Monthly Market Commentary: Rising Outbreak Worry Weakens Equities

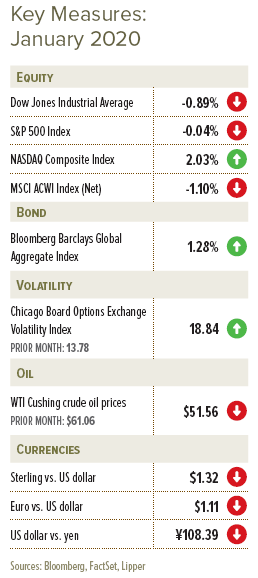

Equity markets around the globe were marked by accelerating volatility throughout the month on intensifying concerns about the coronavirus: A deadly strain originated in Wuhan, China, and began spreading at a faster pace as the month progressed. The number of confirmed cases in mainland China skyrocketed from 45 to well over 11,000 over the final two weeks of January, leading the Chinese government to quarantine millions of citizens in Wuhan1, 2. The outbreak spread to other countries, prompting Mongolia and Russia to close their borders with China and other countries to erect transportation and quarantine barriers to Chinese trade and travel. Beyond the threat to public health, the outbreak and resulting containment measures evoked concerns about the potential dampening of economic activity at the same time that China has struggled to navigate an economic soft patch.

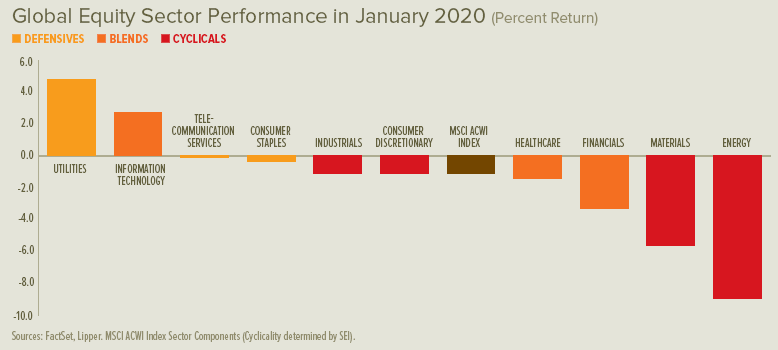

In this environment, UK and European shares were restrained for much of January—barely advancing or declining—before weakening late in the period on concerns about the coronavirus. Asian equities followed a similar path as their UK and European counterparts: Chinese shares tumbled sharply given their proximity to the outbreak and potential for greater fallout; Hong Kong shares also sank, although by less; Japanese equities generally resisted a severe impact. In the US, equities climbed through mid-January before selling off to end the month essentially flat.

Energy prices fell throughout most of January, with declines acclerating later in the month due to a likely clampdown on economic activity tied to quarantines, transportation disruptions and national border closures erected as part of outbreak containment efforts.

Government bond rates fell in the UK, eurozone and US across almost all maturities in January; the declining yields on these safe-haven assets quickened as the month came to a close (bond yields fall when their prices rise). The US Treasury yield curve—which nearly normalised (that is, returned to a positive upward slope) at the end of 2019 after inverting to varying degrees since December 2018—re-inverted across most maturities by the end of January.

The UK formally resigned its membership in the EU at the end of the month after the Conservative Party’s Brexit deal became law on 23 January3. European Parliament ratifed the agreement on 29 January, paving the way for the split4. The two sides will continue to negotiate the terms of their future relationship throughout a transition period that lasts until the end of 2020. Most of the rules that govern trading and travel between the UK and EU will remain in the interim, but the UK forfeited its participation in the EU decision-making process during the transition. If a deal isn’t struck by the end of the year, their trade terms will revert to the rules-based trading system dictated by the World Trade Organization (WTO)—thereby raising tariffs on both sides and slowing the pace of cross-border commerce.

China and the US formalised a “phase one” trade deal in mid-January that offered tariff relief to China (via the reduction of existing tariffs and the delay of additional scheduled tariffs). In exchange, China committed to purchasing $200 billion in US products over a two-year period; addressing its long-standing practice of forcing the transfer of intellectual property and technology to Chinese counterparts in exchange for access to the Chinese market; and promising to continue opening its financial-services industry to foreign investors.

The US-Mexico-Canada trade agreement (USMCA) was approved by the US Congress and signed by President Donald Trump in late January, officially replacing the North American Free Trade Agreement (NAFTA). Earlier in the month, President Trump and France’s President Emmanuel Macron successfully walked back threats of tariffs that originated with French plans for a digital tax that would have targeted US-based multi-national technology companies. The prospect of a digital tax re-surfaced in other countries—including the UK, Italy, Austria and Turkey—which prompted more threats of retailiatory tariffs by US Treasury Secretary Steven Mnuchin. Sajid Javid, the UK’s Chancellor of the Exchequer, disappointed Secretary Mnuchin, his US counterpart, by explaining during a joint interview in late January at the World Economic Forum that the UK would prioritise trade negotiations with the EU over a deal with the US.

