

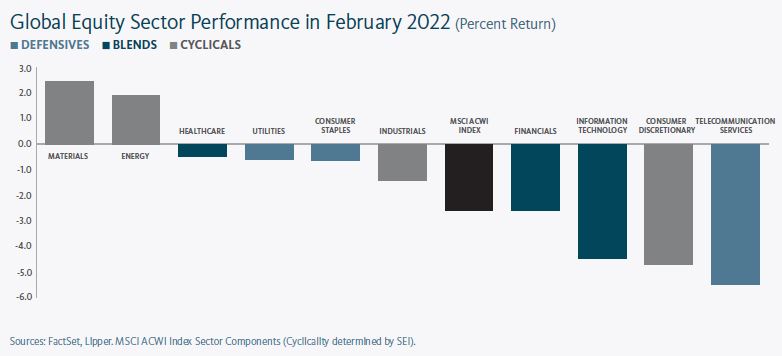

Value-oriented shares continued to fall by considerably less than their growth-oriented counterparts. Globally, the only equity sectors with positive performance were materials and energy.

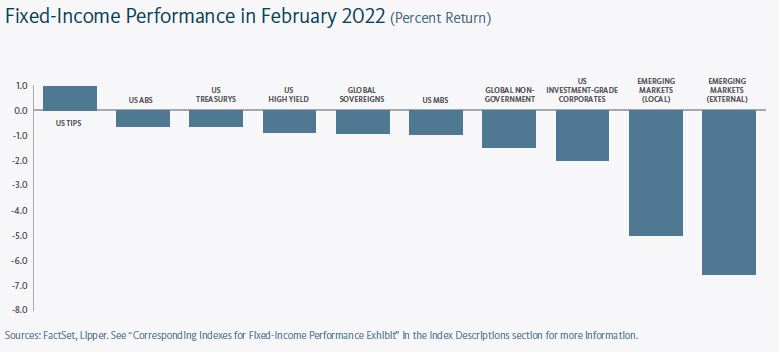

Government bond rates increased across maturities in the UK, eurozone and US during February. Rates rose sharply through mid-month before partially retreating during the second half of the month. Long-term US Treasury yields fell significantly in late February, flattening the Treasury yield curve.

Emerging-market debt plummeted during the month, most sharply within local-currency assets, and most other areas of fixed interest were also down. Inflation-indexed securities were positive.

Commodity prices made a subdued advance for most of February before catapulting higher in the final days of the month (and into the beginning of March) as markets reacted to the unfolding attack on Ukraine. The Bloomberg Commodity Index increased by 6.2% in February, while Brent and West-Texas Intermediate crude oil prices gained 9.8% and 8.6%, respectively, before racing past the $100 per barrel mark on 1 March. Russian oil prices actually declined at the end of February as refiners and lenders began to limit financial commitments with Russian producers.

Ukraine’s emergency service reported in early March that more than 2,000 civilians had been killed during Russia’s invasion. The Russian Defence Ministry stated that 498 soldiers had been killed and more than 1,500 wounded,significantly below the 5,800 Russian casualties reported by Ukrainian officials.Approximately one million Ukrainians had fled their country by early March.

Western nations responded to Russia’s offenses with an array of sanctions, bans, and other coordinated actions—largely focused on disrupting the country’s financial, energy, technology and transportation activities, as well as state-owned enterprises and high-profile individuals in public and business positions.

In addition to having mounted a fierce resistance to Russia’s invasion, Ukraine submitted a formal application for admission to the EU. NATO activated its Response Force for the first time, calling up 40,000 troops to bolster the eastern part of the alliance in the face of intensifying aggression toward Ukraine.

The European Commission, France, Germany, Italy, the UK, Canada, and the US committed to removing Russian banks from the SWIFT (Society for Worldwide Interbank Financial Telecommunication) messaging system for financial payments; block the Russian Central Bank from deploying its international reserves; limit the sale of citizenship to wealthy Russians; and launch a transatlantic task force to freeze the assets of sanctioned entities.

In practice, the moves have essentially blocked Russian entities from trade in major foreign currencies. Upon imposition of these coordinated sanctions, the Russian Central Bank was forced to hike its benchmark rate from 9.5% to 20%; offer unlimited liquidity support to banks as they faced runs; raise capital controls on exporters and residents; and shutter its financial markets.

Corporations across industries began to disentangle their relationships with Russia and Belarus at the end of February and in early March. Major energy companies announced withdrawals from Russian partnerships, including BP’s large stake in Rosneft and joint ventures involving Exxon Mobil, Shell, Total and others.

Russian airlines were banned from Western airspace, largely crippling Russia’s ability to maintain an international flight industry. Boeing and Airbus announced they would stop providing parts and services to Russian companies, which is expected to disrupt Russian domestic flight as well.

Economic Data

UK

- UK manufacturing growth edged upward in February, returning to the high side of the generally strong expansion that has prevailed over the last six months.

