Monthly Market Commentary: Markets Diverge on Geopolitical Unknowns

Economic Backdrop

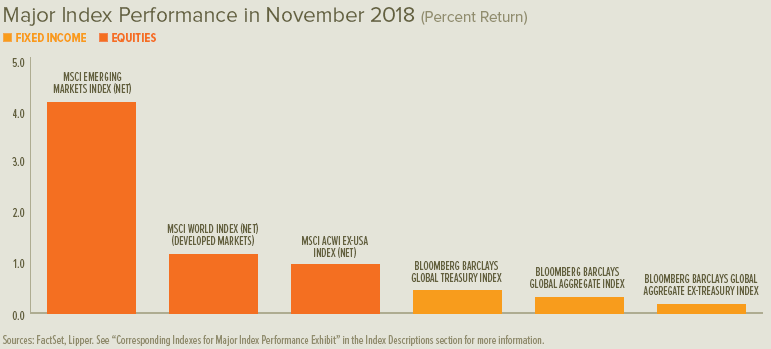

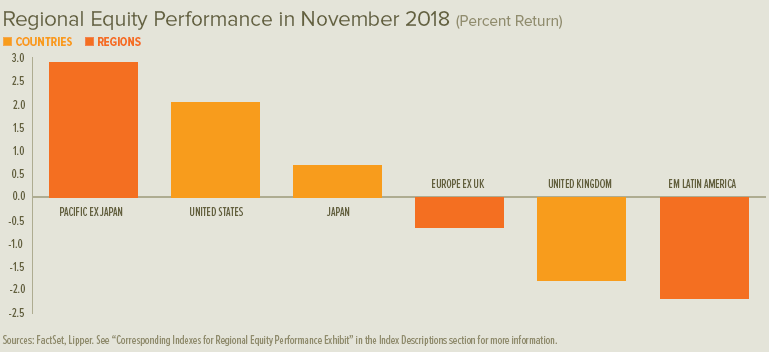

Volatility continued in November, with mixed performance across capital markets. UK and European stocks registered poor performance amid ongoing Brexit uncertainty, while Latin America reversed course as it posted the worst regional performance in November after outpacing the rest of the world last month. US and Asia-Pacific stocks gained on a possible respite from trade-war concerns ahead of early-December talks between US President Donald Trump and Chinese President Xi Jinping at the Group of 20 (G-20) summit in Argentina; the two leaders ultimately agreed to a temporary trade-war truce calling for the US to postpone tariff increases in exchange for China’s commitment to purchase a substantial (but yet-to-be-determined) amount of US agricultural, energy and industrial products in order to reduce the huge US trade deficit with China.

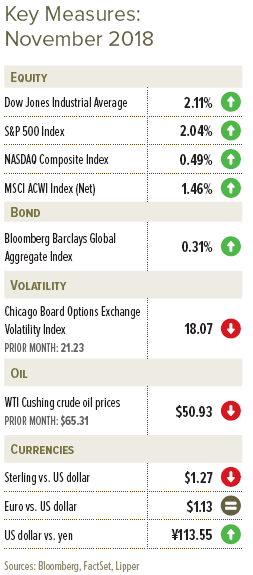

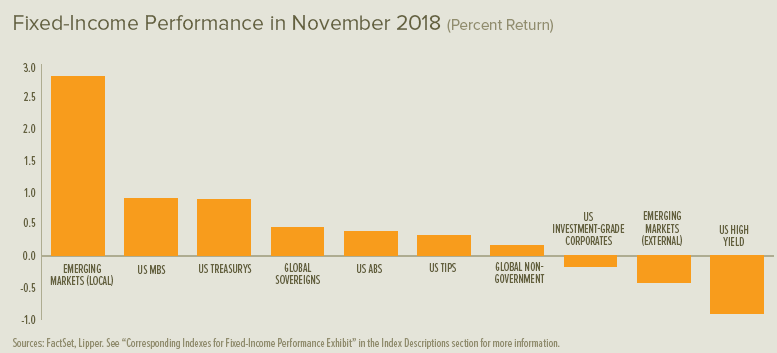

Riskier fixed-income segments such as high-yield and emerging-market debt (foreign-currency-denominated) once again lagged the broader market along with investment-grade bonds. (Local-currency emerging-market debt performed well.) However, in a reversal from the prior month, UK and EU government bond yields increased in November (yields move inversely to prices); the yield on the 10-year US Treasury note moved lower for the month. West Texas Intermediate crude-oil prices tumbled further from their early-October peak, descending by 22% in November.

