Monthly Market Commentary: Lockdowns Resume at Pivotal Political Moment

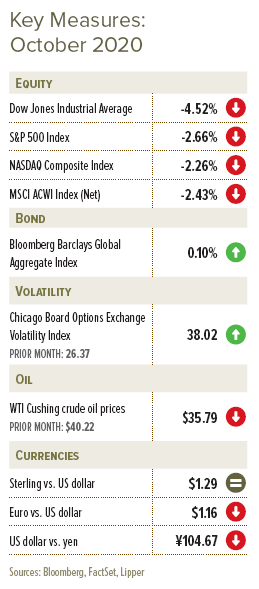

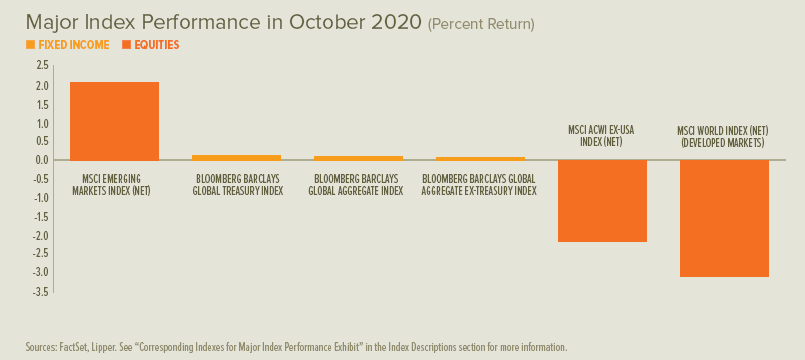

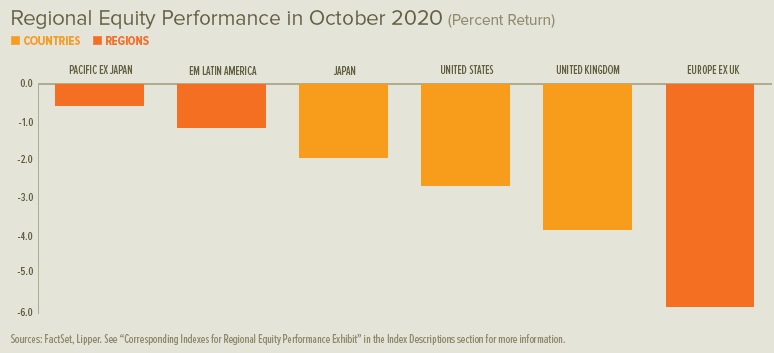

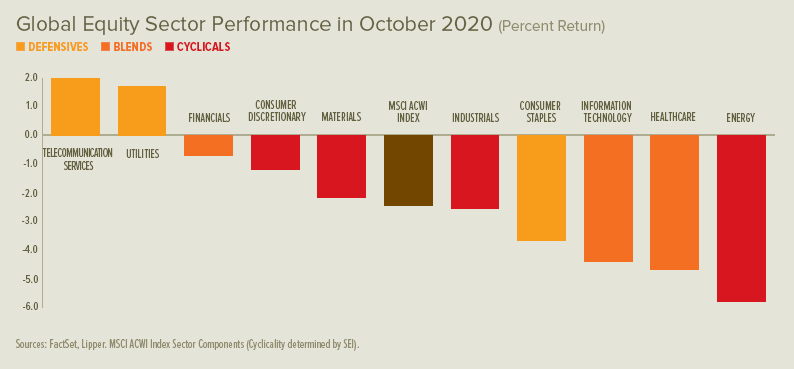

Global equity markets declined in October for the second month in a row1. A broad-based advance for the first few weeks of October gave way to a sharp late-month spike in volatility and a steep selloff driven by a new wave of rising COVID-19 cases. Developed markets were down for the period. European and UK equities declined most dramatically, followed by the US; Japan’s loss was comparably mild. Emerging markets, on the other hand, rallied following their September slide. China’s gains helped propel the rebound, while Brazilian shares were modestly negative.

