Monthly Market Commentary: Markets Tumble as New Variant Complicates Return to Normal

Global equities started November on promising footing. Shares advanced for the first week, then treaded water through mid-month before declining, modestly at first, and then sharply during the last week.

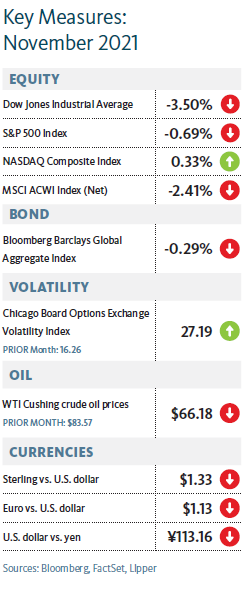

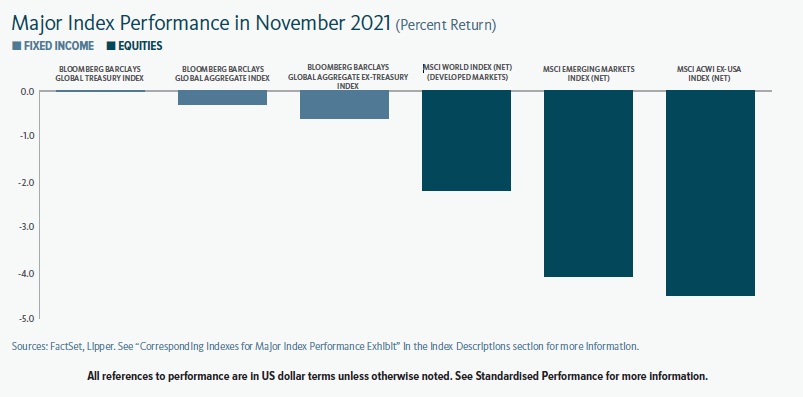

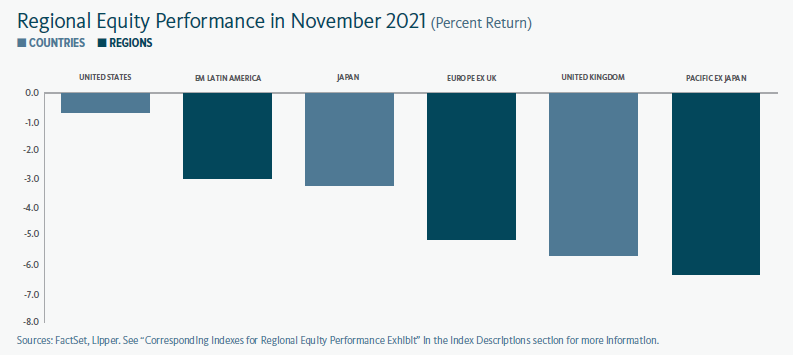

Developed-market shares continued to perform better than emerging markets. China, Hong Kong, the UK and Europe sustained sharp one-month drops. Japan’s losses were less severe, and the slide in US shares was mild compared to other major markets.

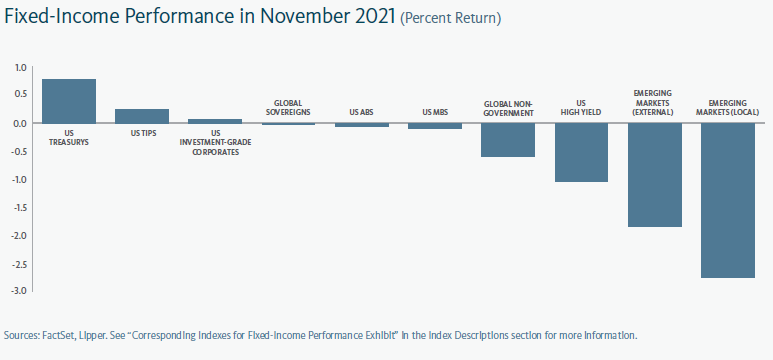

Government-bond rates declined across all maturities in the UK and eurozone; yields went negative on eurozone bonds with maturities all the way out to 30 years (negative yields were out to 12 years at the end of October). Short-term US Treasury rates increased, while intermediate-to-long-term rates declined, resulting in a flatter yield curve. Treasurys were the best-performing fixed-interest segment, while emerging-market debt continued to sustain the deepest losses1.

