Monthly Market Commentary: Markets Maintained Modest Momentum

Economic Backdrop

A late-August Brexit summit yielded little fruit, betraying a fixation by negotiators on the UK’s financial obligations to the European Union (EU). Yet the UK’s desired roadmap became clearer as summer progressed; the transitional post-divorce period could maintain the status quo in order to avoid (or at least delay) the economic pain that would come from a hard break or multiple recalibrations. The UK consensus appears to favour a multi-year transition period that retains single-market access—in return for partial EU institutional dominance (with no British votes), ongoing financial support by the UK and a grace period for the continued free movement of people. Elsewhere, French President Emmanuel Macron unveiled labour-market reforms at the end of the month that delivered on a cornerstone of his agenda; German polls depicted President Angela Merkel’s firm lead in upcoming elections; and monsoon rains flooded parts of the South Asian subcontinent, killing scores.

In the US, top-level White House departures continued amid President Donald Trump’s controversial reaction to violent protests in Virginia. His statements fanned already-heated racial tensions, caused members of his business council to resign in protest, and drew rebukes from senior advisors, cabinet officials and congressional leaders—all of which distracted from the administration’s agenda to push for tax reform. The month also brought historic hurricane rainfalls that affected millions of Americans and hobbled a crucial energy-sector hub; new revelations in the US Justice Department’s Russia-Trump campaign collusion investigation; willingness of Mexico to end trade negotiations if the US rescinds the North American Free Trade Agreement; and escalating provocations from North Korea.

