Monthly Market Commentary: Investor Appetites Fuel Broad Advance in Risk Assets

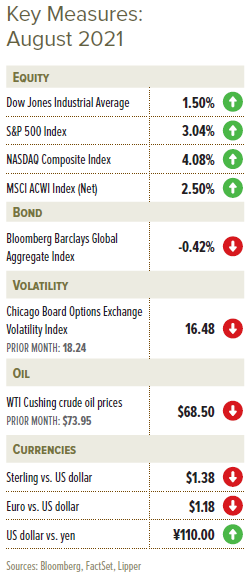

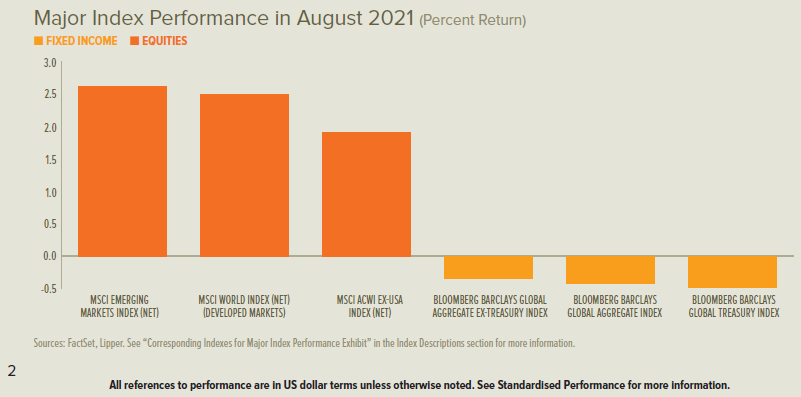

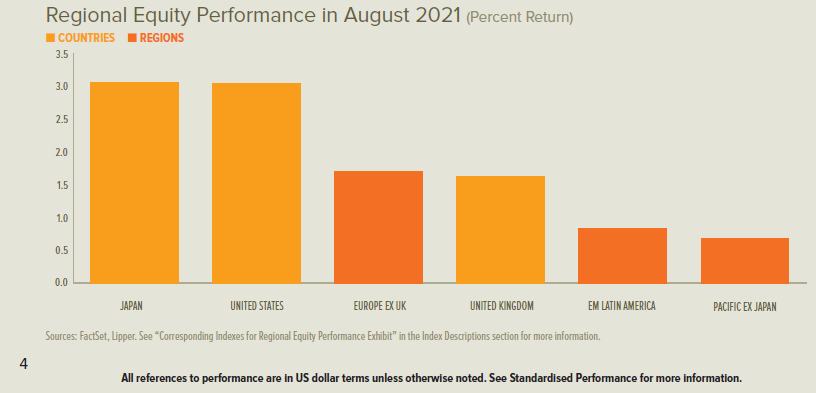

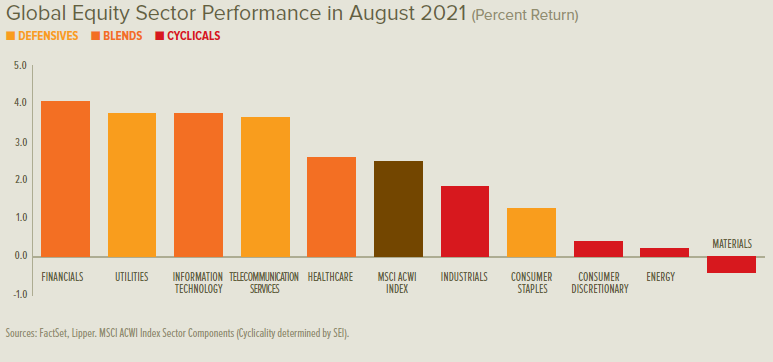

Investor risk appetite increased in most corners of the world during August. Equities delivered strong performance in developed and emerging markets alike, led by Japan and the US within the major economies. European and UK shares also posted healthy returns, while China and Hong Kong were slightly down for the month. Globally, the financials sector was the top performer, while materials lagged with a modest decline.