Commodity prices reversed lower in November. The Bloomberg Commodity Index was mostly flat until a selloff during the last week of the month, finishing November down 7.3%. Crude oil prices moved slightly lower throughout the month, and then similarly tumbled to end the month. The West Texas Intermediate crude oil price dropped 20.8% in November, while the price of Brent crude fell by 17.3%2.

Emergence of the omicron coronavirus variant in southern Africa was a key factor in rattling investors as November progressed3. Omicron appears to contain significantly more mutations than other variants, which could potentially make it more effective in sidestepping neutralisation by antibodies generated from earlier infections and vaccinations.

The US reported the highest country-level number of new COVID-19 infections per day at the end of November, followed by Germany, the UK, France and Russia. Daily deaths associated with COVID-19 were highest in Russia, then the US, Ukraine, India and Poland4.

Vaccination drives mirrored share performance in November: the UAE, Cuba and Chile have the highest population shares with at least one dose of vaccine5. The two best-performing country-level equity performances for the month were the UAE and Chile.

Chancellor of the Exchequer Rishi Sunak faced scrutiny from UK House of Commons Treasury Committees at the beginning of the month for tax increases included in his Autumn Budget. He contended that the revenue raisers—including a 1.25% bump in national insurance contributions set to begin in the spring, as well as a long-telegraphed increase in the corporations tax—are needed to fund necessary spending and intended to be temporary.

The cost side of the budget included a notable pair of adjustments for low-income workers: a reduction in the universal credit’s taper rate (from 63% to 55%, meaning that the credit will phase out more slowly) and an annual £500 increase in work allowances. Brick-and-mortar stores will also see more relief via a temporary 50% cut in business rates and no increase in 2022.

Germany’s new governing coalition came together in late November. The centre-left Social Democrats (SPD, with 25.7% of the September election’s vote share) will work with the progressive environmentalist Greens (14.8%) and pro-business Free Democrats (FDP, 11.5%). SPD leader Olaf Schultz will head the government as chancellor, while Christian Lindner, the FDP’s leader, will serve as finance minister.

The coalition’s policy pledges include a hefty environmental agenda, including an accelerated coal phase out, greater reliance on rail transport, an ambitious goal for electric vehicle adoption, and the promotion of an EU-wide air travel surcharge. An increase in the minimum wage, plans to construct 400,000 apartments per year, and reforms to the immigration and citizenship eligibility system also made it to the top of the agenda.

Germany’s “debt brake” will be re-instated in 2023, limiting government borrowing to 0.35% of GDP, and the FDP extracted a commitment to no new taxes or tax increases in order to join the coalition, raising a question about how the government will fund its goals.

For the second time this fall, US Congressional negotiators appeared on the verge of a last-minute agreement to fund the government in early December ahead of a funding lapse that would otherwise take effect on 4 December. The agreement, which has already passed the House of Representatives, would provide funding through mid-February.

Economic Data

UK

- The expansion in UK manufacturing activity held in November at a strong pace of growth6.

- Services growth settled slightly lower in November, but remained quite robust7.

- The UK claimant count (which calculates the number of people claiming Jobseeker’s Allowance) declined further in October by roughly 15,000, lowering the claimant share of the population from 5.2% to 5.1%.

- The UK economy expanded by 0.6% in September, improving on August’s more modest growth and nearing its pre-coronavirus level of economic activity.

Eurozone

- Growth in eurozone manufacturing activity continued during November in line with the robust pace of the prior two months8.

- Eurozone services growth strengthened in November after slowing in October9.

- The eurozone unemployment rate continued to decline in September, hitting 7.4%.

- The overall eurozone economy expanded by 2.2% in the third quarter, in line with the second quarter’s 2.1% rate.

US

- The US manufacturing expansion continued at a high pace in November10.

- Services activity remained strong during the month despite moderating after October’s sharp acceleration11.

- New weekly US jobless claims held just below 270,000 for most of November before declining to 199,000 later in the month, the lowest level since 1969.

- The broad US economy grew at a 2.1% annualized rate during the third quarter, down from the second quarter’s 6.7% pace.