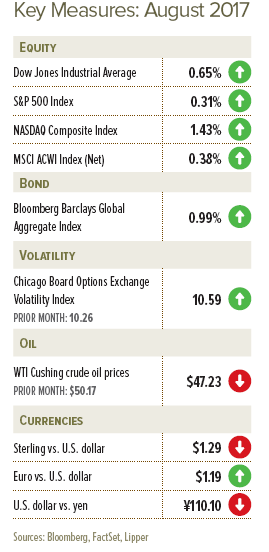

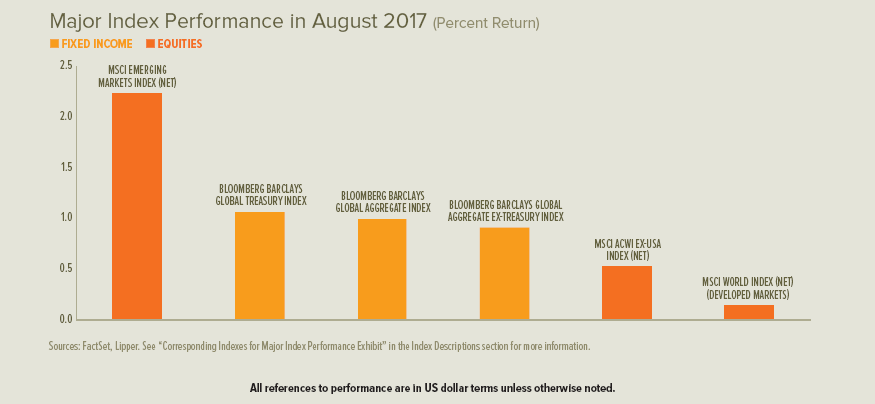

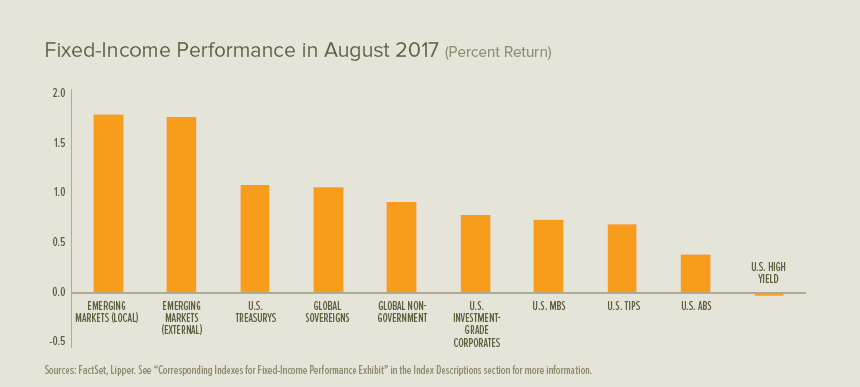

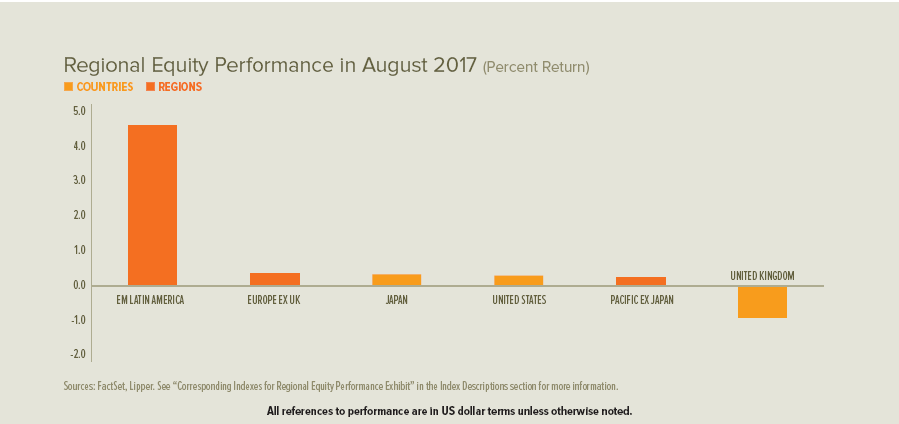

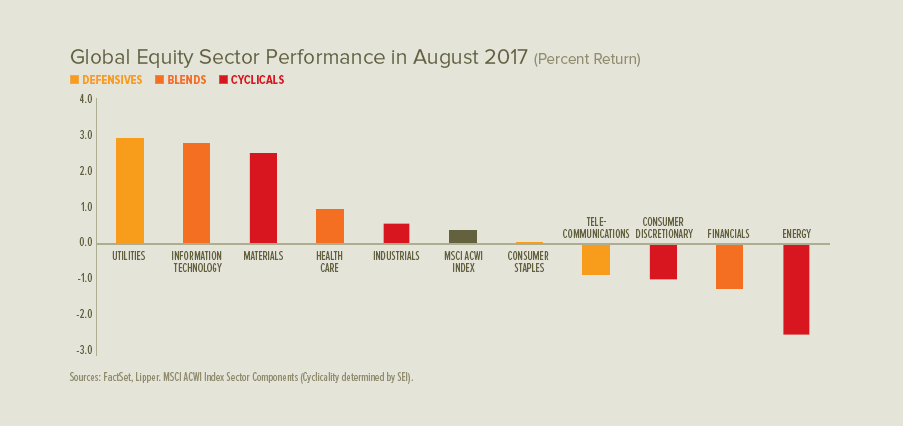

Equity markets were more directionally mixed than they’ve been in some time: the UK was down, the US, Japan and Europe were essentially flat, while China and Brazil advanced along with other emerging markets.[1] The weak US dollar trend that has remained intact for much of 2017 moderated, as the dollar strengthened against sterling and weakened only modestly versus the euro and Japanese yen. Sovereign bond yield curves flattened in the UK, eurozone and US as long-term government-bond rates fell by more than short-term rates. The 10-year US Treasury yield, which serves as a global reference for long-term sovereign rates, fell to its lowest level of 2017 on the last day of the month.

Major central banks were primarily on holiday during August, with the US Federal Reserve (Fed), European Central Bank (ECB) and Bank of Japan (BOJ) reconvening their respective monetary policy councils in September. The Bank of England’s Monetary Policy Committee voted in early August to maintain its current bank rate and stock of purchased assets. The Fed hosted the annual Jackson Hole Economic Policy Symposium, where Fed Chair Janet Yellen spoke about the role of financial regulation since the global financial crisis; ECB President Mario Draghi addressed resurgent protectionist urges of recent years, highlighting the importance of developed-market openness to trade in driving increased productivity.