- UK services activity exploded in February after cooling to a more modest expansion in December and January.

- The UK claimant count (which calculates the number of people claiming Jobseeker’s Allowance) declined in December for the eleventh straight month, by roughly 32,000.

Eurozone

- Manufacturing growth in the eurozone remained strong in February, expanding at roughly the same pace as it has since September.

- The eurozone services sector leapt to heathier growth levels in February after slowing to a relatively anaemic expansion in December and January.

- An early estimate of eurozone consumer price inflation measured 0.9% in February and 5.8% year over year, up from 0.3% and 5.1%, respectively, in January.

US

- After cooling slightly in December and January, the still-robust pace of US manufacturing growth accelerated in February as new orders growth jumped and employment growth slowed.

- Growth in the US services sector accelerated sharply in February after nearly pausing altogether in January.

- New US jobless claims moderated in February, ranging between 200,000 and 250,000 per week during the month.

- US economic growth outpaced expectations in the fourth quarter of 2021, accelerating to an annualised pace of 7.0% from an annualised pace of 2.3% in the prior quarter.

Central Banks

- The Bank of England’s (BOE) Monetary Policy Committee (MPC) reconvened at the beginning of February for its first meeting since raising its bank rate in December 2021—and issued its first back-to-back rate hike in 18 years with an increase of 25 basis points (bps) to 0.50%.15 (A large minority of MPC members voted for a more aggressive 50 bps increase to counteract high inflation.) Additionally, the central bank said it intends to reduce the size of its balance sheet by ceasing to re-invest proceeds from its asset-purchase programme.

- The European Central Bank (ECB) also held its inaugural meeting of 2022 at the beginning of February, after which ECB President Christine Lagarde acknowledged that the widespread stress inflation has caused will likely continue over the short term. Following Russia’s invasion of Ukraine, Lagarde pledged that the ECB “will ensure smooth liquidity conditions and access of citizens to cash,” and that it “stands ready to take whatever action is needed to fulfil its responsibilities to ensure price stability and financial stability in the euro area.”

- The US Federal Open Market Committee (FOMC) did not hold a meeting in February. Federal Reserve (Fed) Chair Jerome Powell stated at the beginning of March that he thinks a 0.25% increase in the fed-funds rate would be appropriate; if enacted at the FOMC’s mid-March meeting, this would be the central bank’s first rate hike since December 2018. The FOMC made a final $30 billion round of new asset purchases in February after releasing a statement in January outlining principles for reducing the size of its balance sheet.

- The Bank of Japan (BOJ) also held no meetings on monetary policy in February.The central bank’s policy orientation remained fixed following its mid-January meeting, with its short-term interest rate at -0.1% and the 10-year government bond yield target near 0%—but its expectations increased for higher inflation. Previously, the BOJ announced that it would revert purchases of corporate bonds and commercial paper to pre-pandemic levels beginning in April.

SEI’s View

We have been watching Russia’s escalating aggression toward Ukraine with the same dread that’s undoubtedly shared by much of the rest of the world.

As investment managers, we take a high degree of comfort from the fact that direct exposure to Russian assets was already quite low across capital markets before the invasion-induced selloff. Still, it’s important to consider second- and third-order consequences, including those resulting from sanctions and other associated actions, which could reverberate through markets for the foreseeable future.

We believe the primary impact on economic growth will be transmitted via commodity markets, with Europe sustaining the greatest impact. Economic growth will likely be hit in the near term, although it’s possible that the extent of any slowdown could be modest as disruptions associated with the COVID-19 Omicron variant rapidly fade and offset some of these headwinds. Households and businesses are in good financial shape heading into this crisis; while the monetary and fiscal response will likely be limited, the odds of an aggressive tightening of monetary policy this year are now considerably lower.

From an asset-allocation perspective, we are humble enough to know that skilled forecasting—even where it exists—does not warrant wholesale changes to portfolio allocations based on tactical views. This is particularly important to understand in the context of fast-moving geopolitical events. Efficient strategic portfolio construction through broad-based diversification helps to prepare our portfolios for adverse events before they happen. We believe it’s much cheaper to buy insurance before the flood.

By acknowledging both risk and uncertainty, we seek to construct resilient portfolios designed to achieve success across a wide range of economic and market outcomes, not just benign environments where we can rely on strong growth and well-behaved inflation.

Thinking about domestic issues, the year ahead still looks like it will be another one of tight labour markets, particularly in the US. We think more people will return to the workforce as COVID-19 fears ease, but there likely will remain a tremendous mismatch of demand and supply. US wage gains have climbed at their fastest pace in decades over the past year.17 The UK also is experiencing a pronounced upswing in its labour-compensation trend. We think Brexit and the departure of foreign workers back to the Continent have aggravated the country’s labour shortage.

Predicting a bad inflation outcome for 2022 isn’t exactly much of a risk. Where we depart from the crowd on inflation is in the years beyond 2022. We are sceptical that the US Fed will be sufficiently proactive as it struggles to balance full and inclusive employment against inflation pressures that are starting to look more entrenched. In our view, this will be the central bank’s biggest challenge in 2022 and beyond.

