Monthly Market Commentary: Everything Rallies with Return to Normal in Sight

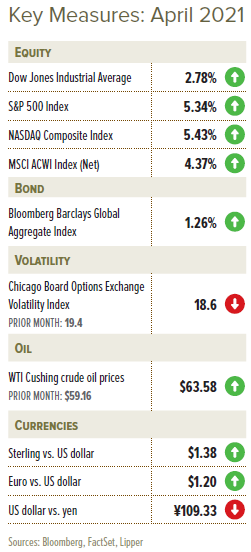

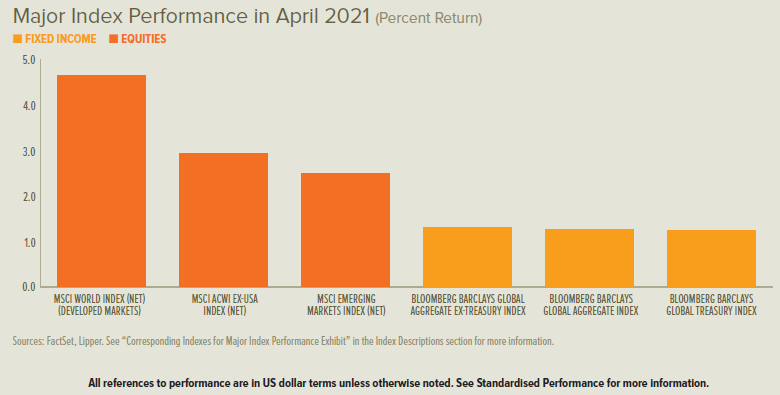

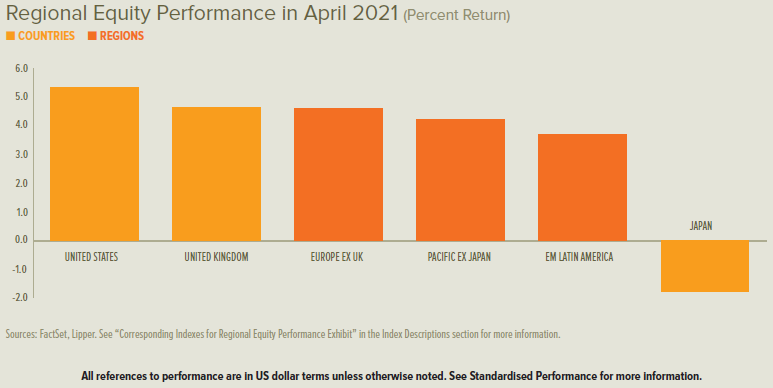

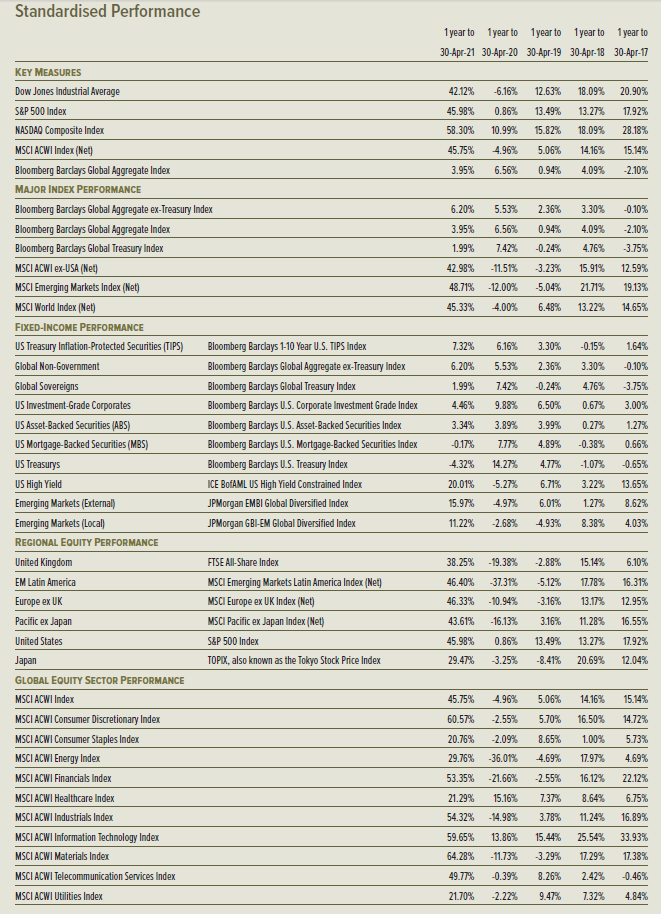

Capital markets posted strong performance across asset classes in April. Once again, equities raced ahead around most of the world, with developed markets leading emerging markets. US shares were the top-performing major market, followed by Europe, the UK, Hong Kong, and then mainland China. Japanese shares declined for the month.

