Monthly Market Commentary : Global market performance diverges amid volatility.

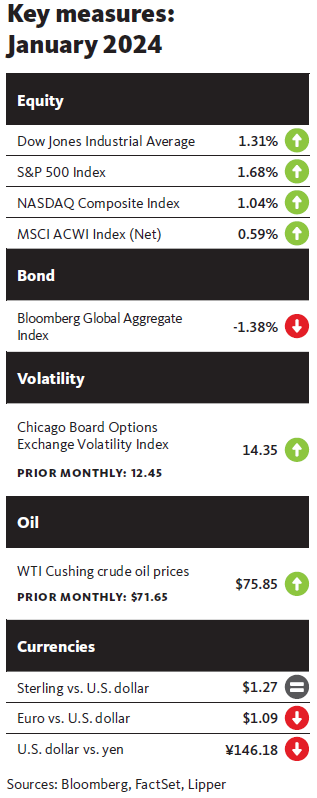

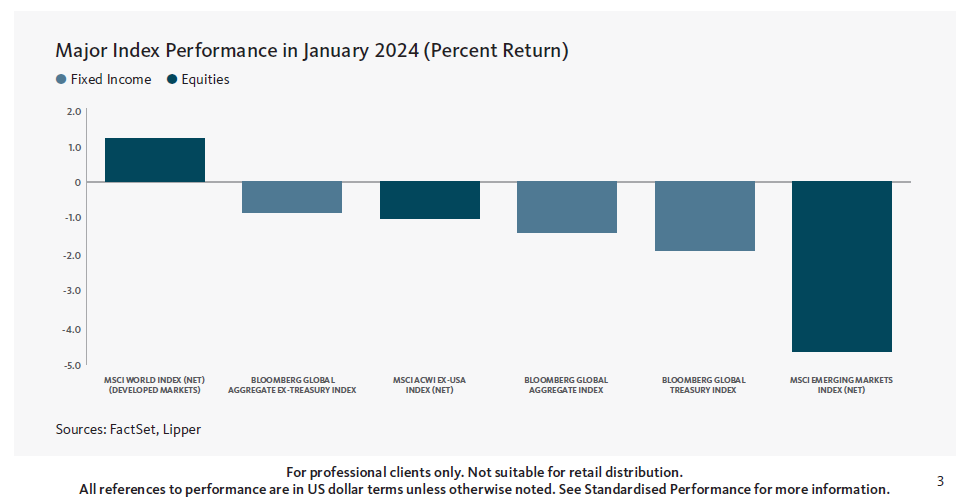

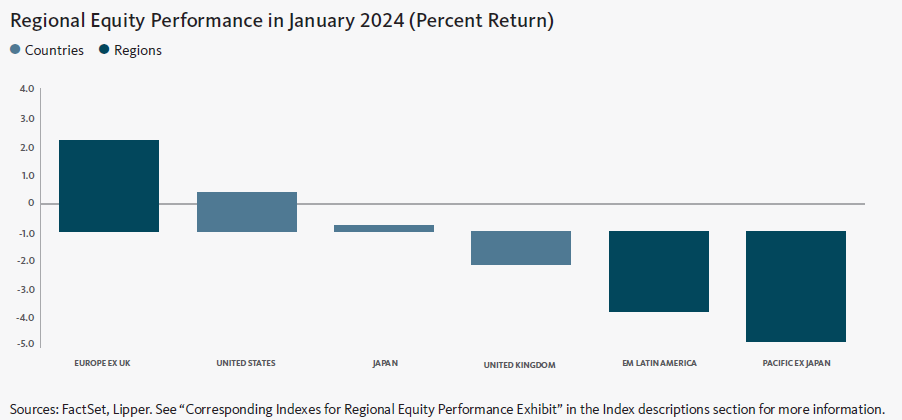

Despite periods of volatility, developed equity markets finished in positive territory in January 2024, as investors’ optimism about the global economy offset concerns regarding geopolitical tensions in the Middle East and Ukraine. Meanwhile, emerging markets recorded negative returns for the month. North America led the major developed markets in January due to strong performance in the U.S., which offset a downturn in Canada. The Pacific ex Japan region was the primary market laggard due mainly to weakness in Hong Kong and Singapore. Europe was the top-performing region within emerging markets for the month, led by strength in Greece and Hungary. Conversely, Chinese stocks posted the most notable losses among emerging markets in January.1

