Monthly Market Commentary: Rising Rates Restrain the Rally

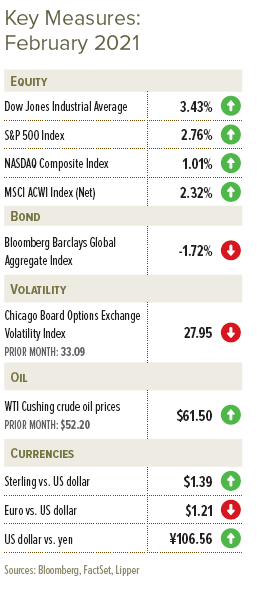

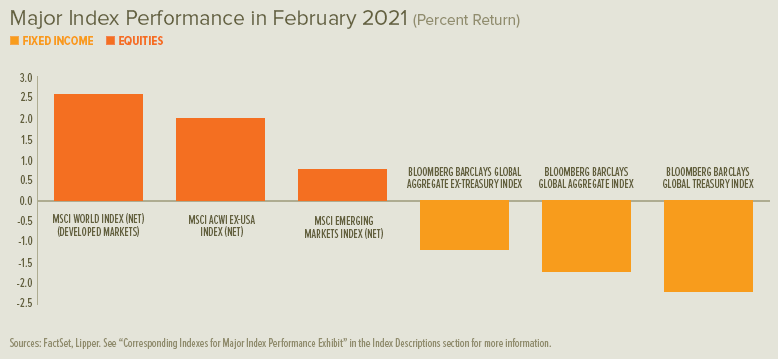

Risk assets continued their advance through the first half of February without any real setbacks. Shares were higher around the world until the middle of the month, when government-bond yields (which had been rising slowly since the fall) began to spike further. The spectre of a sharp increase in borrowing costs sent chills through markets during the second half of February, leading to selloffs of varying intensity. Full-month equity performance, however, was still positive around most of the world.

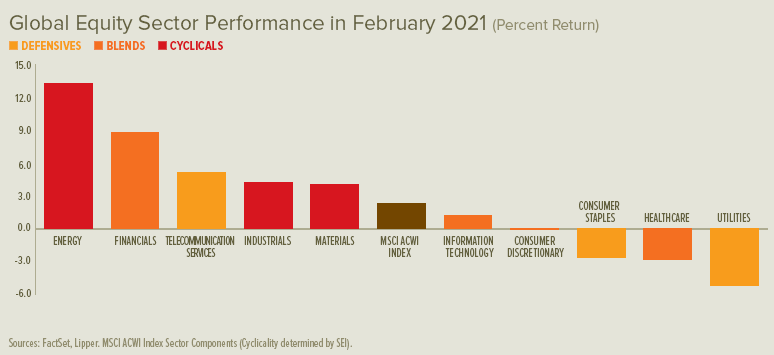

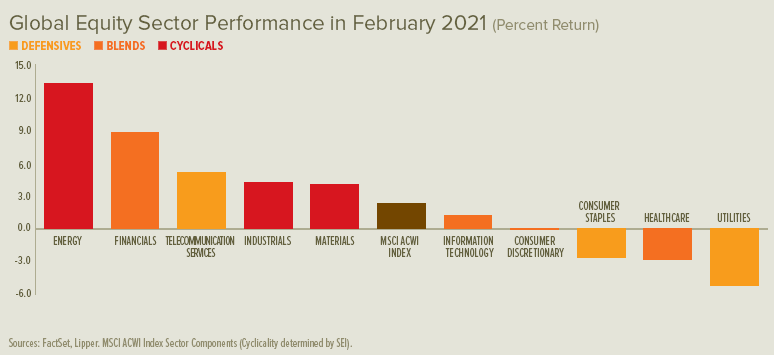

Developed-market equities outperformed emerging markets during the month, with mainland Chinese equities negative and Brazil among the worst performers. UK shares led among major developed markets, followed by the US, Hong Kong, eurozone and Japan. Energy and financials delivered the best sector-level performance in February. Value-oriented shares beat their growth-oriented peers, and small-cap shares outpaced large caps.