UK factory orders advanced in August, reaffirming early-summer progress in the manufacturing sector. Retail conditions were somewhat less comforting, as August sales volumes fell to their lowest levels since the immediate aftermath of the Brexit vote in July 2016. The labour-market landscape continued to firm, with the claimant count declining in July, the unemployment rate ticking lower to 4.4% for the April-to-June period, and average earnings growth rising for the one-year period through the second quarter. Second-quarter economic growth was unrevised at 0.3% for the three-month period and 1.7% year over year.

Eurozone economic sentiment continued to climb in August, reaching its highest level in a decade, with notable gains in Italy, France and Spain as economic recovery continued to reverberate from the core to the periphery. Manufacturing growth accelerated during August on the largest boost to export orders in more than six years, while services growth moderated.The eurozone unemployment rate held at 9.1% in July.

US labour-market gains slowed in August. The unemployment rate increased to 4.4%, while average hourly earnings growth slid from the prior month. Personal-income growth strengthened in July and consumer spending warmed up, while inflation pressures remained light. Economic growth was revised upward for the second quarter, to a 3% annualised rate.

Our View

At the start of this year, SEI held an optimistic view regarding the path of the US economy, corporate profits and, by extension, the stock market. We saw a great opportunity for the passage of business-friendly tax and regulatory reforms—but our hopes for legislative policy now appear too optimistic. Trump’s unpopularity has emboldened the opposition to put up a unified resistance.

US stock-market sectors that performed well immediately following the election have corrected sharply or lagged the overall market meaningfully in the year to date. By contrast, post-election laggards have bounced back sharply. Throughout these gyrations, the US equity market has managed to climb to new record highs. The lack of volatility has brought the widely-watched Chicago Board Options Exchange Market Volatility Index (VIX) to extremely low levels, which we would argue increases the odds of at least a garden-variety correction.

Although our optimism is being tested, we are gamely sticking to our expectation that a major tax bill will be pushed through US Congress. Widespread hopes of a big cut in US corporate tax rates will most likely moderate toward aspirations for a smaller cut. Whatever the size, this fiscal stimulus should still boost economic growth prospects, but could eventually add to inflationary pressures since the country’s economy is edging closer to full employment.

Fed Chair Yellen and a majority of her colleagues may be coming to the same conclusion, as evidenced by the second federal funds rate hike this year and the apparent intentions of the Federal Open Market Committee to reduce the size of the central bank’s balance sheet. The pace of quantitative tightening should not be exceptionally disruptive to the bond market, at least during its ramp-up phase. But the Fed’s selling could aggravate upward pressure on bond yields if investors become more concerned about the inflation outlook. With the 10-year US Treasury bond yielding just 2.12% at the end of August, however, it is obvious that inflation concerns are not yet paramount.

One of the great puzzles remains the lack of upward pressure on the US inflation rate despite a tightening labour market. Wages and salaries continued to rise at a sedate pace, so corporate profit margins remained unusually robust for an aging economic expansion. The connection between tight labour markets and wage inflation has seemingly been severed by slow economic growth; little visible progress on tax reform and fiscal policy stimulus; weak oil pricing; and the secular disinflationary forces of demographics and disruptive technological change.

We believe this is why investors have returned to strategies emphasising yield and stability. Unfortunately, it’s hard to see the value in fixed-income yields that are so low in absolute terms and credit spreads that are tight relative to US Treasury bonds. We do not think this lack of appeal portends imminent danger since inflation also is still low—but it does increase the vulnerability of fixed-income assets to a negative surprise (as is the case with the VIX and US equities).

European economic sentiment has risen to the highest level since 2007, suggesting that economic growth may soon accelerate. Perhaps more important for investors, eurozone earnings have begun to pick up in a recovery that appears to have momentum. The ECB’s expansion efforts seem to have finally had a positive impact. Loan growth accelerated to its best pace in six years—an encouraging-yet-slow expansion that argues strongly in favour of Draghi’s long-standing preference to maintain the current pace of quantitative easing at least through the end of 2017.