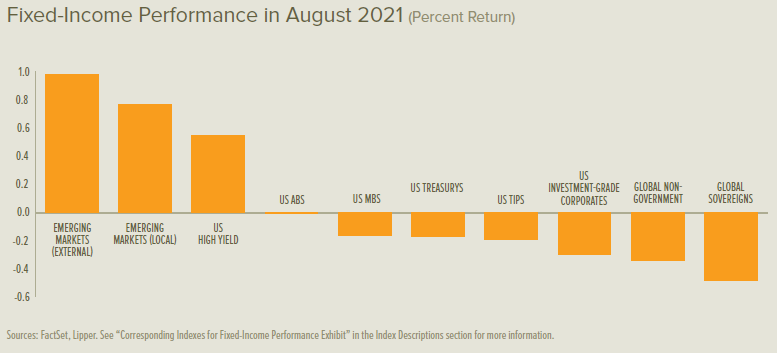

Bonds were mostly a bit lower—aside from higher-risk segments like high-yield and emerging-market debt—as rates increased around the world. Short- to medium-term rates trailed the advance across the gilt yield curve, while they led the climb in eurozone government bonds. Intermediate-term US Treasury rates rose by more than short- and long-term rates.

The US dollar strengthened (according to the DXY Index), peaking in mid-August before giving back a majority of the month’s advance. Prices were down across West-Texas Intermediate and Brent crude oil in August as OPEC+ (the Organization of the Petroleum Exporting Countries led by Saudi Arabia, plus Russia) continued to ramp up production.

Inflation-sensitive assets were subdued during the month. The Bloomberg Commodity Index registered a small loss in U.S. dollar terms, and the decline in U.S. Treasury Inflation Protected Securities (TIPS) essentially matched the slide in U.S. Treasurys of comparable maturities.

The summer wave of COVID-19 cases appeared to peak beginning in mid-August, led by the US in terms of both new reported cases and daily deaths. Cases were growing at the fastest rate in Montenegro, Georgia, Kosovo and Israel in late August. Regions contending with at- and near-peak cases were spread across the Western Pacific, the Balkans and the Greater Middle East, as well as the Caribbean and neighbouring countries1.

Portugal caught up to the United Arab Emirates’ lead on the share of their respective populations that had received at least one dose of COVID-19 vaccine (both around 85% at the end of August). The UK surpassed 70% of its population, while the US approached 61%. South Korea was administering more vaccine doses per capita than any other country in late August2.

France instituted the required use of the EU’s digital health certificate beginning in early August for patrons to verify their COVID-19 vaccination status to gain access to restaurants, various modes of public transit, sports events, and other public gathering places. Italy also adopted the EU’s certificate-based verification method during the month, although on a more limited basis, while Germany’s certificate programme varied according to regional infection rates.

The German federal election, which concludes in late September, headed toward an increasingly clear outcome in the race to succeed Chancellor Angela Merkel. The Social Democrats (SPD)—led by Olaf Scholz, the current vice chancellor and finance minister—carved out a polling lead over Merkel’s CDU/CSU, its current and traditional senior governing coalition partner.

The EU recommended limiting travel by Americans at the end of August as cases rose stateside, although it yielded the actual decision to member states, which mostly planned to remain open to US tourists.

The Infrastructure Investment and Jobs Act—a plan negotiated by a bipartisan group of US senators that would direct $1 trillion (and $550 billion in new spending) toward infrastructure projects over a five-year period—slipped off the front pages as August progressed. Scheduled US

congressional summer recesses and a near-universal occupation with the strained US withdrawal from Afghanistan dominated priorities in Washington, DC. The final end-of-August departure of US military troops concluded 20 years of military operations—the longest war in US history—which culminated a decade ago with 100,000 troops stationed in Afghanistan.

Economic Data

UK

- UK manufacturing activity continued to rapidly expand at a pace in August that was in line with July’s levels, although supply-chain issues worsened (with average supplier lead times at their longest-recorded levels aside from April 2020’s early COVID-19-induced bottlenecks) even as output improved3.

- Services growth also remained strong in the UK during August, but was well below the torrid pace that defined most of the first half of 20214.

- The UK claimant count (which calculates the number of people claiming Jobseeker’s Allowance) held at 5.7% of the population in July as the total number of claimants decreased from 2.30 million to 2.29 million.

- The broad UK economy grew by 4.8% during the second quarter and 22.2% year over year, up from -1.6% and -6.1%, respectively, during the prior quarter.

Eurozone

- Manufacturing growth in the eurozone continued to ease in August from its June record high, but still registered extraordinary strength5. Relative country-level prospects narrowed as fast-growing countries (Netherlands, Ireland, Germany and Austria) moderated to multi-month lows, while slower growers (Italy, Spain and Greece) improved to multi-month highs, although France remained mired in slower growth.