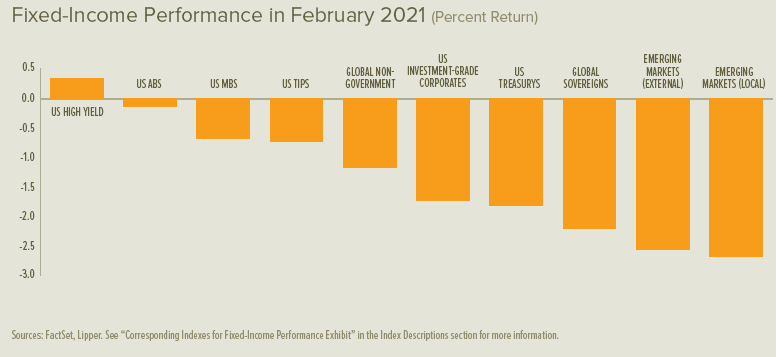

UK and eurozone government-bond rates increased across all maturities during the month, although long-term rates rose by considerably more than short-term rates. In the US, short-term Treasury rates fell by a small amount, while long-term rates pushed higher. The 10-year Treasury yield—a reference rate for everything from corporate debt to mortgages—briefly rose to its highest level in more than a year near the end of February.

The US dollar stayed near its January low (relative to a trade-weighted basket of foreign currencies) and remained confined to the range it has established since early December. The West Texas Intermediate crude-oil price climbed from $52.20 to $61.50 per barrel, or 17.8%, during the month.

In late February, with COVID-19 cases expected to continue declining with the aid of vaccines, UK Prime Minister Boris Johnson unveiled a four-stage plan to reopen England:

- Reopen schools on 8 March and larger outdoor gatherings and sports on 29 March.

- Reopen non-essential retail businesses and cease curfews for restaurants and pubs (still limited to outdoor seating) as early as 12 April, depending on the progression of the infection rate.

- Conclude most social-contact rules (two households will be allowed to meet indoors), and reopen hospitality businesses to indoor service as soon as 17 May.

- Retire any remaining social-contact limits and reopen all still-closed businesses as early as 21 June.

In the US, estimated daily COVID-19 case counts had fallen by the end of February toward the low point of September last year. The US Centers for Disease Control and Prevention (CDC) released updated school reopening guidelines in mid-February that spurred state health departments and local school districts to coordinate plans for more in-person learning and fewer virtual classes.

The US House of Representatives passed a $1.9 trillion economic relief bill at the end of February. The bill will likely be modified by the Senate to exclude a minimum-wage increase that is not allowed in packages passed under the Senate’s reconciliation rules (under which bills may be passed with a simple majority rather than the Senate’s typical 60% majority requirement—as long as the whole bill directly addresses taxes, spending or the level of the US debt).

Johnson & Johnson’s (J&J) COVID-19 vaccine received emergency-use authorisation from the US Food and Drug Administration at the end of February. While less effective than the Pfizer-BioNTech and Moderna vaccines that received the first two emergency approvals, the J&J vaccine only requires one dose (as opposed to the others’ two-dose regimen) and can be stored at the temperature of a regular refrigerator (as opposed to the sub-zero temperatures required to sustain the others) 1. J&J announced an immediate shipment of four million doses, and plans to ship 100 million doses by June and potentially one billion doses by the end of the year.

Following the January collapse of Italy’s governing coalition and subsequent resignation of Prime Minister Giuseppe Conte, Italian President Sergio Mattarella asked former European Central Bank President Mario Draghi to form a technocratic government. Draghi answered his call, and his national unity platform—which includes cabinet ministers from across and outside of the political spectrum—received support from parties in the centre, left, and right. He was sworn in as prime minister on 13 February.

Economic Data

- UK manufacturing growth improved to healthier levels in February after slowing in January from a relatively brisk fourth quarter. The country’s services sector activity was in a holding pattern during February, neither expanding nor contracting, after plummeting in the prior month. The UK claimant count (which calculates the number of people claiming Jobseeker’s Allowance) decreased by 0.1% to 7.2% in January, representing roughly 2.6 million total claimants. The broad UK economy grew by 1.2% in December after breaking a six-month recovery trend in November with a 2.6% contraction.

- Eurozone manufacturing growth jumped in February to strong levels, interrupting a fairly slow and steady recovery that began last spring. Like the rest of the world, the eurozone manufacturing sector was temporarily crippled by the early spread of COVID-19; but it had already been suffering from varying degrees of contraction since early 2019. Eurozone services activity continued to shrink during February, having last experienced growth during a fleeting two-month period that ended in August 2020. The eurozone economy contracted by 0.6% during the fourth quarter of 2020 (after changes of -3.6%, -11.8% and +12.5% during the first, second and third quarters, respectively) and shrank by 5.0% during the 2020 calendar year.

- US manufacturing growth remained strong in February. Services sector growth continued to heat up during the month, nearing November’s highs. New weekly US claims for unemployment benefits broke below 800,000 to start February, but climbed to 861,000 by mid-month before recovering to 745,000 by the end of the period. The overall US economy expanded at an annualised 4.1% rate during the fourth quarter (after annualised changes of -5.0%, -31.4% and +33.4% during the first, second and third quarters, respectively).