Central Banks

- The Bank of England’s Monetary Policy Committee left its policy orientation unchanged at its early-November meeting, with the bank rate remaining at 0.1% and the maximum allowance for asset purchases at £895 billion. The central bank’s November report on monetary policy upgraded its inflation forecast to peak at 5% in spring 2022, and indicated that a rate hike would be necessary if its economic outlook comes to pass.

- The European Central Bank (ECB) did not hold a meeting on monetary policy during November and continued to pursue a moderately lower pace of net asset purchases under the pandemic emergency purchase programme (PEPP) than the target of approximately €80 billion per month that prevailed over the summer. The European Commission’s Autumn Economic Forecast, released in November, showed inflation projections above the ECB’s 2% target in 2021 and again next year, with import prices contributing steeply and compensation to a lesser extent.

- The US Federal Open Market Committee (FOMC) announced a long anticipated timetable to reduce its asset purchase programme following its early-November meeting. The central bank will shrink its monthly asset purchases by $15 billion—split between a $10 billion reduction in US Treasury purchases (from purchases of $80 billion per month in October) and $5 billion in agency mortgage-backed securities (from purchases of $40 billion per month in October)—in November and again in December. Reductions were expected to continue until asset purchases conclude altogether in June 2022, although the pace can be adjusted “if warranted by changes in the economic outlook.” At the end of November, in testimony to the U.S. Congress, Federal Reserve (Fed) Chair Jerome Powell expressed that high inflation could drive the FOMC to reduce asset purchases at an accelerated pace and conclude the programme a few months earlier than planned. Powell was nominated for a second term as Fed Chair by President Biden during the month.

- The Bank of Japan (BOJ) did not hold a monetary policy meeting during November. Its short-term interest rate remained at -0.1% and its 10-year government bond yield target held near 0%, while continuing open-ended asset purchases. The central bank downgraded its near-term consumer inflation forecast in its latest quarterly economic outlook.

SEI’s View

Recent gloom about flagging economic growth is likely a bit overdone. We expect economic growth—in the US and globally—to continue over the next year or two at a pace that meaningfully exceeds the sluggishness of the years that followed the 2007-to-2009 global financial crisis.

Household wealth is at an all-time high, owing to booming stock and home prices12. A big decline in the saving rate has helped cushion the blow to consumer spending; still, saving as a percentage of disposable income remains elevated compared to pre-pandemic levels. We think households generally can adjust to a decline in pandemic relief payments without necessitating a sharp contraction in their expenditures.

The impact of COVID-19 on global supply chains has been a more significant impediment. Vendor deliveries have seldom been as slow in the 74-year history of the Institute for Supply Management’s (ISM) survey as they are now, even with the situation having eased slightly since May. Inventories remain exceedingly low relative to demand.

Input costs have been rising rapidly, but companies have been able to compensate by passing along their increased costs to customers. Corporate pricing power is the good news. The bad news is that inflation keeps exceeding consensus expectations. We still expect inflation to run at a higher rate for a longer period than has been commonly assumed, not just over the next one or two years, but well into the decade.

Growth in unit labour costs typically plummets when the economy emerges from recession. Now, however, unit labour costs are running at the fastest pace since the peak of the 2002-to-2007 expansion13.

While commodity inflation and parts shortages may indeed prove transitory, it isn’t clear whether the labour shortage and resultant pressure on compensation growth will be as quick to revert to lower levels. The tax and regulatory initiatives of the Biden administration will likely add to the cost pressures facing businesses in the years immediately ahead.

Since US demand is expected to remain robust as economic growth normalises, it would not be surprising to see companies continue passing along their increased costs. Inflation over the long haul could thus be closer to 3% than the 2% or so currently expected by the Fed and most investors.

If that turns out to be the case, the Fed may be forced to raise interest rates higher and faster over the next three years than anticipated.

A concern that is much nearer in timeframe is the fight in Washington over infrastructure spending and the debt limit. We assume President Biden will get about half of what he is seeking, but the devil will be in the details. Investors are probably right not to react too dramatically to every development. The debtlimit drama, however, could elicit a more significant disruption as the deadline for must-pass legislation nears (again, after earning a temporary reprieve). Although the debt ceiling will be raised, the wrangling over it will almost certainly come down to the wire.