- Eurozone services activity in August held just below July’s record pace of expansion (dating back to June 2006)6.

- The eurozone unemployment rate declined to 7.6% in July from 7.8% in June.

- The overall eurozone economy grew by 2.0% during the second quarter and 13.6% year over year, representing a marked improvement over the first quarter’s respective rates of -0.3% and -1.3%.

US

- US manufacturing activity softened in August, but remained in red-hot growth territory. New orders and production jumped, backlogs lengthened, and price pressures intensified, while employment contracted modestly7.

- Services growth was strong in the US during August, but continued to mirror the UK’s softening trajectory following a remarkable period of expansion8.

- New claims for US jobless benefits trended toward 350,000 per week during August, spending an entire month below 400,000 for the first time since March 2020.

- Overall US economic growth measured an annualised 6.6% during the second quarter, just above the first-quarter pace of 6.3%.

Central Banks

- The Bank of England’s (BOE) Monetary Policy Committee (MPC) voted in early August to maintain its policy path: the bank rate remained 0.1% and the maximum allowance for asset purchases was unchanged at £895 billion.

- The European Central Bank (ECB) did not convene a meeting on monetary policy during August. During July, however, the central bank unveiled the results of a strategy review in which it adopted a symmetric inflation target of 2% over the medium-term (meaning that it views deviations above or below its target as undesirable) and an acknowledgement that it anticipates fluctuations over shorter time frames.

- The US Federal Open Market Committee (FOMC) also held no formal monetary policy meeting during August. Federal Reserve (Fed) Chairman Jerome Powell spoke at the Federal Reserve Bank of Kansas City’s annual economic symposium in Jackson Hole—a historical platform for sharing significant evolutions in the central bank’s outlook and policy actions—to reinforce that the FOMC could begin to taper, or reduce, asset purchases this year. The FOMC currently purchases $80 billion in US Treasurys and $40 billion in agency mortgage-backed securities per month.

- The Bank of Japan (BOJ) had an August holiday from monetary policy meetings as well. It had shared details in mid-July about its green loan initiative, including extending 0% interest-rate credit to banks for their “green” lending efforts, waiving punitive negative interest rates for associated bank reserve requirements, and allowing foreign-currency bonds issued by Japanese companies to be eligible for the programme.

SEI’s View

Equity markets have long anticipated the economic improvement we are watching unfold. There is increasing concern, however, that equity prices have risen so much that there is little appreciation potential left, even if the global economy continues to forge ahead into 2022.

Since mid-June, we have witnessed a partial unwinding of the rotation trade (from expensive technology-oriented stay-at-home companies to less-expensive cyclically-oriented companies) that began last autumn. So far, this appears to us to be a temporary pause in a longer-term upswing. The global recovery and expansion have a long way to go, especially since many countries are still imposing lockdown measures to varying degrees.

We can’t rule out a choppier and more lacklustre performance for US equities in the months ahead given their strong outperformance since March 2009 and elevated stock-market valuations relative to much of the rest of the world. If stock-market volatility does increase, we don’t think there’s reason to be overly concerned; corrections that range from 5% to 10% can occur without any fundamental reason.

In today’s environment, with economies opening up around the globe and interest rates still at extraordinarily low levels, the dominant trend favours further price gains over the next year or two. Still, investors must take into account that the US economy appears to have reached “peak growth.”

Growth slowdowns, not just recessions, can lead to equity underperformance versus bonds. The relative performance of equites versus bonds was phenomenal over the past 17 months9; a major narrowing of the performance gap is inevitable. Yet, with interest rates still at exceptionally low levels, it is hard to see equities losing ground to fixed-income securities while economic growth remains robust. Not only should consumer demand remain strong as long as economies continue to reopen, but businesses have been in a spending mood—desperately seeking materials and workers.

In the meantime, companies are expected to enjoy a great deal of pricing power and will almost certainly pass along at least a portion of their increased costs to customers. Unfortunately, one person’s pricing power is another person’s inflation. The big question is whether the price pressures seen this year are transitory, as central bankers around the world say they are.

Investors in the bond market seem to agree with the central bankers. Although US bond yields rose sharply in the first quarter, they have since fallen. There’s no telling how long bond investors will maintain such a calm perspective if inflation persists at a pace not seen in almost 30 years.