President Trump’s impeachment trial unfolded in the US Senate during the second half of January. His eventual acquittal with no expected formal consequences seemed almost universally anticipated—even as the US media surfaced corroborating first-hand accounts of President Trump directing underlying events central to the articles of impeachment. These witnesses—one of which was former National Security Advisor John Bolton, whose depictions were made public by leaks of his as-yet unreleased book manuscript—were blocked by a slim majority from testifying under oath before the Senate.

Geopolitical risks ratcheted higher at the start of the New Year when the Trump administration assassinated Qasem Soleimani, a top Iranian general, in Baghdad on 3 January. The Iranian military retailiated on 8 January by launching missiles at two US military bases in Iraq, reportedly causing more than 50 traumatic brain injuries of US service members—and then accidentally downing a Ukrainian International Airlines commercial jet mistaken for US military aircraft, killing all 176 passengers.

Central Banks

- The Bank of England’s Monetary Policy Committee kept the Bank Rate unchanged at 0.75% following its meeting at the end of January. This was the last Monetary Policy Committee meeting for Governor Mark Carney, who will turn his role over to Andrew Bailey before the next meeting in March.

- The European Central Bank (ECB) maintained its existing monetary-policy path following its January meeting. As expected, the central bank’s governing council also approved a proposed policy review that will consider, among other issues, how the ECB measures inflation targets and whether it can help counteract climate change.

- The US Federal Open Market Committee (FOMC) made no changes to the funds rate following its late-month meeting. However, it detailed multiple steps to maintain ample reserves and keep benchmark rates in line with their targets, including the continued purchase of Treasury bills at least into the second quarter of 2020; the continued offering of repurchase agreements (repos) at least through April 2020; and the continued reinvestment of principal proceeds from the Federal Reserve’s (Fed) balance sheet holdings.

- The Bank of Japan (BOJ) maintained its accommodative monetary-policy orientation following its January meeting, while upgrading its forecast for economic growth and slightly reducing inflation expectations.

- At the beginning of February, the People’s Bank of China (PBOC) reduced short-term reverse repo rates and introduced more than $170 billion in new liquidity to money markets through reverse repos to help offset the increased financial pressures created by the coronavirus outbreak.

Economic Data

- The contraction in UK manufacturing appeared to pause during January, while a preliminary report showed services-sector activity accelerated to healthier levels from an essential standstill. The UK claimant-count unemployment rate increased to 3.5% in December from 3.4% during the prior month. The average UK unemployment rate for the September-to-November period held at 3.8% from the prior period, while average year-over-year wage growth slid from 3.5% to 3.4%.

- Eurozone manufacturing activity shrank by less in January than during the prior month. Growth in the services sector cooled, however. The EU unemployment rate declined to 7.4% in December from 7.5% during November. An early report of overall economic activity showed the eurozone grew by only 0.1% during the fourth quarter of 2019 and 1.0% year over year, down from 0.3% and 1.2%, respectively, in the third quarter.

- Multiple reports showed US manufacturing conditions in growth territory during January after indications that activity contracted through the end of 2019. Services sector growth also increased, according to a preliminary report. The US economy grew by a 2.1% annualised rate during the fourth quarter of 2019 and 2.3% for the full year, its slowest calendar-year growth rate in three years.

SEI’s View

At the beginning of 2019, many investors were licking their wounds following a sharp global stock-market correction. Today we are confronted with a notably different market backdrop as share prices generally ended 2019 near their highs of the year. With regard to the US economy, our expectations turned out to be mildly optimistic. But we think it’s worth pointing out that quarter-to-quarter fluctuations in the country’s gross domestic product (GDP) growth have remained on a relatively narrow path compared to their far more volatile historical range. One reason for the lower volatility is steady growth in US household spending. By contrast, the contribution to US GDP growth from investment, both residential and non-residential, has been in a slowing trend; the pace of business spending in the country has eased dramatically since early 2018. On the positive side, the absence of an investment boom means there should be little to no side effect; even if a recession were to develop in the next year or so, it almost certainly will not be especially painful.

On this side of the pond, Prime Minister Boris Johnson’s decision to hold a snap election paid off. He now enjoys the largest Tory majority in Parliament since 1987, when Margaret Thatcher was re-elected Prime Minister for a third term5. The victory eliminated the possibility of a dramatic remaking of the British economy as envisioned by the Labour party—or the chance of a hung Parliament, which could have prolonged the uncertainty surrounding Brexit.

Of course, uncertainty still remains. While the UK formally left the EU in January, the two parties still must negotiate their future trading relationship by the time fireworks once again light up the River Thames at the dawn of 2021. A no-deal Brexit would provide a substantial negative shock to merchandise trade because dealings with the EU would revert to the most-favoured-nation rules of the World Trade Organization. Trade in financial services, a category critical to the UK’s economic well-being, would be saddled with increased regulations, paperwork and costs.