We also don’t think the Fed’s inflation and economic projections are internally consistent. Given its expectation that the economy will be even closer to full employment later into 2022 and beyond, we find it hard to understand why price pressures should ease so dramatically.

Even the central banks that are most likely to taper their asset purchases and raise policy rates in the months ahead will probably do so cautiously. By contrast, policy rates in emerging economies have already jumped.

It remains to be seen whether this pre-emptive tightening of monetary policy will forestall a 2013-style taper tantrum as the Fed embarks on its own rate-tightening cycle.

The People’s Bank of China (PBOC) cut a key interest rate in December and then again in January, both by modest amounts. These cuts followed a reduction in reserve-requirement ratios aimed at increasing the liquidity available to the economy; it will take a while for any beneficial impact to be felt on China’s domestic economy, and even longer for the world at large.

In addition to the start of a new monetary tightening cycle, some economists have expressed concern about the next “fiscal cliff” facing various countries, the US in particular. While there will be a negative fiscal impulse in the sense that the extraordinary stimulus of the past two years will not be repeated, we argue that the impact should be less contractionary than feared.

Perhaps economists should be more concerned about the negative fiscal impulse in the UK, Canada, Germany, and Japan. They are each facing a potential fiscal tightening equivalent to 4% of GDP this year. By comparison, the International Monetary Fund predicts that the cyclically adjusted deficit in the US will contract by less than 0.5% of GDP.

There are always uncertainties to consider when it comes to investing; currently, we are focused on three main areas of geopolitical risk. First, as we have stressed since the beginning of the year, Russian aggression toward Ukraine has been the most important flashpoint in terms of near-term probability and economic impact—especially now that it has escalated into a full-scale attack.

Next is the ongoing tug-of-war between China and the US for influence and military advantage. Here, the most worrisome flashpoint would be over Taiwan given its dominant position in advanced semiconductor manufacturing.

The third major area of concern remains the Middle East and the negotiations with Iran over its nuclear development program. Two things are clear: Iran is now much closer to having a nuclear bomb, and Israel still will not tolerate such a major change in the region’s balance of power. The risk of such a war may still be low, but developments continue to head in a direction that could someday have catastrophic consequences.

In our view, the real anomaly in the financial markets is the ultra-low levels of interest rates in the face of higher inflation and above-average growth in much of the world. This may force central banks to adopt more aggressive interest-rate policies than they and market participants currently envision.

Glossary of Financial Terms

Commercial paper: Commercial paper is a type of short-term loan that is not backed by collateral and does not tend to pay interest.

Cyclical stocks: Cyclical stocks or sectors are those whose performance is closely tied to the economic environment and business cycle. Managers with a pro-cyclical market view tend to favour stocks that are more sensitive to movements in the broad market and therefore tend to have more volatile performance.

European Commission: The European Commission is the executive branch of the European Union. It operates as a cabinet government, with 27 members of the Commission headed by a President.

Fiscal cliff: A fiscal cliff refers to the reduction or withdrawal of government spending, an increase in taxation, or both.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Inflation-Protected Securities: Inflation-protected securities are typically indexed to an inflationary gauge to protect investors from the decline in the purchasing power of their money. The principal value of an inflation-protected security typically rises as inflation rises, while the interest payment varies with the adjusted principal value of the bond. The principal amount is typically protected so that investors do not risk receiving less than the originally invested principal.

International Monetary Fund: The International Monetary Fund (IMF) is an international organisation of 189 member countries that promotes global economic growth and financial stability, encourages international trade, and reduces poverty.

Liquidity: Liquidity refers to the ease with which a holding can be bought or sold without moving its price.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Mortgage-Backed Securities: Mortgage-backed securities (MBS) are pools of mortgage loans packaged together and sold to the public. They are usually structured in tranches that vary by risk and expected return.

NATO: The North Atlantic Treaty Organization (NATO) is an intergovernmental military alliance among 28 European countries and 2 North American countries.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Taper tantrum: Taper tantrum describes the 2013 surge in US Treasury yields resulting from the US Federal Reserve’s announcement of future tapering of its policy of quantitative easing.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Index Descriptions

The Bloomberg Commodity Index is composed of futures contracts and reflects the returns on a fully collateralised investment in the Index. This combines the returns of the Index with the returns on cash collateral invested in 13-week (3-month) US Treasury bills.

The MSCI Emerging Markets Index is a free float-adjusted market-capitalisation-weighted index designed to measure the performance of global emerging-market equities.

The MSCI Russia Index is designed to measure the performance of the large- and mid-cap segments of the Russian market. With 26 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Russia.

The S&P 500 Index is a market-capitalisation-weighted index that consists of 500 publicly-traded large US companies that are considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of

the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should

it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other

nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments.

Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments

may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any

action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation

to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or

using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.