Monthly Market Commentary: New Leadership Faces Old Problems

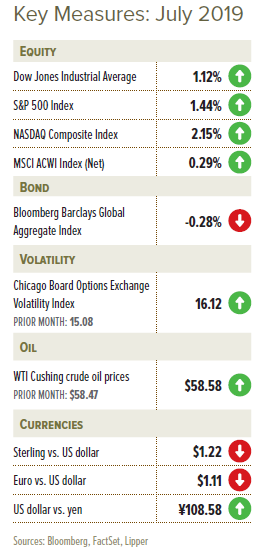

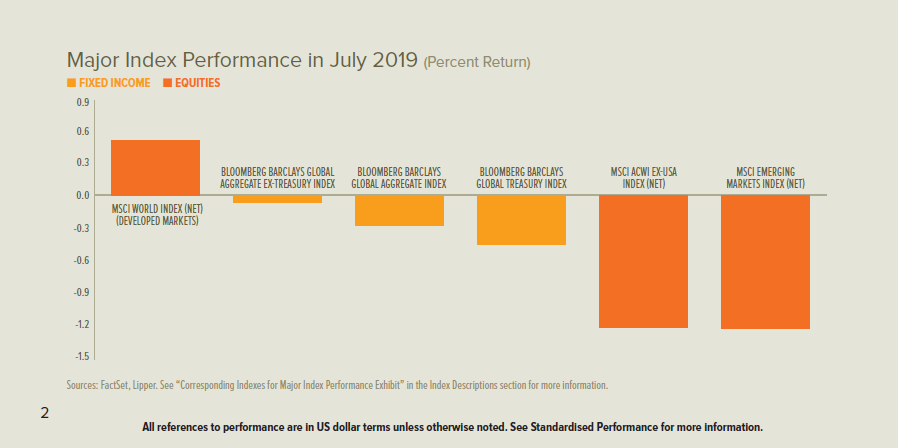

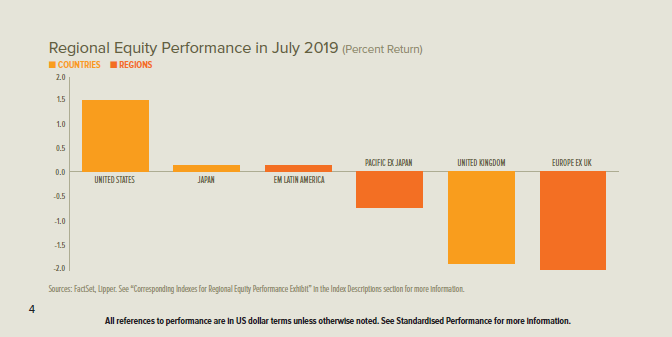

Developed-market stocks crept higher in July, while emerging markets slid amid continued signs of slowing global economic growth. Regionally, the Middle East delivered some of the best country-level returns1 —Turkey and the United Arab Emirates were the month’s top performers; Israel and Qatar also registered among the best returns—while Europe and Asia lagged the rest of the world.

Government bond rates declined across all maturities in the UK and eurozone during July. The shortest-maturity US Treasury rates fell, while short-to-intermediate-term rates increased, reducing (but not eliminating) the yield-curve inversion that has persisted since the spring.

Boris Johnson began serving as UK Prime Minister and leader of the Conservative Party in late July, using his new platform to double down on his campaign promise to depart the EU—with or without a Brexit deal—on 31 October. He signalled that if the EU wants to avoid a no-deal departure, the Irish “backstop” (part of the deal struck between former Prime Minister Theresa May and the EU) would need to be dropped before any substantive renegotiation could commence. EU negotiators, for their part, have expressed no plans to renegotiate the withdrawal agreement struck with Johnson’s predecessor.

In mid-July, European Parliament approved Ursula von der Leyen—a long-time cabinet member in German Chancellor Angela Merkel’s government—to succeed Jean-Claude Juncker as president of the European Commission beginning in November. Earlier in the month, David Sassoli, an Italian member of European Parliament, was elected and immediately began to serve as president of the EU’s legislative body. The European Council selected Belgian Prime Minister Charles Michel to succeed Donald Tusk as its next president later this year; it also appointed Christine Lagarde, chairman and managing director of the International Monetary Fund, to follow Mario Draghi as president of the European Central Bank (ECB) before year end.

Top-level US negotiators wrapped up recently-resumed trade talks with China at the end of July. US President Donald Trump announced on 1 August that the US will impose 10% tariffs on $300 billion of Chinese goods beginning in September, essentially covering all remaining yet-to-be-tariffed imports. China responded that it will retaliate if the tariffs are enacted, but the uneven trade relationship leaves a limited pool of US exports to China that can be tariffed (although China allowed the yuan, its currency, to depreciate in early August as a countermeasure). The US Congress approved a two-year budget agreement in late July, as was expected given sufficient bipartisan support for the deal.

Trade relations between Japan and South Korea began to deteriorate in July when Japan tightened exports on input materials critical to South Korea’s technology hardware industry. By the beginning of August, each country downgraded the trade-relationship status of the other in an effort to impose hurdles that could put pressure on commerce.