Government-bond rates underwent varying changes across different regions during April. In the UK, rates moved higher for gilts with maturities of less than 13 years and lower for gilts of more than 13 years—resulting in a flatter yield curve. Eurozone government-bond rates increased across all maturities; long-term rates rose by more than short-term rates, leading to a steeper curve. US Treasury rates were mixed across short-term maturities, while intermediate- and long-term rates fell, creating a flatter curve.

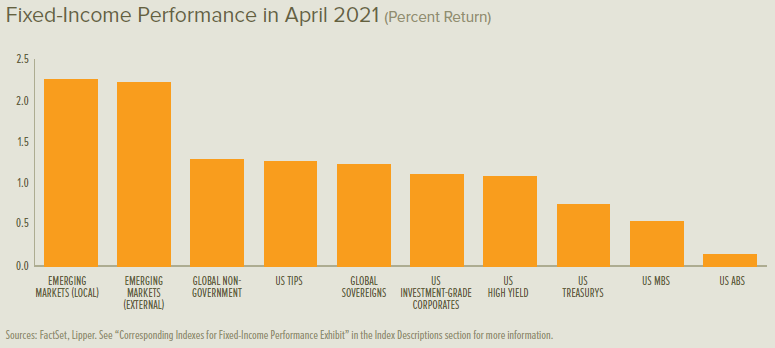

The pause in interest-rate increases during April was beneficial to bonds and the broader fixed-interest universe, which generally delivered positive returns. Commodities also continued to increase in price during April, with the Bloomberg Commodity Index advancing by 6.92% and West Texas Intermediate crude oil rising by 7.47% to $63.58 per barrel.

COVID-19 infection rates dropped in Europe during April to less than 150,000 per day from more than 200,000 per day in the prior month. However, progress was uneven across countries. For example, the seven-day moving average of new cases in Germany at the end of April was 29% below its all-time peak—while France reported a 60% reduction and the UK infection rate plunged by 96% to its lowest level since last August. At the same time, more than 20% of the UK population was fully vaccinated by the end of April compared to 10% of the French population and 8% of the German population.

Non-essential retail businesses reopened in England on 12 April in keeping with the second stage of the country’s four-part reopening plan. Restaurants and pubs were still limited to outdoor seating, but they were no longer bound to curfews. The next stage—set for 17 May, pending continued progress on lower infection rates—will allow restaurants and pubs to provide indoor service and multiple households to congregate inside.

The US began April in the midst of a mild increase in new COVID-19 cases, but returned to the March low by the middle of the month. President Joe Biden’s administration announced in mid-April that all adults in the US are eligible for vaccination; by the end of the month, about 30% of the US population was fully vaccinated. A temporary halt in the use of Johnson & Johnson’s one-dose vaccine (due to concerns about a serious potential side effect) was resolved before the end of April. Globally, more than 1.1 billion doses of COVID-19 vaccine were administered by the end of April.

Asia continued to struggle with a severe outbreak centred in India that began in March; it expanded drastically in April, accounting for the overwhelming majority of new global cases, which reached an all-time high of 15.5 million new cases, dwarfing the previous peak of 3.9 million. This outbreak initially spread to other countries in the region, but appeared to crest in India by late April.

President Biden unveiled a set of spending proposals in late April during a joint address to the Congress that would total about $4 trillion, but which would be funded mostly by tax increases. The proposed plans are split into two groups: The American Jobs Plan, which focuses primarily on infrastructure, would cost $2.3 trillion and be funded by an increase in corporate taxes; and The American Families Plan, which focuses on child care, education, healthcare and a range of other issues, would cost $1.8 trillion and be funded by higher taxes for top earners.

Economic Data

- UK manufacturing activity accelerated further into high-growth territory during April—reaching a 321-month high according to IHS Markit/CIPS— building on a recovery that unfolded throughout most of the first quarter after a brief pause around Brexit at the beginning of 2021. UK services growth accelerated in April to its highest rate of expansion in 80 months. The UK claimant count (which calculates the number of people claiming Jobseeker’s Allowance) remained at 7.3% in March as the total number of claimants increased from 2.66 million to 2.67 million. The broad UK economy expanded by 0.4% in February after contracting by 2.9% in January.

- Eurozone manufacturing growth continued at a red-hot pace during April, reaching the highest level since the 1997 inception of IHS Markit’s eurozone manufacturing purchasing managers’ index (PMI) survey. Meanwhile, eurozone services activity improved modestly in April, moving from a mild contraction to a mild expansion. The eurozone unemployment rate fell from 8.2% to 8.1% in March despite consensus expectations for an increase. Overall eurozone economic activity contracted by 0.6% during the first quarter of 2021 and by 1.8% year over year, compared to contractions of 0.7% and 4.9%, respectively, in the prior quarter.

- US manufacturing activity continued to expand at or near multi-decade highs according to multiple PMI surveys. Services growth accelerated from an already strong pace, reaching the highest rate since the 2009 inception of the IHS Markit US services PMI survey. Jobless claims fell in late April below 500,000 per week—a sharp improvement from an early-month reading of 742,000, and the lowest level since early March 2020. Overall US economic growth jumped to a 6.4% annualised rate during the first quarter of 2021 from 4.3% in the prior quarter.

