Monthly Market Commentary: Markets Fall into Autumn

Economic Backdrop

The British government released a set of contingency plans in late August detailing how segments of the UK economy should prepare for possible failure in striking a Brexit deal with the EU before the autumn deadline; the French government announced intentions to do the same as divorce negotiations persisted. UK cabinet-level ministers asserted throughout the month that the only two realistic negotiation outcomes include one that closely adheres to Prime Minister Theresa May’s so-called Chequers plan or one that reaches no deal at all. The EU’s chief Brexit negotiator, Michel Barnier, said at the end of August that he is holding out hope for a one-of-a-kind trade partnership between the EU and UK, while also ruling out single-market access.

US and Mexican negotiators neared a deal to revise their portion of the trilateral North American Free Trade Agreement, leaving the US-Canada component to be resolved amid ongoing negotiations at month-end. The EU expressed willingness to lift tariffs from all US industrial products—including automobiles (which have been a sticking point with US President Donald Trump’s administration)—provided that the US does the same. Meanwhile, the US Chamber of Commerce, a business-focussed lobbying group with unrivalled influence on conservative politics, launched a pressure campaign to highlight the economic pitfalls of relying on tariffs to conduct trade policy.

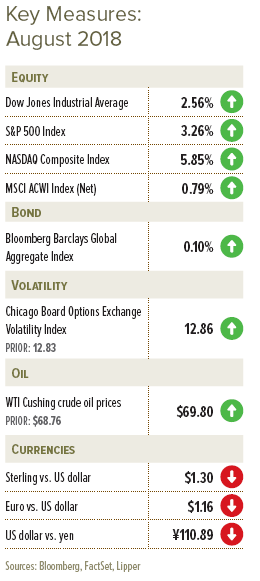

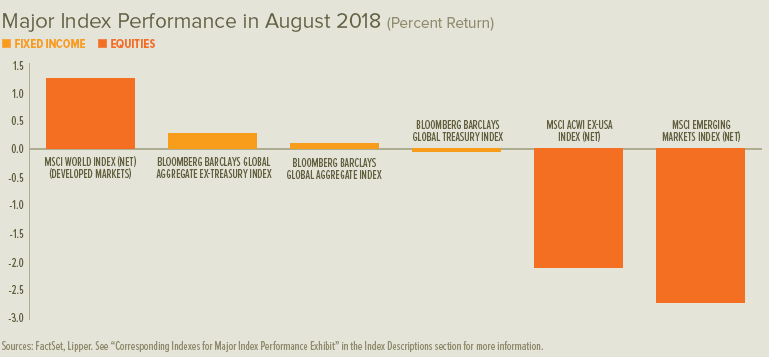

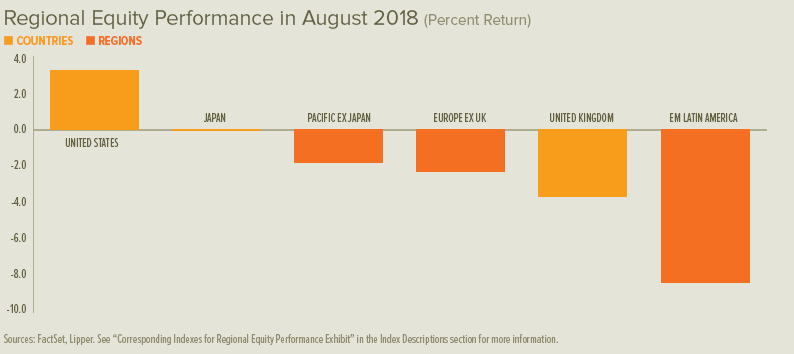

British equities tumbled in August, delivering the poorest performance among major developed markets, and European shares declined on notable weakness in peripheral countries like Greece and Italy (according to country-level performance within the MSCI ACWI Index). US equities jumped higher, providing the only positive performance among major developed markets for the month. Hong Kong and mainland China shares fell, as did South American equities. A double-digit decline in Brazil was overshadowed by a meltdown in Argentina, where the government was forced to take extraordinary measures—including hiking the central bank’s benchmark rate to 60%, securing a stabilization loan from the International Monetary Fund, and announcing austerity measures—all in an effort to keep the Argentine peso from dropping further. Turkey also faced deep destabilisation starting in early August, when the announcement of US sanctions caused a re-evaluation of the country’s ability to service its heavy foreign-debt load, sending the Turkish lira into freefall.