It continues to be our working assumption that a no-deal Brexit will be avoided, although it may take an extension of the transition period to effect a deal that minimises the disruption. With that said, Boris Johnson already announced his intention to exit the transition period at the 31 December 2020 deadline.

For Europe, we accurately anticipated a further slowdown in economic growth over 2019. We think it may now make sense to look past the current gloom when it comes to Europe. The lessening of trade tensions should provide export-dependent Europe with a moderate boost in 2020.

Government policy also is geared toward encouraging growth. There are signs that ECB policy is having some positive impact. The banking system is slowly recuperating. Lending to households and businesses has been in a modestly accelerating trend over the past few years. There also is more serious discussion nowadays about easing fiscal policy. Even Jens Weidman, President of the Deutsche Bundesbank, member of the Governing Council of the ECB, and a long-time hawk, has recently felt comfortable backing calls for government spending. Perhaps there’s hope that fiscal policy will turn into a tailwind for eurozone growth instead of a steady headwind.

Our expectation that emerging-market economies would enjoy a decent 2019 didn’t pan out. First, we thought an economic turnaround in China was just around the corner. The country had been pushing through various monetary, fiscal and structural reform measures aimed at jumpstarting economic growth, and we assumed that the Chinese government would go back to the debt well if needed. This happened only to a limited extent.

We have frequently made the argument that an all-encompassing trade war between China and the US would be in neither countries’ interest. The economic and political reverberations would simply be too painful. And so, the agreement on a “phase-one” deal at least helps lower the temperature and halts the tit-for-tat tariff escalations. We expect the truce will hold through the 2020 US presidential election.

Looking at the big picture for the year ahead, we anticipate continued growth for the US and global economies, but at a sluggish pace. This should keep inflation under control and encourage central banks to remain accommodative. Quantitative easing also should help keep fixed-income yields relatively steady even as government deficit spending picks up. Altogether, this scenario should be positive for risk assets.

We’ve summarised the major themes and outstanding questions that could cause markets to behave in ways that run counter to our positioning in 2020:

- The US is converging with the rest of the world as US economic and profits growth decline. Given the disparity in stock-market valuations, international markets can be expected to outperform US equities.

- The partial US/China trade-war truce and a steady progression of fiscal and monetary stimulus measures over the past two years should pay off in 2020. Early signs of improvement are already apparent, which should boost the prospects of trade-dependent economies, notwithstanding the pressures created by efforts to contain the coronavirus outbreak.

- The US dollar should reverse convincingly to the downside. The Fed’s pivot toward an aggressive approach to supporting the overnight lending market has the potential to significantly increase the global supply of dollars. Since we believe the dollar is overvalued on a fundamental basis, its depreciation is a high-conviction call. This would be a tailwind for non-US economies and financial markets.

- The value style should prevail. Modest improvement in global economic growth, a tendency for inflation and interest rates to move higher and the record disparity in valuation between the most- and least-expensive stocks should lead to a stronger result for value-oriented active managers.

- We foresee less Brexit uncertainty, assuming a trade deal can be reached between the EU and UK. We expect rationality to prevail, but a no-deal Brexit remains a residual risk. As the year-end 2020 transition deadline nears, UK and European markets could experience renewed volatility if the negotiations appear to be foundering on irreconcilable differences.

- Presidential politics could roil equity markets in the US and elsewhere. A sense of which Democratic nominee will face Donald Trump in the coming US presidential election should get clearer in March, when 25 states and Puerto Rico go to the polls; California and Texas, plus 12 other states, will hold their primary elections on Super Tuesday, 3 March.

- The impact of Fed policy is a potential wildcard. While we don’t see it as a likely outcome, the central bank’s dovish stance at a time of full employment could cause a “melt-up” in stock prices.

Even at low interest rates, we would consider a forward-earnings multiple on the S&P 500 Index of more than 20 times as a danger sign. In our view, another stellar year for US equities in 2020 would be a source of concern rather than celebration. Equities and other risky assets are not well-correlated with the fundamentals in the short run. Investor expectations can change much more quickly and far more dramatically than the fundamentals. Indeed, as seen in the past two years, changes in investor expectations can sometimes completely negate the change in the fundamentals.

With that in mind, we will retain our emphasis on strategic investing over tactical moves. We will also continue to take stock of the economic and financial developments around the globe and provide our thoughts on where global growth and interest rates are headed. That’s actually the easy part, as the experience of the last few years illustrates. Figuring out how investors might react to the shifts in macroeconomic conditions is almost always the much harder exercise.

Glossary of Financial Terms

Dovish: Dovish refers to the views of a policy advisor (for example, at the Bank of England) that are positive on inflation and its economic impact, and thus tends to favour lower interest rates. Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.