Central Banks

- The Bank of England’s (BOE) Monetary Policy Committee (MPC) held course at its early-February meeting, keeping the bank rate at 0.1% and retaining a maximum allowance for asset purchases of £895 billion. In response to a banking-system review by the BOE’s Prudential Regulatory Authority that found banks would need six months to prepare for negative benchmark rates, the MPC communicated that it has no intention of introducing a negative rate within the next six months.

- The European Central Bank (ECB) held no monetary-policy meeting during February. In testimony to the European Parliament about the inflation landscape, ECB President Christine Lagarde said, “Underlying price pressures are likely to remain subdued owing to weak demand, low wage pressures and the appreciation of the euro exchange rate.”

- The US Federal Open Market Committee did not hold a meeting during February. Federal Reserve (Fed) Chair Jerome Powell pledged to continue supporting the economy via monetary policy during his semi-annual congressional testimony on 23 and 24 February. He also weighed in on recent concerns about rising price pressures, stating, “I really do not expect we’ll be in a situation where inflation rises to troublesome levels.”

- The Bank of Japan (BOJ) did not hold a meeting on monetary policy during February. The next meeting, scheduled for 18 and 19 March, is expected to coincide with a review of the BOJ’s tools—with an to eye to the eventual prospect of unwinding its deep market interventions that date back as far as the global financial crisis.

SEI’s View

We all continue to look forward to better times ahead. From the looks of it, investors have already begun to set their sights beyond the valley.

Recent market chatter has hinted at the notion of a “Great Rotation” in capital markets, suggesting that investors may have begun to favour value and cyclical sectors over growth names. While there has been some evidence of this, we believe it is still too early to tell if this is the beginning of a major secular shift in equity investment themes.

In our view, several signs of potential normalisation seem to support the prospect of a style regime change.

- US Treasury yields started to tick up last fall and we’ve seen a sustained increase in intermediate-to-long-term interest rates in the year to date.

- The development and improved distribution of highly effective COVID-19 vaccines has helped investors shake worries about the pandemic lasting indefinitely.

- Regulatory changes across multiple jurisdictions have hinted that the dominance of large technology companies may no longer be as straightforward, long-lasting or profitable as some investors have grown accustomed.

No one knows whether these changes truly signal a Great Rotation from growth leadership to cyclical and value-oriented areas of the market. Still, we expect investors will be willing to shrug off the likely prospect of more bad news in the difficult months that lay ahead—including, for example, slowdowns or pauses in the manufacturing, distribution, administration or uptake of COVID-19 vaccines.

Politics will also come into play, with potential to act as either a tailwind or a headwind. The US Congress struggled for months to provide additional income support to the people and businesses most seriously affected by the economic disruptions caused by the virus. The lawmakers finally came up with a $900 billion compromise that is limited in scope and falls far short of what is needed. Most of the benefits are set to expire in March and April, and it does not address revenue shortfalls facing state and local governments. There’s a high likelihood that the Biden administration’s American Rescue Plan (or a variation thereof, pending congressional negotiations) will succeed in getting additional fiscal support to those who need it.

Policy depends on personnel, and the priorities of the Biden administration have already proven to be quite different from those of the Trump era. One of the most important nominations put forth by Biden is that of former Fed Chair Janet Yellen as Treasury Secretary. A close working relationship between the US Treasury and the Fed will probably be reassuring for investors in the near term since there is little doubt that the central bank will continue its extraordinary efforts to support the economic recovery in 2021.

Casting our focus across the Atlantic, the last-minute Brexit deal in December provided a Christmas gift of sorts, at least in terms of removing a degree of uncertainty. While a skinny deal is better than none, the UK’s long period of intense uncertainty has continued to a degree as the deal addressed the transfer of goods but not commerce in services.

Such barriers to trade tend to introduce economic inefficiencies. Post-Brexit, therefore, UK prices will likely move a bit higher, GDP a bit lower and supply chains a bit more unreliable.

Looking at the forward price-to-earnings ratio of the MSCI United Kingdom, MSCI Europe ex-U.K. and the MSCI USA Indexes, we can see that the US market has consistently traded at a premium valuation over the past 15 years.

That premium has widened since 2017 and expanded significantly further in 2020. The other two markets have mostly traded at similar valuations to each other over time—but a major divergence began to develop in 2019 and became more pronounced in 2020.

UK equity valuations, in our opinion, reflect much of the bad news. Maybe it is time for investors to think about the things that could go right:

- First, of course, is the development and distribution of vaccines, which are expected to drive the global economy to higher ground in 2021. This should benefit the large energy, materials and industrial multinationals that make up about one-third of the market capitalisation of the MSCI United Kingdom Index.