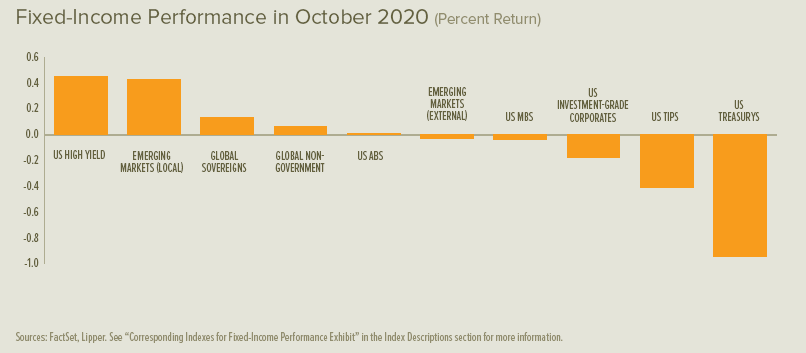

The West-Texas Intermediate crude-oil price declined by approximately 11% from its October peak through the end of the month as prospects for global economic activity cooled alongside rising cases2. UK and US government-bond rates generally increased across the yield curve, while rates declined in the eurozone. US dollar weakness returned in October after being temporary interrupted by a large rebound in late September, resuming its slide against a trade-weighted basket of foreign currencies that began in March after the passage of a massive US fiscal stimulus.

Governments re-imposed lockdown measures as COVID-19 cases climbed through October. England announced four weeks of closures affecting pubs, restaurants, gyms and other non-essential retail businesses. The restrictions were coupled with plans for greater government payments for affected self-employed workers as well as an extended deadline (until January) to apply for business loans underwritten by the government. France and Germany announced similar plans in late October centred on closing bars and restaurants for a month.

UK and EU negotiations over a potential post-Brexit trade agreement continued through the end of October but remained stuck on fishing rights and state aid to businesses. Specifically, the EU wants a long-term guarantee regarding the allocation of fishery rights and access to British waters, while the UK wants to renegotiate these rights every year. With regard to business subsidies, the EU seeks to ensure a level playing field that would unlikely give either side unfair advantages.

These talks accelerated to a daily pace as of late October; negotiators now estimate that final the terms must be settled by mid-November for any deal to be enforced by the end-of-year expiration of the Brexit transition period. An agreement would need to be passed through UK and EU Parliaments before becoming law. At the same time, an EU-UK joint committee had begun hashing out the real-world implications of the Withdrawal Agreement’s Northern Ireland Protocol for customs and border cooperation under a no-deal Brexit scenario.

In the US, another major round of fiscal stimulus remained elusive. President Donald Trump expressed willingness to meet the high price tag proposed by Democrats in control of the House of Representatives, while Republicans with power in the Senate did not appear willing to go along. The 2020 US general election featured the highest US voter-participation rate in 120 years. Historic turnout, combined with an unprecedented surge in mail-in ballots, slowed the vote-counting process compared to past elections. Former Vice President Joe Biden appeared set to win the race, although he’s expected to face vote re-counts and other election-related lawsuits before the results can be certified.

The World Trade Organization handed down a ruling in mid-October that allows the EU to impose retaliatory tariffs on $4 billion of US exports in response to favourable tax treatment for major US aerospace companies. Elsewhere, China demanded that the US stop a planned sale of surface-to-surface missiles to Taiwan (which China considers part of its territory). China responded in part by announcing in late October that it intends to sanction major US defence companies for arms sales to Taiwan.

Economic Data

- The rebound in UK manufacturing growth slowed through October after peaking in August. Growth in the UK services sector followed a similar path, although with a higher August peak and a sharper deceleration in October. UK mortgage lending jumped dramatically in September, beating forecasts for the first time since June. Meanwhile, consumer credit contracted by £622 million in September on expectations for an expansion, indicating a potential return to contraction after growing through July and August 3.

- The eurozone’s recovery in manufacturing activity continued to solidify in October after a promising improvement during September. Services sector activity contracted for the second consecutive month in October, retreating further from its peak growth recorded in July. Eurozone unemployment hit 8.1% in September, the fourth straight monthly increase. The overall eurozone economy grew by 12.7% during the third quarter and contracted by 4.3% year over year.

