Monthly Market Commentary: Markets Thaw despite Showdowns and Shutdowns

Economic Backdrop

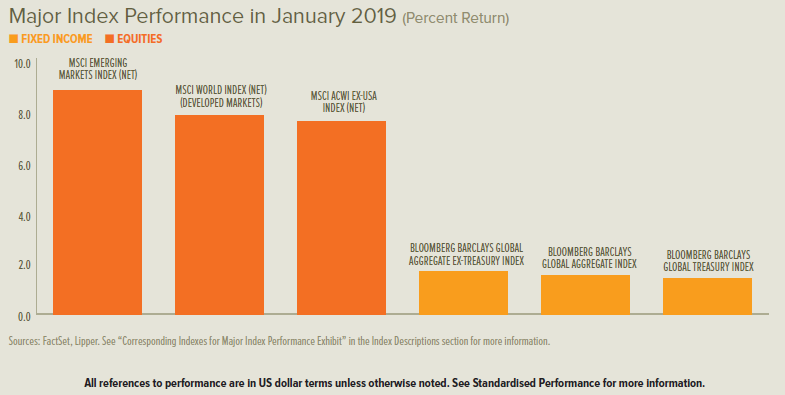

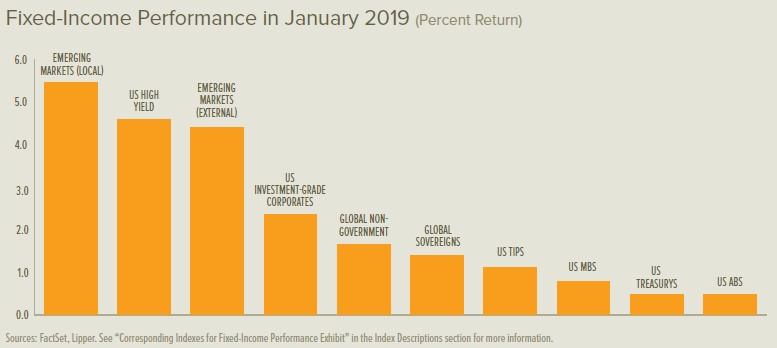

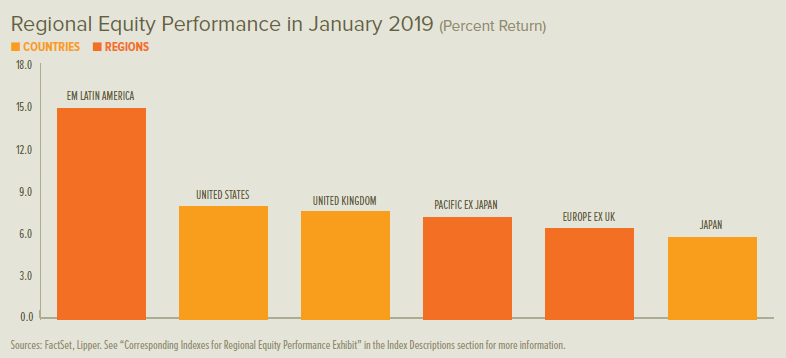

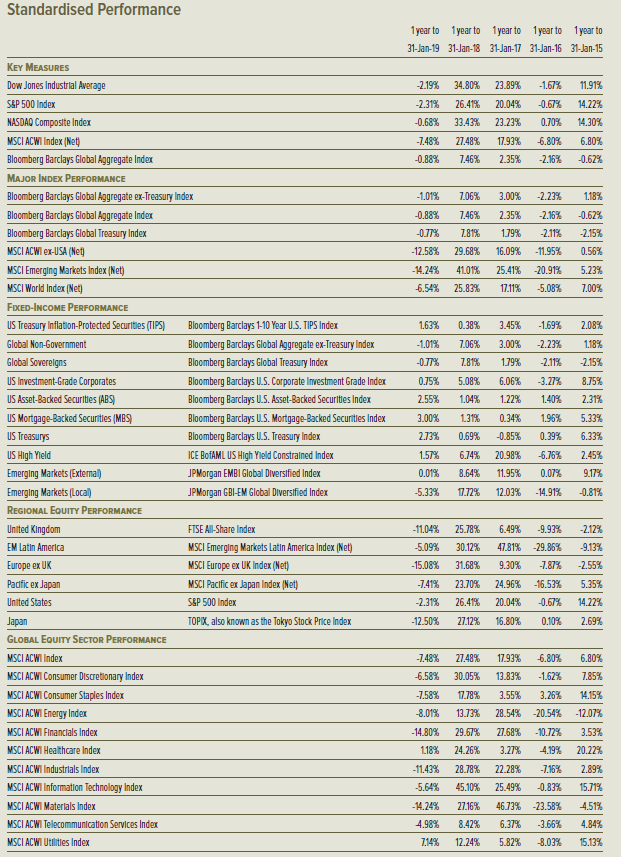

The New Year provided an occasion to break with the negative trend that defined financial market conditions during the final quarter of 2018. Riskier assets led a worldwide rally that generally persisted throughout January, while oil prices increased and stock-market volatility settled down. Sterling and the euro strengthened relative to the US dollar, which retreated versus a broad trade-weighted basket of foreign currencies. Emerging markets, particularly those in Latin America, were the top performers in equity and fixed-income markets (see performance exhibits on pages 2 to 4).

Government bonds had positive performance, but still generated some of the weakest returns among asset classes for the month. Interest rates declined on government bonds in the UK, Europe and US (except for short-term bonds in the UK and Europe). The short-to-intermediate-term segment of the US Treasury yield curve remained inverted throughout January.

UK Prime Minister Theresa May’s divorce agreement with the EU suffered a major defeat in Parliament on 15 January; she nevertheless survived a no-confidence motion tabled by the Labour party on the following day, thanks to Conservative members of Parliament who cast confidence votes in her favour despite their opposition to her Brexit deal. On 29 January, Parliament voted on newly proposed changes to the agreement, opposing an amendment to delay Brexit day (currently 29 March) and supporting (in a non-binding vote) an amendment that rejects a no-deal Brexit. This offered mixed signals as the Northern Ireland backstop issue remained the key sticking point. European leaders were steadfast in their unwillingness to renegotiate the agreed-upon deal.