Central Banks

- The Bank of England’s Monetary Policy Committee held no meeting during July. Its announcement on 1 August kept policy unchanged and retained a Brexit-contingent preference for tighter policy.

- The ECB made no immediate changes during its late-July meeting. However, it announced a willingness to consider pushing benchmark rates further into negative territory and a need to explore options that could lead to a new asset-purchase programme.

- The US Federal Open Market Committee (FOMC) voted during its late-July meeting to cut to the federal-funds rate 0.25%, as was widely anticipated, but signalled in its announcement that the cut should be interpreted as a mid-cycle adjustment rather than the beginning of an easing cycle. The dovish turn also involved an early conclusion to its balance-sheet reduction programme, which was originally scheduled to end in September. These accommodative actions came amid below-target inflation and uncertainty about trade developments.

- The Bank of Japan announced no changes to its monetary policy following its meeting at the end of July.

Economic Data

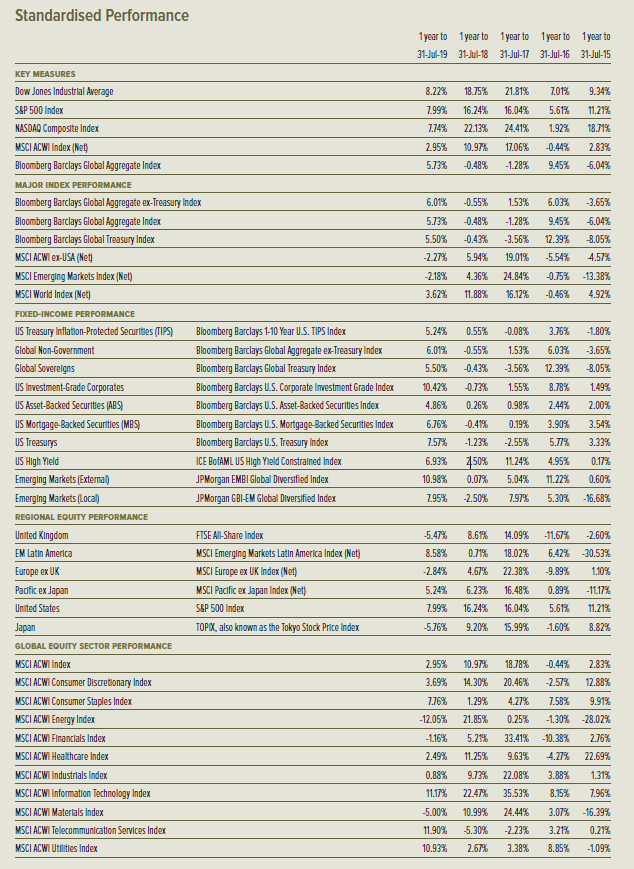

- UK manufacturing conditions contracted at the same pace in July as it did in the prior month, while activity in the services sector remained at a standstill. The UK claimant-count unemployment rate increased 0.1% to 3.2% in June; during the March-to-May period, average yearover- year earnings expanded from 3.1% to 3.4% and the UK unemployment rate held at 3.8%.

- Eurozone manufacturing contracted further during July, clocking its sixth straight month of recession. Services sector activity continued to expand at a moderate pace. Labour-market conditions were unchanged in June, with the eurozone unemployment rate holding steady at 7.5%. Eurozone economic growth was halved during the second quarter to a pace of 0.2%, causing the year-over-year rate to slow 0.1% to 1.1%.

- US manufacturing conditions eased firmly into modest expansion territory during July, while services sector activity accelerated to slow-but-healthier levels. The US unemployment rate held firm at 3.7% in July, near a 50-year low, and the labour-force participation rate increased to 63% as US employers continued to hire workers at a moderate pace. US economic growth measured an annualised 2.1% during the second quarter, down from 3.1% in the first quarter.

SEI’s View

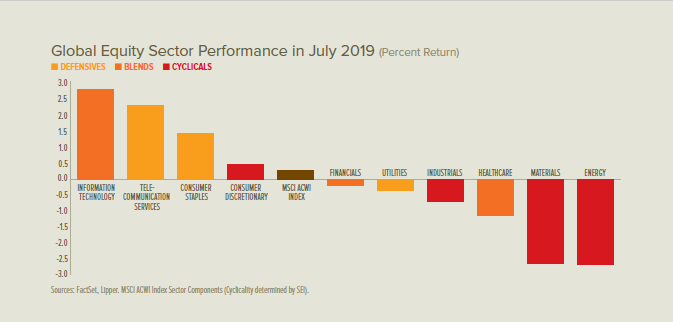

July marked the tenth anniversary of the US economic expansion. The bull market in the S&P 500 Index reached its tenth birthday in March, and it appeared to be celebrating this achievement by moving into new-high territory through late July. But there now seems to be anxiety that the bull market in equities is on its last legs, the victim of a slowing global economy, the lagged impact of last year’s US interest-rate increases and, perhaps most importantly, a worsening trade war between the US and China.