- US manufacturing growth has persisted at a moderate pace since August—yet reports were mixed for October, with some showing acceleration and others indicating a continuation of modest expansion. While new orders drove the sector’s growth in prior months, manufacturing employment played a key role in October as it began to expand for the first time since July 2019. Initial US jobless claims oscillated between 800,000 and 900,000 during most of October before dipping to 787,000 later in the month. The overall US economy grew at a 33.1% annualised rate in the third quarter, the largest quarterly gain on record following a record-breaking decline in the prior quarter.

Central Banks

- The European Central Bank (ECB) made no new changes to monetary policy following its late-October meeting. However, the Governing Council announced plans to use periodic economic projections at its December meeting to conduct a thorough reassessment and take new actions as appropriate. ECB President Christine Lagarde noted that the eurozone economy appeared to be “losing momentum more rapidly than expected” and that the “rise in COVID-19 cases and the associated intensification of containment measures is weighing on activity, constituting a clear deterioration in the near-term outlook.”The Bank of Japan (BOJ) also took no new actions following its late-October monetary policy meeting. It will continue to implement all tools associated with its Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control policy; separately, its crisis-response programme will proceed until at least March 2021.

- Neither the Bank of England’s Monetary Policy Committee nor the US Federal Open Market Committee (FOMC) held meetings in October.

SEI’s View

It has already been an eventful and exhausting year, but we have a sense that the next few months could prove critical to the future course of the global economy and financial markets. Most countries were in V-shaped recovery mode during the third quarter, moving sharply off their low points in May and June. The latest round of lockdowns to contain COVID-19 outbreaks appear more limited in scope than those instituted earlier this year. For developed countries, virus treatments have improved, vulnerable populations appear to be better-protected, and younger, generally healthier people have started to account for a much larger share of confirmed new cases.

Despite these positive developments, we doubt there will be a full return to normal economic behaviour until safe and effective vaccines are approved and distributed globally. The news on this score has also been favourable, and probably is a key reason for the continued buoyancy of equities and other risk assets. According to the World Health Organization, 45 vaccines were in clinical trials at the end of October, while 156 more were in pre-clinical testing.4 We think it is realistic to assume that a few different vaccines will be generally available by this time next year, which means that social-distancing measures must still be followed well into 2021 and, most likely, into 2022.

There’s no disputing that US economic activity remains far below normal. Although incomes have been recovering as more people get back to work, the lack of additional income support may be a drag on consumer spending in the final months of the year. Business sentiment appears to have bottomed, but the outlook remains sufficiently uncertain to keep us in a watch-and-wait mode. We would not be surprised to see the official US unemployment rate move up during the third quarter as hard-hit industries are expected to eliminate jobs now that government support has run out.

In August, Federal Reserve (Fed) Chairman Jerome Powell officially unveiled a new framework for conducting the central bank’s monetary policy. The Fed has decided to see how low the US unemployment rate can get before it causes the inflation rate to exceed the 2% mark by a meaningful extent. It may be a long time before the federal-funds rate rises as the FOMC’s own projection does not envision a return to 2% inflation until the end of its forecast window in 2023.

In our view, all that’s really left in the Fed’s monetary toolbox is quantitative easing, along with the provision of lifeline support to corporations as well as state and local governments through its various credit facilities. Monetisation of debt will likely continue until the pandemic crisis is in the distant past and the US unemployment rate approaches its previous lows.

The US presidential election is expected to have a major impact on the economy and financial markets in the months and years ahead. Still, we firmly believe that it would be a mistake to pursue even a short-term investment strategy that necessitates accurately predicting: (1) policies proposed by the newly inaugurated president; (2) the ways in which Congress will modify those proposals throughout the legislative process; or (3) the impact those new laws would have on the economy and financial markets.

Regardless of the election’s outcome, we assume the winning candidate will see his platform tempered before it’s put into practice. This is partly deliberate (constitutional checks and balances) and partly happenstance (increasing polarisation of opinion in the country tends to favour a draw). While there could be some market volatility plausibly attributed to the election, it is usually best to pay strict attention to the fundamentals and to ignore the politics.