The recent UK election result means the country is now far more likely to move toward a “soft” Brexit. In our view, UK services industries and the City of London have more to gain from a hybrid relationship with the European Union than from a complete sundering of the relationship (as is the wish of more hardline Brexiteers).

This latest political surprise came at a time when the UK was showing mixed economic results. Inflation has been accelerating over the past year, which can be traced to sterling’s steep decline since August 2015. This has not been matched by rising incomes—UK households have been falling behind, even though the unemployment rate dropped to its lowest level in 40 years.

If a trophy were given to the most underrated stock market, we would vote for Japan. It is no secret that its economy faces serious demographic issues. Yet Japanese equity prices have outperformed both the US and Europe since 2012, when Prime Minister Shinzo Abe entered office. Governance of large, publicly traded companies in Japan has improved quite a bit, as the government under Abe has been working hard to open markets that were protected from competition.

Another factor behind the strong performance of Japanese equities stems from the liquidity infused into the economy by the BOJ through its quantitative and qualitative monetary-easing programme. As a percentage of gross domestic product, the central bank’s securities holdings are almost as large as the economy itself.

As interest rates in the US move up and the differential versus Japanese yields widens, we anticipate the yen to resume its trend of weakening against the US dollar. This should serve as a tailwind for additional price appreciation in Japanese equities.

Developing-market equities have been on a tear this year, with the MSCI Emerging Markets Index far outpacing US equities in the year to date. To be sure, we have seen previous episodes of US equities lagging during this long bull market—but those were typically brief stumbles, lasting a mere few months. Perhaps the current bout of underperformance will also prove transitory. But we no longer view US equities as the best game in town.

Despite the gains, emerging stock markets have remained attractive on a valuation basis relative to developed markets. Investors have also been drawn to the region due to improving global economic fundamentals, with China leading the way and Brazil recording a sharp recovery from recession.

We still have concerns about the sizable increase in debt across developing economies—mostly within the corporate sector, especially in China. But at this point, we expect current trends to hold—moderate global economic growth, rising inflation that leads to commodity-price gains, and a stable or slightly weaker US dollar—all of which provide a favourable macroeconomic backdrop for emerging-market economies and financial markets.

[1] According to the country-level or regional components of the MSCI ACWI Index (Net).

Glossary of Financial Terms

Asset-backed securities: Asset-backed securities are a type of securitised debt that are backed by loans, leases or credit card debt, but not mortgages. Securitised debt consists of a portfolio of assets, such as mortgages or bank loans, which have been grouped together and repackaged as individual securities.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to do so) and investor confidence is high.

Core eurozone countries: Core eurozone countries are those countries in the eurozone with the largest economies.

Credit spread: Credit spread is the additional yield, usually expressed in basis points (one basis point is 0.01%), that an index or security offers relative to a comparable duration index or security (the latter is often perceived as “risk-free” credit, such as sovereign government debt).

Fundamentals: Fundamentals refers to data that can be used to assess a country or company’s financial health, such as amount of debt, level of profitability, cash-flow and inventory size.

High-yield debt: High-yield debt is rated below investment grade and is considered to be riskier.

Macroeconomic: Macroeconomic refers to the broad economy of a country or region, or the global economy.

Mortgage-backed securities: Mortgage-backed securities are made up of multiple mortgages packaged together into single securities. These can be comprised of commercial or residential mortgages. Agency means that the debt is guaranteed by a government-sponsored entity, while non-agency means that it is not.

Peripheral eurozone countries: Peripheral eurozone countries are those nations in Europe’s common-currency area that were hit hardest by the sovereign debt crisis (most notably Greece, Ireland, Italy, Spain and Portugal).

Quantitative easing/tightening: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy; quantitative tightening refers to efforts by central banks to help decrease the supply of money in the economy.

Treasury inflation-protected securities: Treasury inflation-protected securities are US Treasury securities issued at a fixed rate of interest, but with principal adjusted every six months based on changes in the consumer price index.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Important Information

Past performance is not an indicator of future performance.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.