To be sure, the US economy is hardly firing on all cylinders. There’s a good chance that capital spending will continue to ease in the months ahead, but we’re not forecasting a major downturn. Corporate cash generation continues to run slightly ahead of capital expenditures. The main point to remember: It’s not unusual for capital expenditures to run well in excess of cash flow, especially toward the end of the economic up-cycle. And that’s not happening yet.

We need to see a severe deterioration in financial and leading economic indicators before climbing onto the recession train. Even after the past two years of multiple Fed rate increases, there are still few signs of a build-up in financial stress.

The big unknown, of course, is how the evolving tariff war between China and the US will affect US economic growth and global trade in the months ahead. Tariff tensions and worries about global growth have put only a modest dent in the confidence of American businesses so far, but it certainly looks as if the US-China trade relationship is getting frostier.

It is our view at SEI that the US economy should be able to weather this storm. An all-out tariff war between the two largest economies in the world will certainly disrupt supply chains and likely lead to higher prices for a broad range of consumer goods. Still, we think it helps to keep the problem in perspective. Even if the US imposes a 25% tariff on all Chinese imports, total duties will amount to roughly 0.5% of US gross domestic product, according to our calculations of data provided by the U.S. International Trade Commission.

It is not our intention to minimise the importance of the shift in US trade policy toward protectionism. The speed and ease with which supply chains can be relocated to other countries will be a critical factor, either exacerbating or tempering the tariff impact on consumers and companies in both the US and China. An escalation of the trade wars by the US against other countries would prove far more dangerous for the near-term growth prospects in the US than if trade were disrupted only with China.

We have been thinking that the US would avoid waging multiple tariff wars as it concentrated its firepower on China. But our persistent optimism may not hold. Tariffs on German and Japanese autos are still a possibility later this year.

In all, we think the US economy will show resiliency in the face of what is admittedly a stiff headwind. Household income growth has continued to advance at a good pace. The decline in US interest rates that began late last year should certainly help consumers.

The market-implied rate (based on federal-funds futures contracts as at 1 August) projects a federal-funds rate of 1.65% by the close of 2019, according to the CME Group, consistent with two additional 25 basis-point cuts. Although the forecasts of FOMC members have been more cautious, they are moving in the direction of the markets. The recent decline in bond yields to levels last seen in 2016 ranks as one of the biggest surprises of the year. We find it hard to justify these moves. In our view, recession is not likely without a severe policy mistake, such as fighting a tariff war on multiple fronts.

When one considers all the headwinds facing emerging economies—a significant slowdown in Chinese economic growth, on-going trade tensions between the US and China, weak commodity pricing, and a still-resilient US dollar—it’s surprising that emerging stock markets have appreciated at all this year.

Europe currently faces a variety of idiosyncratic challenges, both economic and political, that makes it hard for even contrarian investors to get terribly enthusiastic about the near term. Economically, the downward trajectory is similar to that of the 2011-to-2012 period amid the region’s periphery debt crisis. This time, however, Germany’s industrial economy is fully participating in the slowdown.

It’s not just the region’s heavy exposure to manufacturing and international trade that makes German industrialists glum. There is also a worrisome vacuum of political leadership. Chancellor Angela Merkel is on her way out, and a politically distracted Germany is a concerning issue given the country’s central importance in the eurozone and EU.

At the supra-national level, Christine Lagarde will succeed Mario Draghi as president of the ECB and is expected to maintain the dovish policies of her predecessor. But unconventional monetary policy in the form of negative European interest rates, quantitative easing and term lending facilities do not carry a lot of punch nowadays. An aggressive easing of fiscal policy makes sense, but that strategy is a non-starter in the eurozone. Once again, the structural flaws of the eurozone are coming to the fore.

And then there’s the looming cloud of Brexit. Although it has been delayed until 31 October, there is little sign that the breathing space will be put to good use. It’s hard to see how Boris Johnson’s ascension to the role of prime minister improves the chances of an orderly exit.

Although economic growth is sluggish, the UK economy is not exactly cratering as the deadline approaches. In fact, the UK unemployment rate fell to a multi-decade low. The eurozone also recorded steady labourmarket improvement; the jobless rate itself remained far higher, owing to structural factors.

That said, we can’t help but think Brexit (if it indeed occurs) will prove to be a highly disruptive event for the UK and the EU. Roughly half of the UK’s trade in goods, imports and exports, is with the EU.

We think there is still life in the economic expansion, both in the US and globally. If we’re right, that means corporate profits should continue to expand and push global stock markets to higher levels in the months ahead. This may seem like a bold statement at a time when the world appears increasingly unpredictable and the economic data point to slowing growth. Yet we simply do not yet see the economic imbalances or nosebleed equity-market valuations that normally bring on recessions and an associated contraction in earnings and stock prices. It is also clear that central banks have investors’ backs as monetary policymakers promise to (or already are) cutting interest rates in various parts of the world and providing additional liquidity to their banking systems in both developed and emerging countries.

Glossary of Financial Terms

Dovish: Dovish refers to the views of a policy advisor (for example, at the Bank of England) that are positive on inflation and its economic impact, and thus tends to favour lower interest rates.

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Quantitative easing: Quantitative easing refers to expansionary efforts by a central bank to help increase the supply of money in the economy.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publiclytraded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.