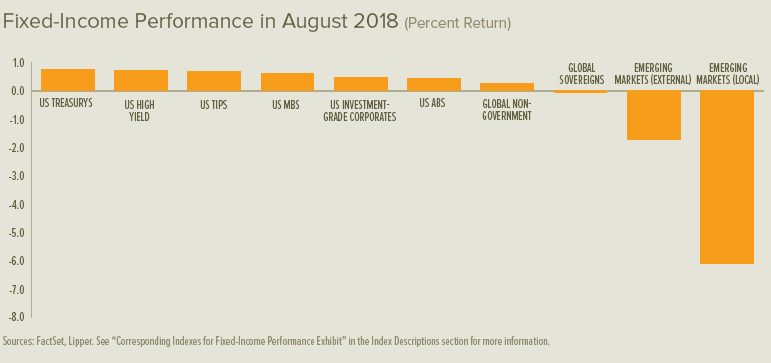

Yields on UK gilts and US Treasurys declined, except for those with the shortest maturities, while euro-area government bond yields fell universally across all maturities during the month. The Bank of England’s Monetary Policy Committee voted unanimously in early August to increase the bank rate by 0.25%, its second such hike of the current cycle. Bank Governor Mark Carney expressed willingness to remain on the job past his planned departure next summer to help provide stability as the UK grapples with its exit from the EU. The European Central Bank (ECB) and Bank of Japan had no meetings in August; both kept their policy paths steady following late-July meetings, and the Japanese central bank said it plans to offer more specific forward guidance on policy rates in an effort to influence its inflation target. The US Federal Open Market Committee took no new actions on monetary policy, according to its statement on the first of August. Meeting minutes released later in the month revealed that most members think another rate hike would probably be warranted in the near future given bright prevailing economic conditions. US Federal Reserve (Fed) Chairman Jerome Powell offered a measure of accommodation at the central bank’s annual summit in Jackson Hole, WY, saying that its policy-setting committee would try to avoid overreacting with rate hikes if faced with inconclusive economic data.

UK services sector growth jumped in August, exhibiting healthy conditions, while manufacturing growth slowed to more modest levels. July’s claimant count (the number of people claiming unemployment benefits) held firm at a 2.5% rate. Unemployment for the April-to-June period fell by 0.2% to a rate of 4.0%, although average year-over-year earnings growth ticked down to 2.4%. Overall economic growth registered 0.4% for the second quarter, improving by 0.2% from the final reading of the prior quarter.

Eurozone manufacturing growth softened during August, while services strengthened; however, both measures were at healthy levels of expansion despite remaining far below their respective peaks at the beginning of 2018. Economic sentiment continued to trend lower on slowing economic growth. The eurozone unemployment rate was 8.2% in July, unchanged from June’s downward-revised figure. Total economic growth was adjusted higher by 0.1% for the second quarter (to 0.4%) and for the 12-month period ending June (to 2.2%).

US manufacturing reports for August depicted consistently strong new-order growth, while services-sector growth slowed. Prices for core personal consumption expenditures (the Fed’s preferred inflation gauge) edged up to 2.0% in July, precisely in line with the central bank’s target inflation level. Economic growth was adjusted higher by 0.1%, to an annualised 4.2% second-quarter rate.

Our View

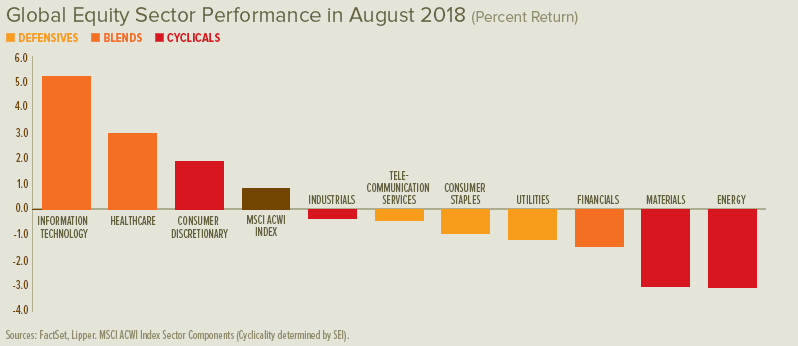

Make no mistake about it: headwinds blowing in the face of risk assets have accelerated. Growth in business activity has slowed somewhat, especially in Europe. Monetary policy has tightened in the US and is set to become less expansionary in Europe. Inflation has ticked higher across the major economies, driven by synchronised global growth and a contracting of labour markets and industrial capacity in the US, Germany, the UK, China, and elsewhere in Asia. A jump in oil prices has pushed headline consumer-price index readings to their highest levels in several years; the Organization of the Petroleum Exporting Countries and Russia have shown a fair degree of discipline in constraining the supply of crude oil at a time when demand is strong and inventory levels have fallen. Some developing countries have been forced to raise their policy rates dramatically in an effort to defend their currencies.