Fed Chairman Powell has continued to reiterate that the US labour market has a long way to go before it reaches full employment. Job openings in the country are now soaring. If the rise in the Employment Cost Index accelerates as we expect, inflation could become a greater concern for investors.

The recent stumble in the rotation theme was exacerbated by the marginally hawkish shift in Fed expectations. It is clear, however, that the US central bank intends to cautiously move away from its current policy stance.

The path of US fiscal policy is harder to decipher given strained bipartisanship and the narrowness of the Democratic majority in the Congress. A traditional infrastructure bill appears likely to get passed with bipartisan support, but the push for non-traditional forms of infrastructure—and the taxes to pay for all the added spending—will depend on whether the Democrats in the Senate can come to terms with each other.

The combination of above-average economic growth, significantly higher inflation than seen in the past decade, a fiscal policy that expands the size of federal government spending, and extreme monetary ease aimed at suppressing interest rates, is the perfect backdrop for risk assets—and the creation of speculative bubbles.

The relative success of the US vaccination effort and the country’s state-by-state response has resulted in a significantly stronger economy this year than in other major developed countries. Fortunately, injection rates have been accelerating in Europe and Japan. We believe other advanced economies will record strong economic results in the second half of the year and into 2022, exceeding the pace of growth in the US.

Although economists correctly point out that the US has employed direct fiscal measures (emergency spending, income support and tax breaks) more aggressively than any other nation, other countries have used different tactics that far exceed the US effort.

Several European nations and Japan have relied on equity injections, loans and guarantees. Italy (35% of gross domestic product), Japan and Germany (both at 28%) are the most notable, according to the International Monetary Fund10. In the eurozone, some of these loan commitments have only just begun to flow. Italy and Spain are big beneficiaries of the eurozone’s €750 billion in loans and grants as part of the so-called NextGenerationEU programme.

The ECB also seems dedicated to maintaining its pandemic-related monetary support at least through March 2022. As a percentage of gross domestic product (GDP), the ECB’s balance sheet has risen more than 25% since the beginning of the COVID-19 crisis, more than any other major central bank besides the BOJ (30%)11. The ECB’s actions have succeeded in keeping peripheral Europe’s sovereign bond yields well behaved through the crisis period.

While the US, the UK and Canada seem to be enduring a much sharper inflationary increase than Japan or the eurozone, the latter two are probably relieved to have a respite from the deflationary pressures that have afflicted their economies for many years. There seems little reason for the ECB or BOJ to join the Fed when it comes to discussing a near-term reduction in asset purchases, much less raising their policy rates ahead of the US.

We do not see much evidence that the Fed’s shift toward an earlier lift-off in rates will lead to a 2013-style “taper tantrum” among emerging economies. A strong US dollar would certainly threaten the bull market in commodity prices.

While we are still bullish on the outlook for commodities, we are watching price trends carefully. Commodity prices of all types have enjoyed a spectacular run since March 2020 and were already in the process of consolidating or correcting before the Fed revised its views in mid-June.

We remain optimistic that the more cyclical and value-oriented areas within emerging markets will bounce back from their modest stumble in June. But there are near-term challenges besides the shift in perceptions about Fed policy and the future course of the US dollar and commodity prices. Credit growth has decelerated significantly in China, similar to the slowdowns recorded in 2013 and 2018—years when the performance of emerging markets was less than stellar.

Another potential source of market volatility could stem from the increasingly fraught relationship between China and the US and its allies. If there is any consensus in Washington nowadays, it is focused on countering China’s growing economic and military strength; although market participants have mostly managed to look past political tensions to date.

Fundamentally, emerging markets continue to look cheap versus most other regions. The forward price-to-earnings multiple of the MSCI Emerging Markets Index is selling at a 41.8% discount to that of the MSCI USA Index. Outside the March-to-April 2020 low point, this is as cheap a relative multiple against the US as has been seen at any time in the past 16 years12.

We are counting on advanced economies to take up the slack while vaccines ramp up in developing countries. There has been a tremendous amount of excess savings and pent-up demand in North America and Europe. That said, as we’ve witnessed with the surge in new cases driven by the delta variant, the possibility of regional spikes cannot be dismissed. If severe enough, markets could switch back to a decidedly risk-off position.