European leaders finally signed an agreement in November after more than two years of negotiations, officially outlining the terms of the UK’s divorce from the EU. If it passes EU and UK parliamentary votes next month, the two sides will enter a 21-month post-Brexit standstill on 29 March during which they will negotiate future trade and security provisions. The treaty also includes a solution to avoid a hard border on Northern Ireland, allowing it to remain in the EU’s single market and customs union. An additional non-binding document indicates an agreement to maintain strong economic ties between the UK and EU—yet prohibits UK manufacturers from gaining unrestricted access to the EU’s single market; it also calls for close security cooperation.

While reaching a divorce agreement was a significant breakthrough, UK Prime Minister Theresa May must still secure support from sceptical members of Parliament—a particularly difficult task as the treaty includes a range of compromises that have elicited criticism across political affiliations.

Failure to secure backing from lawmakers before Brexit occurs on 29 March, as scheduled, could result in significant trade and security disruptions between the UK and EU.

In the US, the Federal Reserve (Fed) released a financial stability report toward the end of the month, citing the biggest risks facing the country’s financial system: increased asset prices; historically elevated debt burdens for US businesses; and rising issuance of higher-risk bonds. The report also noted that potential shocks to the US economy—such as indirect effects of Brexit fallout, slowing growth in emerging markets (particularly China), or ongoing trade tensions—could further test the country’s financial system. The US-China trade detente in early December came days after the Fed’s report was released.

None of the world’s major central banks, with the exception of the Fed, held monetary-policy meetings in November; each is scheduled to reconvene in mid-to-late December. The European Central Bank (ECB) released its meeting minutes from the prior month, which stated that recent economic data for the region remained in line with broad-based economic expansion despite weaker-than-anticipated reports; the minutes also reiterated the ECB’s intention to end net asset purchases before the end of the year. In the US, the Federal Open Market Committee maintained its federal-funds rate and confirmed that inflation sits near 2% amid strong jobs growth and consumer spending, yet noted moderating business investment. The Fed remains widely expected to hike rates in December.

UK manufacturing beat expectations in November, expanding by two points from the 27-month low recorded in October, yet remained one of the slowest monthly paces recorded in the past two-and-a-half years. Construction growth also fared better than anticipated in November, hitting the highest point since July of this year. Labour-market conditions appeared mixed in the latest report: claimant-count unemployment increased by 0.1% to 2.7% in October; the July-to-September unemployment rate ticked 0.1% higher from the prior reporting period to 4.1%; average year-over-year earnings growth increased by 0.2% to 3.0% over the same three-month period.

Eurozone business activity softened further in November, with manufacturing growth picking up by less than expected (with output registering its worst reading in about 65 months) and services growth shrinking to a 25-month low. Unemployment increased so minimally that the rate held steady at 8.1% in October; joblessness in Italy surged, offsetting improvements France, Germany and Spain. The second estimate of overall economic conditions was unchanged, showing eurozone gross domestic product (GDP) expanding by 0.2% in the third quarter and 1.7% year over year—a deceleration over both periods and the slowest quarterly pace since the three-month period ending September 2014.

US manufacturing was depicted in mixed reports as healthy in November, either accelerating to an unusually strong pace or softening slightly to a still-solid rate of expansion. Services-sector growth appeared to moderate in November, according to preliminary reporting. The core personal consumption expenditures price index registered a lower-than-expected 0.1% gain in October, falling below the Fed’s target inflation level with a year-over-year increase of 1.8%. Payrolls increased in November, and average hourly earnings grew by 3.1% year over year, as the unemployment rate remained at a 49-year low. The US economy grew at a slower but still-strong 3.5% annualised rate for the third quarter, according to an unrevised second estimate.

Our View

The ratcheting-up of trade-war tensions between the US and China has remained the number-one preoccupation of investors. And with good reason: Whatever happens between the two countries has global implications. China and the US together accounted for 42% of world nominal GDP last year. So, when Trump and Xi agreed to a ceasefire, it makes sense that markets around the world breathed a collective (if temporary) sigh of relief—particularly in Asia and other emerging markets, which tend to have trade-dependent economies.

While China’s currency soared higher immediately after news of the agreement, its remains far lower than the US dollar and versus a broader basket of currencies compared to its level before trade tensions arose. The weaker currency has partially offset the impact from tariffs already imposed by the US, while the competitiveness of Chinese exporters against other countries has improved as a result of this year’s devaluation.

The US is still in strong shape economically—but nobody wins in a trade war. Even White House advisors with a pro-trade bias do not expect the US to come out unscathed if tit-for-tat tariffs between the two countries resume after a 90-day ceasefire.

Despite a near-term view that is fraught with uncertainty, we continue to believe in diversifying portfolios with emerging-market exposure. The alpha opportunities (that is, the ability to achieve returns in excess of benchmarks) also are much greater given the economic and political idiosyncrasies inherent in the asset class. The price-to-earnings ratio for the MSCI Emerging Markets Index is still running at a discount to that of the MSCI USA Index (as at 30 November 2018).