The US government remained partially shuttered for most of January due to an impasse between Congress and President Donald Trump’s administration about whether to fund a multi-billion dollar wall on the US-Mexico border championed by the president. Trump ultimately relented (at least temporarily), enabling federal workers to receive pay again and setting up a three-week negotiation window—after which, he warned, the government may again partially shut down in the absence of an agreement. Vice Premier Liu He of China met with Trump in the Oval Office on 31 January following two days of high-level talks between Chinese and US leaders in an effort to settle their trade dispute; this came ahead of an early-March deadline for the two countries to reach an agreement before the US issues additional tariffs on Chinese goods. The only concrete concession offered by China’s delegation was to purchase several million tonnes of US

soybeans.

The Bank of England’s Monetary Policy Committee had no meeting in January and will reconvene on 7 February. The European Central Bank’s (ECB) late-January monetary-policy meeting produced no changes to its plan to maintain interest rates through at least the summer and re-invest cash flows from its asset-purchase programme through an even longer period. The US Federal Open Market Committee abstained from increasing the federal-funds rate, as expected, following its month-end meeting. The post-meeting statement took a dovish turn, notably in the omission of a phrase that previously signalled an expectation for multiple future rate hikes and a willingness to temper its balance-sheet reduction as warranted by economic or financial conditions—thereby signalling patience on the policy-tightening front and expressing a more modest perception of economic conditions. The Bank of Japan made no changes, remaining accommodative after a late-month policy meeting. The People’s Bank of China (PBOC) undertook several initiatives to increase liquidity during the month, including injecting $83 billion into the financial system through pen-market operations on 16 January; announcing the release of $37 billion to banks on 25 January following a reduction in reserve requirement ratios; establishing a new medium-term lending facility; and opening up a line to swap perpetual bank bonds for PBOC bills that can be pledged as collateral.