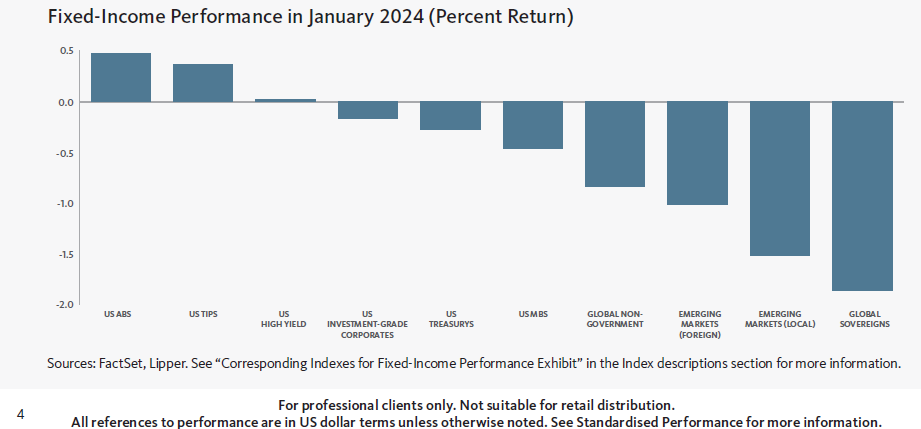

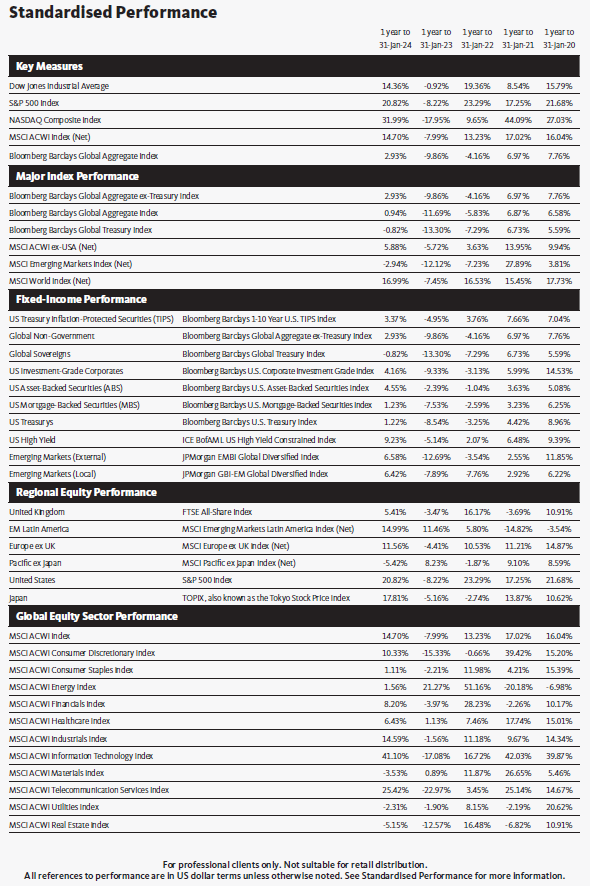

Global fixed-income assets, as represented by the Bloomberg Global Aggregate Bond Index, declined 1.4% in January. High-yield bonds saw flat performance for the month, but led the U.S. fixed-income market; corporate bonds and U.S. Treasury securities recorded modest losses.2 Treasury yields moved somewhat higher for all maturities greater than one year. Yields on 2-, 3-, 5- and 10-year Treasury notes increased 0.04%, 0.04%, 0.07% and 0.11%, respectively, over the month. The spread between 10- and 2-year notes narrowed from -0.35% to –0.28% in January, and the yield curve remained inverted.3

As widely anticipated, the Federal Open Market Committee (FOMC) maintained the federal-funds rate in a range of 5.25% to 5.50% following its meeting on 30-31 January, but cited progress in slowing inflation. In a statement announcing the continuation of the pause in its rate-hiking cycle, the FOMC appeared open to interest-rate cuts later this year, noting that “the risks to achieving [the Fed’s] employment and inflation goals are moving into better balance.” However, the central bank cautioned that rate cuts are not imminent, as it “does not expect it will be appropriate to reduce the target [federal-funds] range until it has gained greater confidence that inflation is moving sustainably toward 2 percent…The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.”

On the geopolitical front, the U.S. and U.K. (with support from Australia, Bahrain, Canada, and the Netherlands) conducted airstrikes on several targets in Yemen in the early morning of 23 January (local time in Yemen). The military action was in response to Houthi rebel attacks on commercial shipping in the Red Sea off the coast of Yemen. The Houthi movement is an Iran-backed militant group that seized Sanaa, Yemen’s capital, in 2014. The group has attacked U.S. military bases in Iraq and Syria, as well as numerous commercial ships in the Red Sea, forcing international shipping companies to reroute their vessels around the Cape of Good Hope in South Africa, putting upward pressure on freight costs. In late January, an Iran-backed militia group conducted a drone attack at a U.S. military base in Jordan, killing three U.S. troops. President Joe Biden indicated that the U.S. would retaliate for the attack.