We suggest focusing on longer-term considerations: Economic growth should stay relatively strong in 2022. Households are in solid financial shape and will benefit as employment and wages continue to move higher. Companies are still able to pass along increased costs and maintain high profit margins. Fed policy is still biased toward accommodative credit conditions via ultra-low rates and asset purchases. This should all create a favourable backdrop for risk assets and support a resumption in the coming months of the cyclical/financial/value trend versus growth/technology.

Other developed countries are broadly on the same path as the US, and are reacting to the same catalysts.

Purchasing managers’ surveys from recent months show that US economic growth is still strong versus pre-pandemic levels. Activity in Europe, led by Germany, appears to be on the upswing—boosted by a decline in Delta (which has allowed for more travel and tourism in Europe) and an increase in EU fiscal support.

The major outlier is Japan, which has been rather weak so far this year versus its industrial-country peers. Inflation-adjusted GDP fell in the first quarter and posted only a tepid gain in the second quarter. Economists blame COVID-19- related restrictions. The global shortage in the supply of semiconductor chips, meanwhile, has impeded auto production. Citizens nonetheless blamed Prime Minister Yoshihide Suga. In response, he has been succeeded as prime minister and leader of the Liberal Democratic Party (LDP) by former foreign minister Fumio Kishida. The LDP retained a comfortable majority in a 31 October election, cementing Kishida’s leadership.

US inflation may be near a peak, but a further acceleration appears in store for Europe. The immediate concern for households in the region is the cost of energy. Even without energy-production shortages, electricity prices across Europe tend to be much higher than in North America—especially for households, particularly in Germany.

Europe’s energy woes probably won’t cause the region’s governments to deviate from the climate-change agenda they have put in place. The German election underscores this point, as parties from across the political pectrum all committed to reducing carbon emissions.

Beyond energy, Europe’s reopening should cause the price of services to rise as they have in the US, albeit to far less of an extent. The overwhelming assumption is that any pickup in inflation will be short-lived.

China is dominating investor perceptions of emerging markets. The Xi government’s push to enforce “common prosperity” has had far-reaching effects on corporate China. The country’s 20-year boom has exacerbated social inequality. Crackdowns on for-profit tutoring companies, major gig employers, and individuals (notably, Jack Ma, the founder of e-commerce giant Alibaba and digital payments company Ant Group) is a brutal but effective way of addressing disparities in wealth and income.

Although some of these moves have hurt foreign equity investors, it’s unclear whether the economy itself will be severely constrained. China is a huge country with tremendous internal capital upon which to draw. Foreign companies probably won’t cut and run, but they will certainly be forced to play by Beijing’s rules if they stay.

We expect diversification of supply chains away from China at the margin, but this has been happening anyway. It is in advanced countries’ interests to be more self-sufficient in producing critical products. But China is too big, too efficient and too important a manufacturer for the world to turn its back on.

China’s economic growth rate should nevertheless slow as a result of the government’s actions. Property development has been the driving force behind its rapid expansion over the past 15 years. Critics of China’s economic model have wondered for years if the bill would ever come due.

It might be coming due now. We are watching the trend in commodity prices for hints that pressure on China’s construction activity is beginning to reverberate beyond its borders. So far, there has been little sign of that occurring. Iron ore prices have plunged, but that appears to have been caused primarily by government-mandated closures of steel plants in an effort to curb pollution.

Even within China itself, investors seem to be taking the Evergrande debacle in stride. The effective yield on the country’s high-yield bonds has been rising sharply since May, but it is nowhere near the 40% yield reached in 2008. In contrast to high yield, the yield on Chinese investment-grade bonds is currently at its lowest level in the past 20 years—indicating no sign of contagion14.

One explanation for the resiliency of the MSCI Emerging Markets Index is the strength of the global economy outside China. The US has been leading the way, but other advanced countries—notably Europe—continue to post improved economic activity.

If history is any guide, however, upside inflation surprises in the G-10 countries suggest that emerging economies will follow suit over the next few months. Unlike advanced countries, where inflation expectations tend to better anchored, central banks in vulnerable emerging economies are forced to raise interest rates sooner than they would prefer in order to dampen inflation pressures and defend their currencies.

Given these concerns, investors might be tempted to avoid emerging-market equities. We believe that would be a mistake. Valuations, particularly relative to the developed world, look especially cheap.