UK manufacturing growth slowed in January to a three-month low and services-sector growth ground to a halt, while retailers reported sluggish

conditions (albeit an improvement on December’s sharp slide). The claimant-count unemployment rate held firm at 2.8% in December, while the September-to-November unemployment rate declined to 4.0% and average year-over-year earnings growth increased to 3.4% during the three- month period.

Eurozone services-sector growth slipped and manufacturing conditions continued a six-month trend of slowing growth in January, yet both measures generated just enough gains to avoid outright slowdowns. The eurozone unemployment rate was unchanged at 7.9% in December despite the number of unemployed workers falling by 75,000 for the month. Overall economic growth registered 0.2% in the fourth quarter of 2018 and 1.2% year over year.

US manufacturing growth accelerated in the first month of the year after softening in December. Employers added more than 300,000 workers

to payrolls in January, while the labour-force participation rate expanded as the US unemployment rate increased to 4% (due in part to the partial

government shutdown). Average hourly earnings growth held firm at 3.2% year over year.

Our View

As painful as 2018 was for risk assets, their gyrations were not outside the norm. Rather, given our views that the global economy will continue to grow and that market participants are overreacting to the concerns of the day, we see another important risk-on opportunity developing in equities and other risk assets. We believe a rebalancing of assets back toward undervalued equity classes is an appropriate and timely response.

In our view, the US economic position remains fairly solid. Points of strength include the improving economic position of US households as labour markets tighten and real wage growth accelerates, while increased government spending has also helped. With Democrats controlling the House of Representatives and Republicans holding power in the Senate, any fiscal-policy agreement made during a period of political gridlock will likely mean slightly more federal-government spending—not less.

Some Federal Reserve (Fed) officials, including Chairman Jerome Powell himself, explicitly acknowledge that the federal-funds rate is now near a level that can be considered neither stimulative nor deflationary. We are pencilling in just one increase in the federal-funds rate during 2019, and perhaps one in 2020—but these are just guesses. The important thing to remember is that the central bank is adopting a wait-and-see approach to monetary policy and has ended the nearly automatic quarterly rate increases of 2017 and 2018.

We think the odds favour a strong rebound in US equity prices for the following reasons:

- The US economy should continue to grow, and corporate earnings per share are expected to post a mid-to-high single-digit gain in 2019.

- Valuations for the S&P 500 Index have declined from almost 19 times one-year forward earnings per share to an attractive level of almost 14 times following the decline in share prices.

- US bond yields remain rather low after moving down again in late 2018, bolstering the case for riskier assets.

- Investor risk aversion increased sharply in late 2018, and we think much of the bad news of recent months is reflected in current stock prices—creating space for potential upside surprises on trade wars, the Fed’s policy path, Brexit, corporate profits and elsewhere.

- We do not expect fiscal policy to be the strong catalyst for growth in the US that it was in 2018, but the impact of political gridlock should still be mildly expansionary.

As for Brexit, we believe it’s unlikely that the UK will fall out of the EU without some sort of deal in place. A no-deal divorce would deliver a mighty blow to the economy. In our view, the real choice now is between May’s Brexit deal or no Brexit at all. A no-Brexit-at-all scenario could take one of two forms. The UK government could unilaterally revoke Article 50, basically calling off the divorce from the EU. The second alternative is to go back to voters and hold a second referendum. Although the legality would be disputed, we think this is the far more likely scenario. The financial markets probably would respond quite positively to this decision, yet the next few months can still be volatile as the late-March Brexit date nears.

