Monthly Market Commentary: January Hot Streak Ends on a Cold Note

Economic Backdrop

UK Prime Minister Theresa May announced plans in late January to limit the free movement and residency rights of EU citizens starting in the post-Brexit transition period despite demands from EU negotiators for status quo through the end of 2020. An impact report prepared for the Department for Exiting the EU was leaked to the media, painting a bleak picture of potential Brexit outcomes for the UK economy. Negotiations over the formation of a grand coalition in Germany continued through month-end, with the expectation of a pact in early February—indicating the likely continuation of pro-EU government in Europe’s largest economy. Italy’s euro-sceptic Five-Star Movement, the best-polling individual party heading into an early March election, dropped a promise to hold a referendum on pulling Europe’s third-largest economy out of the euro. Conservative parties are expected to win the largest combined share of votes, however, and form a governing bloc; some anticipated coalition members are still weighing a euro departure.

The US government shut down for several days in the middle of January before congressional Republicans and Democrats agreed to pass another stopgap spending bill that was expected to last for three weeks. The Trump administration announced tariffs on imported solar panels and washing machines in a move designed to protect American manufacturers from lower-priced overseas competition, garnering mixed responses. The president also openly contemplated renegotiating membership in the Trans-Pacific Partnership trade agreement after bowing out a year ago. Fourth-quarter earnings appeared strong: three-quarters of S&P 500 Index constituents that reported their numbers thus far (about half as of 2 February) pointed to positive earnings surprises; an even higher number of companies had favourable sales surprises.1 US oil production in November, reported on the last day of January, topped 10 million barrels per day for the first time since 1970.

US Federal Reserve (Fed) Chair Janet Yellen presided over her last monetary policy meeting on 31 January (at which no changes were made), as her four-year term came to an end. The European Central Bank (ECB) and Bank of Japan (BOJ) similarly announced no changes to their policy programmes. The BOJ kept its quarterly economic projections steady; although the central bank’s announcement in early January of reduced long-term bond purchases propelled yields and the yen upward (yields and prices move inversely). The Bank of England’s (BOE) Monetary Policy Committee had no January meeting.