The ongoing UK-EU trade negotiations have created their own unique political melodrama—and a hard Brexit would certainly not help matters. But the worst possible impact of a no-deal divorce—and subsequent reversion to the World Trade Organization’s (WTO) most-favoured-nation trading rules—would likely be sustained by financial companies and other service-producing entities as WTO rules deal mostly with tradable goods. The increase in tariffs, for the most part, will be bearable once border-related issues are worked out. In the meantime, the UK and the rest of Europe are facing a second wave of COVID-19 that could turn what’s been a V-shaped recovery into something looking more like a W.

This year’s pandemic and postponement of the summer Olympics proved to be a bitter ending to Japanese Prime Minister Shinzo Abe’s record-breaking term in office. His push to lift Japan out of its deflationary spiral was somewhat successful. Prices mostly stopped declining in the aggregate, but there were few occasions when overall consumer-price inflation rose above 1%. Pandemic pressures have caused a return to outright deflation in recent months.

In our view, it is unlikely that radical changes will be made to the direction of policy under Japan’s new Prime Minister Yoshihide Suga. In the near-term, the priority will be on the response to the coronavirus; fiscal policy will remain quite expansionary. The Bank of Japan will continue to buy most of the government-issued bonds along with other types of corporate debt and equity as part of its QQE program over the past four years.

The contrast of the big Asian stock markets versus other large emerging-market equities is dramatic. China’s strong gains can be chalked up to its rebound in economic activity. Although travel and other services are still constrained due to lingering concerns about the virus, infrastructure-related spending and manufacturing have experienced an almost-complete recovery to pre-pandemic levels. Investors seem unfazed by the deterioration of China’s economic relationship with the US or the increasingly fraught diplomatic relations between China and other countries.

Emerging markets are already showing some good news. The price of raw industrials has moved sharply higher since bottoming in early May. It’s a good bet that emerging-market corporate profits will also rise sharply if industrial commodity prices advance in a sustained, multi-year fashion as they have in previous cycles.

Our optimism is somewhat tempered by the rising debt burden facing many emerging countries. Much of the increase in emerging-market debt has been tied to the corporate sector—especially in China, where private domestic, non-financial debt has reached an eye-watering 216% of GDP5. Of more concern are the mostly small-to-medium-sized countries that are running current-account deficits and are too dependent on external hard-currency debt, or do not have the reserves to easily cover their debt service.

The actions of the world’s major central banks back in March, especially the US Fed’s provision of US dollar liquidity, have helped to ease the strain on the market for emerging-country debt. Governments and other official lenders, meanwhile, have granted loan forbearance to nearly 80 countries; it’s a tougher job to get private creditors to agree to do the same6. Nonetheless, emerging-market sovereign yields on US dollar-denominated debt have fallen back toward their previous record lows, more than reversing the spike endured prior to the Fed’s rescue operations in March.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Pandemic Emergency Longer-Term Refinancing Operations (PELTROs): PELTROs are a series of longer-term refinancing operations intended by the ECB to ensure sufficient liquidity and smooth money-market conditions during the COVID-19 pandemic period. PELTRO operations are planned to be allotted on a near-monthly basis maturing in the third quarter of 2021.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset-purchase programme of private and public sector securities established by the ECB to counter the risks to monetary-policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Paycheck Protection Program: The Paycheck Protection Program is a loan offer by the US government’s Small Business Administration (SBA) designed to provide a direct incentive for small businesses to keep their workers on the payroll. SBA will forgive loans if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest or utilities.

Quantitative and Qualitative Monetary Easing with Yield Curve Control: The BOJ’s policy framework consists of two major components. The first is “yield curve control” in which the BOJ controls short-term and long-term interest rates through market operations. The second is an “inflation-overshooting commitment” in which the BOJ commits itself to expanding the monetary base until the year-on-year rate of increase in the observed consumer price index exceeds the price stability target of 2 percent and stays above the target in a stable manner.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.