Before the trade war with China appeared set to cool at month end, the Trump administration had already turned more conciliatory toward other countries with which it had picked fights. Broad agreement has been reached with Mexico and Canada on the new trilateral United States-Mexico-Canada Agreement (USMCA), which replaces NAFTA (notwithstanding Mexico’s stipulation of being exempt from steel and aluminium tariffs); the proposed new agreement is now pending approval by the US Senate and House of Representatives. However, the threat of tariffs on European and Japanese autos and auto parts was reignited by the Trump administration ahead of formal negotiations due to start in January; we are hopeful that the White House realises that it’s better to gain allies in its battle against China than fight on multiple fronts.

In Europe, there are business-as-usual problems: sluggish economic growth, still-high unemployment and the never-ending disagreements over how expansive monetary policy should be. Europe also faces trade tensions of its own. The UK is far more dependent on the EU as an export market than the other way around. A “hard” Brexit would therefore severely affect the UK’s export of financial and other services (keep in mind that manufacturing accounts for only 10% of the UK’s GDP nowadays, while services account for 80%).

Although a last-minute agreement or a mighty kicking of the can down the road is possible, widespread fear of a hard Brexit is apparent in the economic data. The Organisation for Economic Co-operation and Development’s (OECD) leading economic indicators show that the UK has deteriorated more dramatically than any of the world’s other major developed economies.

As if the future departure of the EU’s second-largest member isn’t bad enough, Italian government-bond yields have risen sharply higher this year as the Lega/Five-Star coalition pushes to make good on some of its campaign promises. Italy is the third-largest eurozone economy, and has the fourth-largest debt-to-GDP ratio in the world. To say the least, a debt crisis in Italy would not be as easy to handle as the Greek one (which wasn’t all that easy).

A complicating factor for Italy and other highly-indebted countries is the tapering of asset purchases by the ECB. Since the program’s inception, the ECB’s purchases of Italian bonds equate to 53% of the country’s cumulative deficit (as at 30 September 2018), according to German think tank Centre for European Economic Research (ZEW). Italy will be losing a large price- and risk-insensitive buyer of its bonds at an inopportune time. The ECB is set to finish its taper at the end of the year.

Tax cuts, deregulation and strong revenue growth have provided an ideal backdrop for US equities to appreciate, but performance could be constrained if earnings estimates fade in light of increasing tariffs on tradable goods. Valuations also could fall if interest rates climb at a faster-than-expected pace. That said, we still think it’s premature to turn negative on the near-term US outlook given today’s mosaic of economic fundamentals. In our view, the risks to the US stock market are evenly balanced.

The multi-year persistence of high US corporate profit margins is unusual. Margins have spiked in the past two quarters, reflecting the impact of the US tax cut and the acceleration of sales growth. In the latter stages of an economic expansion, margins normally contract on a sustained basis as higher costs for labour, interest-expense and depreciation take a larger slice of the pie.

Besides uncertainty about trade tensions with China, we see the Fed as another, more traditional, major potential threat to the US equity bull market. The question is how high the federal-funds rate will ultimately go, and whether that level proves to be sufficient to keep inflation near the central bank’s 2% target or turns out to be overkill. We agree with the Fed’s view that the federal-funds rate is still below the so-called neutral rate of interest. Additional rate increases appear appropriate, as long as the Fed doesn’t keep hiking after reaching the neutral rate—a level that has historically seen the stock market run into real trouble.

One can argue about whether the valuations embedded in the US equity market are high, especially when measured against other global stock markets, although earnings growth in the latter has been less robust. The extreme appreciation in some large technology companies also suggests that the US stock market could be subject to a sharp rotation from previous winners to the laggards somewhere down the road. SEI equity strategies certainly tilt in the direction of more value-oriented companies and industries.

Predicting the future is a hazardous venture most of the time. In view of the uncertainties presently facing investors, the prediction game is, perhaps, even more challenging. Accordingly, we believe in a diversified approach to investing. Although maintaining exposure to risk assets may feel uncomfortable, we believe that investors with long time horizons should know that mistiming entries and exits into and out of equities can be costly. Today, mistiming an exit is the greater concern.

Glossary of Financial Terms

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to do so) and investor confidence is high.

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Fundamentals: Fundamentals refers to data that can be used to assess a country or company’s financial health such as amount of debt, level of profitability, cash flow or inventory size.

Index Descriptions

MSCI World ex USA Index: The MSCI World ex-USA Index is a free float-adjusted market-capitalisation-weighted index that is designed to measure the equity market performance of developed markets, excluding the US.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.