As vaccination rates slow in the developed world, more shots are becoming available to the rest of the world. We expect a rolling reopening of the global economy that will extend well into 2022. This wave of recovery could resemble a prolonged up-cycle that keeps the pressure on supply chains, leading to continued shortages of goods and labour. Investor faith in the “transitory inflation” narrative probably will be tested as we head into year end and enter 2022.

Glossary of Financial Terms

Asset-Backed Securities (ABS): ABS are securities created from pools of loans or accounts receivable such as credit cards, auto loans and mortgage loans.

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bubble: A bubble occurs when excessive speculation leads to a drastic increase in asset prices, leaving them at risk to collapse.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Cyclical stocks: Cyclical stocks or sectors are those whose performance is closely tied to the economic environment and business cycle. Managers with a pro-cyclical market view tend to favour stocks that are more sensitive to movements in the broad market and therefore tend to have more volatile performance.

Delta variant: The B.1.617.2 (delta) variant of the severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2), the virus that causes coronavirus disease 2019 (Covid-19), arose during the sharp surge in cases in India during spring 2021 and has now been detected across the globe, including notable increases in cases in the UK and US.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Forward price-to-earnings (PE) ratio: The forward PE ratio is equal to the market capitalisation of a share or index divided by forecasted earnings over the next 12 months. The higher the PE ratio, the more the market is willing to pay for each dollar of annual earnings.

Gilt: Gilt refers to a sovereign debt instrument issued by the UK government.

Green lending: Green lending refers to the Bank of Japan’s effort to strengthen the lending market for environmentally-friendly projects.

Hawk: Hawk refers to a central bank policy advisor who has a negative view of inflation and its economic impact and thus tends to favour higher interest rates.

Inflation-Protected Securities: Inflation-protected securities are typically indexed to an inflationary gauge to protect investors from the decline in the purchasing power of their money. The principal value of an inflation-protected security typically rises as inflation rises, while the interest payment varies with the adjusted principal value of the bond. The principal amount is typically protected so that investors do not risk receiving less than the originally invested principal.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Mortgage-Backed Securities: Mortgage-Backed Securities (MBS) are pools of mortgage loans packaged together and sold to the public. They are usually structured in tranches that vary by risk and expected return.

NextGenerationEU: NextGenerationEU is an economic recovery fund established by the EU and totalling more than €800 billion projected to be spent between 2021 and 2027. The centrepiece of the programme is a €723.8 billion facility for loans and grants to EU countries for investments.

OPEC+: OPEC+ combines OPEC—a permanent intergovernmental organisation of 13 oil-exporting developing nations that coordinates and unifies the petroleum policies of its member countries—with Russia, a major oil exporter, to make collective high-level decisions about oil production levels.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset purchase programme of private and public sector securities established by the ECB to counter the risks to monetary policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Summary of Economic Projections: The Fed’s Summary of Economic Projections (SEP) is based on economic projections collected from each member of the Fed Board of Governors and each Fed Bank president on a quarterly basis.

Taper tantrum: Taper tantrum describes the 2013 surge in U.S. Treasury yields, resulting from the U.S. Federal Reserve’s announcement of future tapering of its policy of quantitative easing.

Transitory inflation: Transitory inflation refers to a temporary increase in the rate of inflation.

Treasury Inflation-Protected Securities (TIPS): TIPS are sovereign securities issued by the US Treasury that are indexed to an inflationary gauge to protect investors from the decline in the purchasing power of their money. The principal value of TIPS rise as inflation rises, while the interest payment varies with the adjusted principal value of the bond. The principal amount is protected so that investors do not risk receiving less than the originally invested principal.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Index Descriptions

The Bloomberg Commodity Index is composed of futures contracts and reflects the returns on a fully collateralized investment in the Index. This combines the returns of the Index with the returns on cash collateral invested in 13-week (3-month) U.S. Treasury bills.

The US Dollar Index (DXY Index) measures the value of the US dollar relative to a basket of other currencies, including the currencies of some of the US’s major trading partners: the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona.

The Employment Cost Index is a quarterly economic series published by the U.S. Bureau of Labor Statistics that details the growth of total employee compensation. The index tracks movement in the cost of labour, as measured by wages and benefits, at all levels of a company.

The MSCI Emerging Markets Index is a free float-adjusted market-capitalisation-weighted index designed to measure the performance of global emerging-market equities.

The MSCI USA Index measures the performance of the large- and mid-cap segments of the U.S. market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.