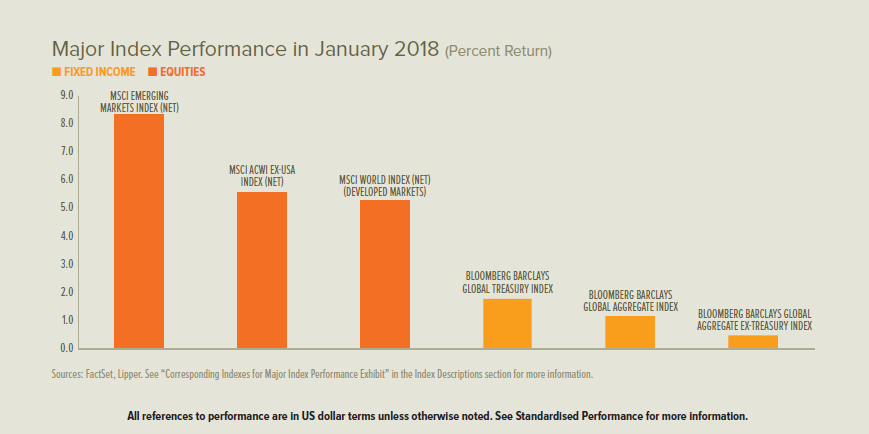

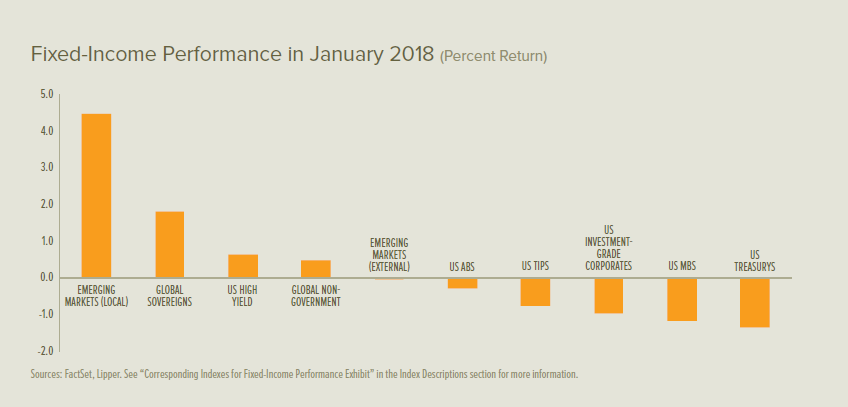

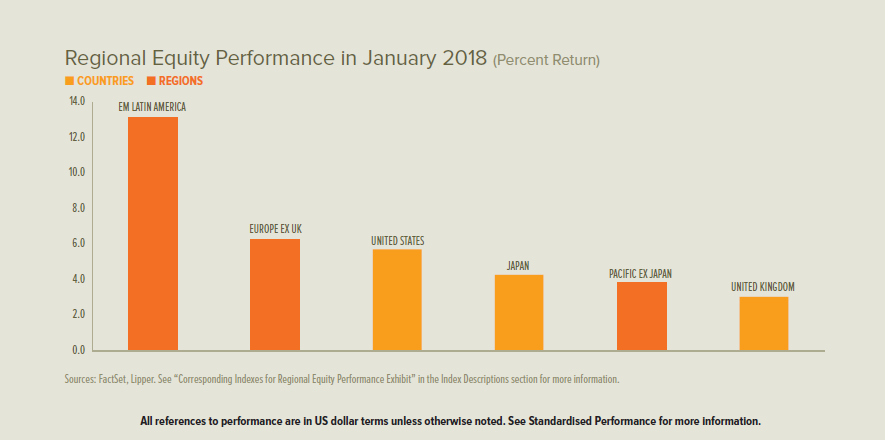

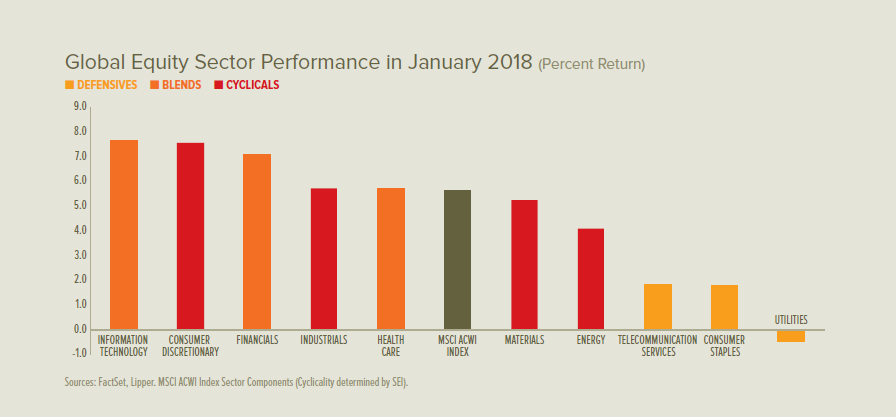

Equity markets were generally higher around the world in January, but experienced a significant risk-off move near the end of the month that reverberated through the beginning of February. Major developed-market government-bond rates advanced across essentially all maturities. The 2-year US Treasury yield rose above 2% for the first time since September 2008, and the 10-year yield reached its highest level in almost four years; but the 30-year yield, while elevated, remained below its 2017 peak. The US dollar continued to slide, touching its lowest level (against major foreign currencies on a trade-weighted basis) in more than three years.

UK services sector activity slowed during January, but remained firmly in expansion territory, while construction growth decelerated to just above a standstill. Manufacturing growth also moderated, but at healthier levels. Claimant count unemployment edged down in December from the prior month’s upward-revised figure, pushing the rate higher. The Septemberto- November unemployment rate and average earnings growth figures were unchanged for the one-year period ending November—at 4.3% and 2.5%, respectively—from the previous report. The British economy grew by 0.5% in the fourth quarter, according to an early estimate, improving slightly compared to prior three-month period.

Eurozone momentum carried into the New Year as services sector growth hastened to impressive levels and manufacturing growth (while modestly lower) also showed remarkable strength. The unemployment rate was an unchanged 8.7% in December; however, 134,000 Europeans found work during the month (almost matching November’s upward-revised gain) and the youth unemployment rate declined. Preliminary overall fourth-quarter economic growth was measured at 0.6% (and 2.7% year over year).

The solid pace of growth in US manufacturing activity was essentially maintained in January, while non-manufacturing growth accelerated by far more than expected. Unemployment held at 4.1% in January, and average-hourly-earnings growth accelerated to a 2.9% year-over-year rate.

Personal-income growth increased in December, while consumer-spending growth decelerated and inflation pressures appeared to remain contained. Employment costs were reported near the high end of their expected ranges in fourth-quarter productivity reports. The first estimate of fourthquarter economic growth indicated a 2.6% annualised rate, which was a disappointment following the 3.2% pace in the third quarter.

Our View

The global financial crisis finally appears to be in the rear-view mirror. In its place is synchronised expansion across most developed and emerging economies. Admittedly, developed economies continued to run at a rather sluggish pace of approximately 2% to 2.5% gross domestic product (GDP) growth (as of the latest available figures for the fourth quarter). This is, at best, a middling sort of performance in the context of the past five decades.Emerging-market economies, meanwhile, continued to expand at a clip well below that of the past 20 years. Over the next year or so, we think global growth can still be vibrant enough to allow risk assets to perform well.