Global commodity prices, as measured by the Bloomberg Commodity Total Return Index, moved modestly higher in January. The West Texas Intermediate and Brent crude oil prices initially spiked in response to the military action in Yemen before retreating, ending the month with gains of 5.9% and 4.6%, respectively. Oil prices also benefited from energy firms’ larger-than-expected draws of crude oil from storage. The New York Mercantile Exchange (NYMEX) natural gas price fell 9.8% in January amid declining demand due to above average winter temperatures in the U.S.

The gold spot price fluctuated, falling amid the rise in U.S. Treasury yields (the gold price typically moves inversely to bond yields) for most of the month before rallying during the last week of January in response to relatively strong U.S. economic data and declining Treasury yields. The gold price ended the month with a modest loss of 0.2%. The 5.2% decrease in wheat prices during the month was attributable to relatively weaker demand for exports from the U.S.4

Economic data

U.S.

The Department of Labor reported that the U.S. consumer-price index (CPI) rose by a higher-than-expected rate of 0.4% in December following a 0.1% uptick in November. The CPI advanced 3.4% year-over-year—up from the 3.1% annual rise in November. Housing and energy costs were the largest contributors to the month-over-month rise in the CPI, increasing 0.5% and 0.4%, respectively. Food prices were up 0.2% for the month and advanced 2.7% over the previous 12-month period. The 3.9% rolling 12-month rise in core inflation, as measured by the CPI for all items less food and energy, was the smallest annual increase since August 2021, and was marginally lower than the 4.0% year-over-year rise in November. Core inflation was up 0.3% in December, matching the increase during the previous month.

According to the initial estimate from the Department of Commerce, U.S. gross domestic product (GDP) grew at an annualised rate of 3.3% in the fourth quarter of 2023, down from the 4.9% rise in the third quarter, but significantly exceeding expectations. The U.S. economy expanded by 2.5% for the 2023 calendar year, topping 2022’s 1.9% annual gain, bolstered by increases in consumer spending—which comprises more than two-thirds of U.S. GDP—and nonresidential fixed investment (purchases of both nonresidential structures and equipment and software). The main contributors to GDP for the fourth quarter included consumer spending, exports, state and local government spending, and nonresidential fixed investment. The government attributed the lower economic growth rate in the fourth quarter relative to the previous three-month period primarily to slowdowns in private inventory investment (a measure of the changes in values of inventories from one time period to the next) and federal government spending.

U.K.

The Office for National Statistics (ONS) reported that consumer price inflation in the U.K., as measured by the Consumer Prices Index (CPI), rose 0.4% in December, following a decline of 0.2% in November. The CPI rose 4.0% year-over-year, up marginally from the 3.9% annual increase during the previous month. The largest contributors to the 12-month rise in inflation included alcohol and tobacco, as well as food and non-alcoholic beverages. These more than offset a decline in for housing and housing services costs. Core inflation, which excludes volatile food prices, rose at an annual rate of 5.1% in December, matching the year-over-year increase in November.5

According to the initial estimate of the ONS, U.K. GDP fell 0.2% over the three-month period ending 30 November, 2023 (the most recent reporting period) compared to the previous three-month period ending 31 August. However, GDP rose 0.2% year-over-year in December. Production output decreased 1.5% over the three-month period, hampered mainly by a notable slump in manufacturing. The services sector was flat relative to the previous three-month reporting period, as growth in human health and social work activities, and education was offset by weakness in information and communication, as well as arts, entertainment, and recreation. Output in the construction sector fell 0.6% during the period, attributable primarily to a significant downturn in new work, particularly private new housing.6

Eurozone

Eurostat pegged the inflation rate for the eurozone at 2.9% for the 12-month period ending in December, up from the 2.4% annual increase in November. Prices for food, alcohol and tobacco rose 6.1% year-over-year in December, but the pace of acceleration slowed from the 6.9% annual rate for the previous month. Costs for services and non-energy industrial goods were up 4.0% and 2.5%, respectively, year-over-year. Conversely, energy prices fell 6.7% over the previous 12 months following an 11.5% decline in November.

Core inflation, which excludes volatile energy and food prices, rose at an annual rate of 3.4% in December, down 0.2 percentage point from the 3.6% year-over-year increase in November.7

According to Eurostat’s preliminary estimate, eurozone GDP was flat in the fourth quarter of 2023, a slight uptick from the 0.1% decline in the third quarter, but increased 0.5% for the 2023 calendar year. The economies of Portugal and Spain were the strongest performers for the fourth quarter, expanding 0.8% and 0.6%, respectively. Conversely, Ireland’s GDP fell 0.7% during the period.8

Central banks

During a news conference following the FOMC’s meeting on 31 January, Fed Chair Jerome Powell said, “It will likely be appropriate to begin dialing back policy restraint at some point this year, but the economy has surprised forecasters in many ways since the pandemic and ongoing progress toward our 2% inflation objective is not assured.” When asked if the Fed has achieved a “soft landing” (in which growth and inflation slow but the economy does not enter a recession), Powell responded, “We still have a ways to go. We’re encouraged by the progress, but we’re not declaring victory at this point.”