Most important, the stoking of trade-war tensions by the US has threatened to undermine the very foundation of the system that has supported the global economy since the end of the Second World War. Although actual US trade actions to date have been modest, the impact on global supply chains bears close watching.

Economic fundamentals that drive the stock market nevertheless appear solid, even in places like Europe and developing economies. Plus, interest rates remain at levels that are accommodative to global economic growth. Key risks—escalating trade tensions and the polarisation of electorates over issues like immigration and fiscal sovereignty—appear more political in nature. The positives include a still-solid global economy, strong momentum in corporate-profits growth, and persistent equity valuations that seem reasonable against the backdrop of still-low (albeit rising) interest rates.

If one believes, as we do, that the global economy is sound and current political uncertainties will be contained, then the proper course (in our view) should be to remain exposed to equities and other risk assets and ride out the short-term ups and downs.

ECB President Mario Draghi and other bank governors decided to conclude net asset purchases by the end of this year because they view deflation risks as having moderated significantly. Since the ECB will no longer be a price-insensitive buyer of eurozone debt, we could see yield spreads rise as investors demand a risk premium for those countries with a heavy debt burden relative to the size of their economy. Italy’s new government wants to institute several expensive propositions that would blow a hole in the government’s budget, likely causing the country’s bonds to be further discounted by investors—with other periphery countries’ bond yields rising in sympathy.

Recent UK economic data reports, like those of other countries in Europe, suggest that Great Britain is wending its way through a soft patch. Underlying growth nevertheless appears solid, indicating the UK economy is in stable condition; although the trade sector looks to be a problem spot.

The biggest source of uncertainty facing the UK is its looming withdrawal from the EU. The Conservative Party’s internal fight over the country’s future relationship with the EU has stalled progress toward a clear post-Brexit status. Maybe it’s sheer coincidence, but sterling versus the US dollar is almost where it was the day after the Brexit vote on 23 June 2016. The recent trend has been to the downside, as currency-market participants worry about the rising odds of a hard Brexit and more-thorough disruption of UK trade with the EU. We would not be surprised to see further downside volatility in sterling as we draw closer to the EU exit date.

American investors, businesses and consumers have much to applaud despite fears of a trade war pitting the US against foes and allies alike. The country’s corporate tax reform, tax cuts for households, and reduced or modified regulation of various industries have led to record-high consumer and business confidence.

But sabre-rattling between the US and China has deteriorated into actual skirmishing, and the latest back-and-forth suggests this spat will get worse before it gets better. To be blunt, the Trump administration’s strategy of waging a trade war with China could prove to be the equivalent of cutting off one’s nose to spite one’s face.

In the US, a trade war will likely lead to higher prices for consumers and hurt the bottom lines of companies that sell imported goods and those that depend on global supply chains in their production process—resulting in a net loss for its society. A small group of American producers will probably benefit substantially from the trade impediments, while most consuming industries and households suffer declines in purchasing power—declines that may be small at the level of the individual but would add up to an enormous loss across the affected economies. With any luck, the Trump administration will shy away from further ratcheting tensions. But we must admit that doesn’t seem to be in the cards in the near-term.

A confluence of events has conspired to hurt the performance of emerging-market assets. An extensive trade war that disrupts multinationals’ supply chains would interrupt the flow of raw commodities and semi-finished materials from developing economies, which depend on these exports for economic growth. Rising US interest rates, resulting in another period of sustained US dollar strength, are a second threat. The soft patch in Europe and recent signs of deceleration in China’s economic growth is a third.

But while emerging-market stocks and bonds have come under pressure this year, we’ve yet to see any widespread deterioration in economic performance or financial conditions. On balance, we think most emerging markets have the ability to weather the storm—again, assuming the disruption to global trade does not devolve into something more encompassing.

A broadening of the trade war with China or a US departure from the North American Free Trade Agreement would likely have a severely negative impact on the profitability of US manufacturers, prompting us to reassess our still-positive view. Impediments to trade also could lead to a higher inflation rate as US companies use the tariffs umbrella to raise their selling prices. The US Fed may feel compelled to lean against this threat to price stability, thereby aggravating any economic shock arising from the disruption of global supply chains—which is how a bear market could develop.

This is not our base-case scenario. We still think this old bull has some life left in it, but the risks to the equity market now seem more balanced than skewed to the bullish side.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to do so) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to do so) and investor confidence is high.

Fundamentals: Fundamentals refers to data that can be used to assess a country or company’s financial health such as amount of debt, level of profitability, cash flow, inventory size, etc.

Yield spreads: Yield spreads represents the difference in yields offered between different types of bonds. If they tighten, this means that the difference has decreased. If they widen, this means the difference has increased.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.