US tax legislation is hardly perfect: we do not expect it to be as stimulative as advertised since tax cuts are skewed toward upper-income tax payers who tend to have a higher saving rate than the median household. But the permanent corporate tax changes, repatriation holiday, and the full expensing of capital equipment purchases over the next five years are positive developments for economic growth and investment.

Security analysts, always an optimistic lot, are calling for an 11% rise in S&P 500 Index per-share operating earnings in 2018. Although earnings estimates tend to fade through the year as estimates adjust to reality, this time may be an exception because tax cuts have not yet been taken fully into account.

The major worry for investors comes down to the stock market’s valuation. A little more than three-fifths of the S&P 500 Index’s price gain in 2017 came from improving earnings, while the rest was due to a rise in the priceto- earnings (P/E) ratio. But elevated valuations can be justified by the low level of bond yields and the strong trend in profits growth. Of course the higher the valuation, the more vulnerable the stock market becomes to unexpected bad news. The market is overdue for a correction—in 2017, the S&P 500 Index didn’t even register a price pullback of 3%—and we have already witnessed a peak-to-trough decline of greater magnitude from late January through the beginning of February.

We won’t be really concerned, though, unless we see a more aggressive swing in Fed policy toward monetary tightness—something we don’t anticipate in the coming year. It’s possible that the US will see inflation pressures finally begin to build in the New Year, but US companies have proven able to maintain profit margins without resorting to price increases. In our opinion, Europe has more growth potential than the US. According to the World Economic Forum’s annual report on global competitiveness, the high-income countries of Western Europe have made important strides in improving labour-market efficiency over the last five years. We also would note that political concerns in the eurozone are far more muted compared with a year ago, although we have not yet seen the end of the heavy antiestablishment undercurrent.

Given our view that the region is a long way from employment levels that will stir inflation pressures, we expect monetary policy to be supportive of growth throughout the coming year—even as the ECB proceeds with tapering its quantitative-easing programme. Since we expect these asset purchases will continue at least until the end of September, it appears that policy rates will stay put until 2019.

We therefore believe the path is clear for further economic growth in the year ahead. The strong 2017 revival in corporate revenues and earnings should continue; the MSCI European Economic and Monetary Union Index (Total Return) forward P/E ratio was no higher as of December 31, 2017, than it was a year earlier. Solid economic growth and cheap equity valuations are usually a good combination for investors.

These have not been easy days for UK Prime Minister Theresa May. The divorce stage of Brexit talks has finally concluded, with the UK mostly acceding to the EU’s demands. But Parliament has begun to flex its muscles—and disapproval there would force the parties back to the negotiating table. Keep in mind that any changes to the withdrawal agreement demanded by Parliament would require unanimous approval of the 27 members of the EU on the other side of the negotiating table.

The BOE’s Monetary Policy Committee forecasted only two rate increases between now and the end of 2019. While time will tell whether the central bank’s view regarding future policy moves are accurate, policymakers in the UK face tremendous challenges over the next few years. We think investors should tread lightly until there are clearer signs that inflation pressures have peaked and Brexit negotiations actually yield a favourable economic outcome for the country.

Japan is clearly benefiting from the global economic recovery. Exports to China are growing particularly quickly, and are now about equal to the share going to the US. Exports to the US and Europe also have accelerated, but not to the same extent.

Although there have been rumblings that the BOJ would like to take a step away from the extraordinary monetary policies that have been in place since the financial crisis, the central bank may find it difficult to do so. Domestic demand remains weak and the population has begun contracting, a trend that will likely accelerate.

Japanese equities did well last year, with the TOPIX rising by 26.55%. Remarkably, the forward P/E ratio declined over the course of 2017 despite the improvement in economic fundamentals. It remains one of the morecheaply valued stock markets among developed countries. Forwardearnings estimates have climbed sharply in the past year; we note that revenue estimates are also inflecting higher.

Emerging-market equities climbed significantly last year, with a particularly strong contribution from China. Despite some backsliding last year, China has continued to reduce its dependence on heavy industry and increase the value added to GDP from service-producing industries. While these macro statistics need to be taken with a grain of salt, it appears that China’s growth has accelerated significantly from two years ago and is advancing at its fastest clip since the 2012 to 2013 period. If China can maintain positive momentum, commodity prices should continue to rally as well.

We have held a positive view of risk assets for most of this long bull market. When speaking to investors who are nervous about the stock market’s valuation, we urge them to keep a longer-term focus. Timing the market in anticipation of a short-term correction should be discouraged. As we’ve seen in the past year, making a major de-risking move could result in a significant opportunity-loss when there are few, if any, signs of major economic imbalances or frothy valuations. Until we see a more significant deterioration in the economic and financial fundamentals that have underpinned the global bull market in risk assets over the past two years, our default investment stance is to stay the course. There are many possible events and developments that could have a big negative impact, but most have a low probability of actually happening. We

will therefore maintain our “risk-on” bias until we see evidence that such a stance merits revision.