Following its meeting on 31 January, the Bank of England (BOE) left the Bank Rate unchanged at a 15-year high of 5.25%. However, the rate decision was not unanimous; two of the nine BOE Monetary Policy Committee (MPC) members supported a 25-basis point increase, while another member voted for a reduction of 25 basis points. In its announcement of the rate decision, the BOE commented, “The Committee judges that the risks around its modal CPI inflation projection are skewed to the upside over the first half of the forecast period, stemming from geopolitical factors. It now judges that the risks from domestic price and wage pressures are more evenly balanced, meaning that, unlike in previous forecasts, there is no difference between the MPC’s modal and mean projections at the two and three-year horizons.”

The European Central Bank (ECB) left its benchmark interest rate unchanged at 4.50% following its meeting on 25 January. In a statement announcing the rate decision, the ECB’s Governing Council stated, “Aside from an energy-related upward base effect on headline inflation, the declining trend in underlying inflation has continued, and the past interest rate increases keep being transmitted forcefully into financing conditions. Tight financing conditions are dampening demand, and this is helping to push down inflation.” The central bank also reiterated its goal of ensuring that “inflation returns to its 2% medium-term target in a timely manner. Based on its current assessment, the Governing Council considers that the key ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a

substantial contribution to this goal.”

The Bank of Japan (BOJ) left its benchmark interest rate unchanged at -0.1% following its meeting in January. The central bank also maintained the upper yield limit of 1.0% for the 10-year Japanese Government Bond (JGB) that it had established in July 2023 as an “upper bound” rather than a stringent cap. In a statement announcing the monetary policy actions, the central bank noted, “With extremely high uncertainties surrounding economies and financial markets at home and abroad, the [BOJ] will patiently continue with monetary easing while nimbly responding to developments in economic activity and prices as well as financial conditions. By doing so, it will aim to achieve the price stability target of 2 percent in a sustainable and stable manner, accompanied by wage increases.”

SEI’s view

We expect more subdued economic growth in the U.S. in 2024, perhaps deteriorating into a stagnant/mildly recessionary environment along the lines currently seen in much of Europe. While interest rates may no longer be rising, they remain high and are starting to bite harder. Households have smaller savings cushions to draw upon to sustain spending in excess of their incomes. Credit-card usage is up sharply and, as a result, delinquency rates are climbing. The situation is not yet critical or indicative of recession, but households will be more heavily reliant on a continued robust jobs market and strong wage growth in the months ahead. The good news is that the jobs market is still tight. However, there are signs of weakness cropping up.

The U.S. inflation rate has decelerated more quickly in recent months than we had expected. The U.S. led the global acceleration of inflation in 2021 and 2022; in 2023, it led the way down. Both the U.S. and the eurozone have enjoyed a decline in inflation back toward the 2% level, measured on a year over year basis. The U.K. and France have been lagging in terms of inflation levels, but, nonetheless, have registered a rather sharp slowdown from their inflation-rate peaks.

Does the slowdown in inflation mean that central banks can confidently declare “mission accomplished”? In our opinion, the answer is a firm “no.” It is important to note that the bulk of the improvement has come in volatile food and energy prices. We believe that the recent upbeat views regarding the U.S. economic and market outlook for this year have been overly optimistic. Investors are anticipating continued equity market dominance from the “Magnificent Seven” (Apple, Microsoft, Google parent Alphabet, Amazon, Nvidia, Meta, and Tesla), double-digit corporate earnings growth, massive interest-rate cuts from the Fed, and inflation that drops to 2% or lower and remains subdued.

While stock indexes fared notably well in 2023, it is important to note that many widely followed indexes are capitalization-weighted and, therefore, the largest stocks have a disproportionate effect on performance. This was certainly the case last year, as the Magnificent Seven drove the bulk of the gains.

Unlike the stock market, the U.S. bond market’s rally in 2023 was broad, driven by a pivot in central bank policy that saw an end to interest-rate hikes. Despite the upturn in the bond market last year (and falling yields, as bond prices and yields move inversely), as well as a bumpy start to the new year, we think that yields will likely remain more attractive than they have been in decades, which is good news for income-seeking investors.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated.

This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information. Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Not all strategies discussed may be available for your investment.

Information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

For professional clients only. Not suitable for retail distribution.