Globally, the earnings of publicly traded companies generally remain robust; we believe that analysts are still underestimating that strength. With the exception of Japan, earnings estimates for 2021 have been raised dramatically versus just six months ago. Forecasts for 2022 earnings have been cut in half from where they were six months ago, but they still are expected to show mid-to-high single-digit gains.

This lowering of the bar for next year could allow for upward revisions in analysts’ earnings estimates—assuming, as we do, that the renormalisation of global economic growth gets back on track with wider vaccine distribution.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Cyclical stocks: Cyclical stocks or sectors are those whose performance is closely tied to the economic environment and business cycle. Managers with a pro-cyclical market view tend to favour stocks that are more sensitive to movements in the broad market and therefore tend to have more volatile performance.

Debt brake: The debt brake refers to a balanced budget amendment used by the German federal government to limit structural budget deficits to 0.35% of GDP.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Forward price-to-earnings (PE) ratio: The forward PE ratio is equal to the market capitalisation of a share or index divided by forecasted earnings over the next 12 months. The higher the PE ratio, the more the market is willing to pay for each dollar of annual earnings.

Group of Ten (G-10): The G-10 is a group of countries that agreed to participate in the General Arrangements to Borrow (GAB), an agreement to provide the International Monetary Fund (IMF) with additional funds to increase its lending ability. G-10 members include Belgium, Canada, France, Germany, Italy, Japan, Netherlands, Sweden, Switzerland, United Kingdom and United States.

Hawk: Hawk refers to a central-bank policy advisor who has a negative view of inflation and its economic impact, and thus tends to favour higher interest rates.

Inflation-Protected Securities: Inflation-protected securities are typically indexed to an inflationary gauge to protect investors from the decline in the purchasing power of their money. The principal value of an inflation-protected security typically rises as inflation rises, while the interest payment varies with the adjusted principal value of the bond. The principal amount is typically protected so that investors do not risk receiving less than the originally invested principal.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Mortgage-Backed Securities: Mortgage-backed securities (MBS) are pools of mortgage loans packaged together and sold to the public. They are usually structured in tranches that vary by risk and expected return.

NextGenerationEU: NextGenerationEU is an economic recovery fund established by the EU and totalling more than €800 billion projected to be spent between 2021 and 2027. The centrepiece of the programme is a €723.8 billion facility for loans and grants to EU countries for investments.

OPEC+: OPEC+ combines OPEC—a permanent intergovernmental organisation of 13 oil-exporting developing nations that coordinates and unifies the petroleum policies of its member countries—with Russia, a major oil exporter, to make collective high-level decisions about oil production levels.

Open-ended asset purchases: This type of programme refers to a central bank’s policy of purchasing assets (typically centred on government bonds but also potentially including private-sector securities) without a defined upper limit.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset-purchase programme of private and public sector securities established by the European Central Bank to counter the risks to monetary-policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Recession: A recession is a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Sovereign: A sovereign refers to government-issued debt.

Summary of Economic Projections: The Fed’s Summary of Economic Projections (SEP) is based on economic projections collected from each member of the Fed Board of Governors and each Fed Bank president on a quarterly basis.

Taper tantrum: Taper tantrum describes the 2013 surge in US Treasury yields resulting from the US Federal Reserve’s announcement of future tapering of its policy of quantitative easing.

Transitory inflation: Transitory inflation refers to a temporary increase in the rate of inflation.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Index Descriptions

The Bloomberg Commodity Index is composed of futures contracts and reflects the returns on a fully collateralised investment in the Index. This combines the returns of the Index with the returns on cash collateral invested in 13-week (3-month) US Treasury bills.

The Employment Cost Index is a quarterly economic series published by the US Bureau of Labor Statistics that details the growth of total employee compensation. The index tracks movement in the cost of labour, as measured by wages and benefits, at all levels of a company.

The ICE BofA Investment Grade Emerging Markets Corporate Plus China Issuers Index tracks the performance of US dollar and euro denominated emerging markets non-sovereign debt publicly issued within the major domestic and Eurobond markets. The investment grade rated bonds of qualifying Chinese issuers must have at least 250 million (Euro or USD) in outstanding face value for inclusion in the index.

The MSCI Emerging Markets Index is a free float-adjusted market-capitalisation-weighted index designed to measure the performance of global emerging-market equities.

The MSCI USA Index measures the performance of the large- and mid-cap segments of the US market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.