- The UK also appears competitive versus other advanced countries when measured by various benchmarks, such as relative unit labour costs.

- The government’s trade negotiators have already fanned out across the world to make sure that the UK retains the same trade agreements that it enjoyed as a member of the EU.

Like so many other relationships in the equity market, the underperformance of the eurozone benchmark has been going on for a long time. Europe is more cyclical, value-oriented and less dynamic than the US—but that does not prohibit a rebound in performance against the US stock market at a time when the US appears to be excessively tilted toward technology stocks, the US dollar is weakening, and a global economic recovery is at hand.

The pandemic has had one good economic outcome for Europe. It finally forced Germany and other fiscal “hawks” to allow an expansion in fiscal policy. This move away from budgetary austerity should be viewed in context. Most countries have experienced a sharp rise in red ink during 2020, with the biggest deficits outside the eurozone. European economies probably can afford to run higher deficits than the International Monetary Fund appears to have pencilled in for 2021. The memory of the European periphery debt crisis is still fresh in the minds of many policymakers who realise that pushing for fiscal austerity measures prematurely would probably be a mistake.

On the other hand, we think there is a greater need for other countries outside the eurozone to regain control of their finances. If those countries fail to do so, Europe could be the beneficiary of investment flows that would further prop up the euro and equity valuations.

Emerging-market equities have been on a tear since they bottomed out last March4. However, the MSCI Emerging Markets Index (total return) is still just above its previous high-water mark recorded in January 2018. Frontier markets have fared even worse. The MSCI Frontier Emerging Markets Index (total return) has yet to surpass its most recent pre-pandemic high level recorded in January 20205.

Fortunately, not only has the combined fire power of global central banks prevented a liquidity crisis, it has also driven borrowing costs down to

near-record lows—even as total emerging-market debt exceeds 200% of GDP6. Only two problem debtors—Argentina and Turkey—had to increase their interest rates in recent months to stem investment outflows. As the world returns to normal, other nations may need to raise interest rates in order to attract sufficient investment inflows to sustain their fiscal and current-account positions.

A weak US dollar is an important catalyst for emerging-markets performance. Although the currency weakened meaningfully in 2020 and pushed emerging-market equities higher, the performance of emerging markets relative to developed markets has been in a narrow range. We anticipate the coming year will see emerging equities’ relative performance improve, partly because the US dollar is expected to continue to weaken.

If the world economy enjoys a durable cyclical recovery in 2021, the US dollar should indeed sink further. A recovery would also bolster the rebound in commodity prices. Commodities of all sorts have been moving sharply higher since the spring, with metals, raw industrials and foodstuffs rallying together for the first time since the 2009-to-2011 period.

As COVID-19 abates and economic activity normalises, signs of a recovery should continue to reveal themselves. In the meantime, fiscal spending and accommodative central-bank policy should sustain GDP growth and eventually cause inflation to rise. As the market prices in these developments, “long-duration” growth and expensive high-profitability stocks will likely be pressured—while momentum investors are expected to rotate into new themes, potentially adding more fuel to this nascent cyclical rally.

Glossary of Financial Terms

Austerity: Austerity refers to measures taken by a country’s government to reduce its expenditures and its budget deficit.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Forward price-to-earnings ratio: The forward price-to-earnings ratio is the ratio of a company’s share price to its forecasted earnings over the next 12 months, which can be used to help determine whether a stock is undervalued or overvalued.

Hawk: Hawk refers to a policy advisor, for example at the Bank of England, who has a negative view of inflation and its economic impact and thus tends to favour higher interest rates.

International Monetary Fund: The International Monetary Fund is an international financial institution, whose work focuses on global monetary cooperation, securing financial stability, facilitating international trade, promoting high employment and sustainable economic growth, and reducing poverty around the world.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Index Descriptions

The MSCI Emerging Markets Index is a free float-adjusted market-capitalisation-weighted index designed to measure the performance of global emerging-market equities.

The MSCI Europe ex-UK Index is a free float-adjusted market-capitalization-weighted index that captures large- and mid-cap representation across developed-market countries in Europe excluding the UK.

The MSCI Frontier Emerging Markets Index is a free float-adjusted market capitalization index designed to serve as a benchmark covering all countries from the MSCI Frontier Markets Index and the lower size spectrum of the MSCI Emerging Markets Index.

The MSCI United Kingdom Index is designed to measure the performance of the large- and mid-cap segments of the UK market.

The MSCI USA Index is designed to measure the performance of the large- and mid-cap segments of the US market.

The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.