Although the European banking system is in better shape than it was in the immediate aftermath of the global financial crisis, it is still vulnerable at

a time when the ECB is in a holding pattern, policy-wise, and has limited flexibility in the event of a financial emergency. A lack of enthusiasm for Europe’s economic prospects is reflected in its equity-market valuations: the MSCI European Economic and Monetary Union (EMU) Index price-to earnings ratio has sunk to less than 12 times from nearly 15 times at the start of the year. Note that European equities outperformed US equities in the fourth quarter of 2018.

We are leaning on the optimistic side for emerging markets in 2019. The valuation piece is already in place, in our opinion, with the price-to- forward-earnings ratio of MSCI Emerging Markets Index collapsing from 13 times at the end of January to 10.5 by year-end. But what could be the catalyst for a turnaround? Big debt expansions in China typically lead to big gains in emerging-market equities. The question is whether the Chinese government has the will to support increased debt issuance one more time.

It surely would be a big positive for the country if the threat of tariffs was negotiated away, but we’re not holding our breath. On the contrary, the US China economic relationship will likely continue to deteriorate as the Trump administration seeks to level the playing field—even if it means a less efficient global trading system. When push comes to shove, the Chinese government will probably get even more aggressive in easing lending constraints if the situation warrants.

Commodity prices and the earnings of emerging-market companies are closely correlated in inverse fashion with the movements of the US dollar.

For most of 2018, the US dollar gained against other currencies, putting downward pressure on commodity prices and the earnings of energy and

materials companies that are a large part of the MSCI Emerging Markets Index. In 2017, the opposite conditions held.

We are looking for another change in the dollar’s trend in 2019. In our view, US economic and corporate-earnings performance will move toward that of other developed countries. If there are positive developments in some of the pressure-point issues that have roiled markets, investment capital could flow away from the US and back into the world—thereby removing an important source of support for the US dollar and a big headwind from the rest of the world. This potential for a reversal in investment flows could accelerate if Fed policy becomes more dovish than currently projected by the central bank.

The poor performance of risk assets in the fourth quarter can certainly prey on investors’ emotions. But the global economy is not exactly in dire straits. Yes, there are an unusually large number of uncertainties and concerns, some of which could have a material impact on growth if the worst comes to pass. However, even in an extraordinarily unfavourable economic scenario in which the tariff wars with China and other countries deepen

and the Fed raises the funds rate too far and too fast, we doubt that the US economy would experience anything worse than a garden-variety recession by 2021. The economic and credit excesses that usually precede a deeper recession simply aren’t to be found.

During periods of market volatility like the one we experienced at the end of 2018, investors should be mindful about the importance of sticking

with a strategic and disciplined approach to investing that is consistent with personal goals and risk tolerances. Diversification is the key to that

approach, and the construction of portfolios should be dictated by long-term capital market assumptions.

Ultimately, the value of these assumptions is not in their accuracy as point estimates, but in their ability to capture relevant relationships—as well

as changes in those relationships as a function of economic and market influences.

Glossary of Financial Terms

Dovish: Dovish refers to the views of a policy advisor (at the Bank of England, for example) who has a positive view of inflation and its economic impact, and therefore tends to favour lower interest rates.

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the Federal Reserve) to another depository institution overnight in the US.

Price-to-earnings ratio: The price-to-earnings ratio is the ratio of a company’s share price to its earnings over the past 12 months, which can be used to help determine whether a stock is under- or overvalued.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter yield curve indicates the yields are closer together.

Index Descriptions

MSCI Emerging Markets Index: The MSCI Emerging Markets Index is a free float-adjusted market-capitalisation-weighted index designed to measure the performance of global emerging-market equities.

MSCI European Economic and Monetary Union (EMU) Index: The MSCI EMU Index captures large- and mid-cap representation across the developed-market countries in the EMU.

S&P 500 Index: The S&P 500 Index is an unmanaged, market-capitalisation-weighted index comprising 500 of the largest publiclytraded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relat on to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.