Central Banks

- The Bank of England’s (BOE) Monetary Policy Committee (MPC) did not hold a meeting during April. In its March meeting, the MPC maintained the bank rate at 0.1% and retained an £895 billion maximum allowance for asset purchases; it does not intend to increase rates “at least until there is clear evidence that significant progress is being made in eliminating spare capacity and achieving the 2% inflation target sustainably.”

- The European Central Bank (ECB) held course at its late-April monetary policy meeting, increasing the pace of asset purchases under its €1.85 trillion Pandemic Emergency Purchase Programme (PEPP). This move, previously announced in March, is intended to counter the negative economic impact of rising rates. ECB President Christine Lagarde expressed that any decisions about winding down PEPP would be data dependent, and that it would be premature to do so today given the current economic environment.

- The US Federal Open Market Committee (FOMC) made no significant policy changes following its late-April meeting: the federal-funds rate remained near zero and asset purchases were set to continue at a level of $80 billion in US Treasurys and $40 billion in agency mortgage-backed securities per month. Like Lagarde, US Federal Reserve (Fed) Chair Jerome Powell squashed questions about tapering the central bank’s extraordinary support, noting that “we’re 8.5 million jobs below where we were in February of 2020” and are therefore far from the Fed’s mandate to support full employment.

- The Bank of Japan (BOJ) made no immediate changes to its monetary policy at its late-April meeting after announcing a shift in March from programmatic market interventions to a more as-needed approach. The BOJ shared the possibility that its emergency pandemic-related programmes could be extended past their scheduled September 2021 end dates if economic conditions warrant.

SEI’s View

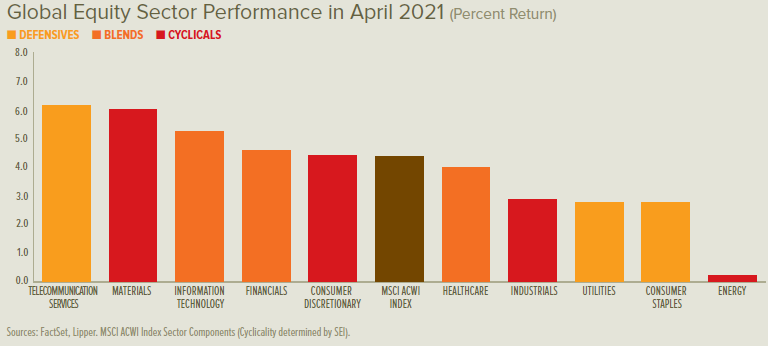

The war against COVID-19 is not over, but the path to victory has become clearer. Investors are anticipating the return to a more normal world. This was reflected in the rapid rise in bond yields during the first quarter, the most important change in the financial environment so far this year. This jump caused outsized price drops in long-term fixed-income securities and helped fuel the sharp equity-market rotation away from expensively priced growth shares and into value-oriented and cyclical sectors, both in the US and internationally.

With the passage of the latest US fiscal stimulus package, the cumulative amount of US fiscal support since March 2020 totals a remarkable $6 trillion—approaching 30% of US GDP. The Fed has gone to great lengths to protect the bond market from the rising tide of Treasury issuance with its purchases of outstanding issues. In the 12 months ended March 2021, the Fed bought $2.3 trillion of Treasury securities; as of February, the federal deficit over the prior 12 months amounted to $3.55 trillion.

Higher bond yields may cause bouts of indigestion for equities but should not derail the bull market. We expect cyclical and value-oriented shares to continue to advance relative to growth and defensively oriented sectors. In most cycles, value shares outperform growth when the yield curve is rising or is especially wide (rates on long-term Treasury bonds are well above those on short-term securities). Value’s performance against growth bottomed on 1 September, and has driven higher ever since.

While value-oriented shares have been making a comeback against growth in the US, other countries’ equity markets are making a comeback against the US.

As spring arrives and lockdowns end in the UK on the back of successful vaccination efforts, we expect the country to experience a strong recovery in consumer demand and business activity that outpaces the rest of Europe.

UK government policy remains supportive in the near-term. But the recently proposed fiscal budget appears rather restrained compared to measures taken by the Biden administration, adding only about 3% of UK GDP to the budget deficit for the 2021-to-2022 fiscal year. From the 2023-to-2024 fiscal year and beyond, policy actions are projected to begin reducing the deficit, mostly through increasing the corporation tax rate from 19% to 25% and through the freezing of income tax thresholds.

Although not as high as the valuation metrics found in the US equity market, shares outside the US still appear expensive. Currently, the MSCI World ex USA Index is priced at almost 17 times the earnings per share forecast for the next 12 months, the highest level since 2004.

To repeat, developed-country equity markets still look cheap compared to US equities. The forward price-to-earnings ratio for the MSCI USA Index is above 23. The MSCI World ex USA Index therefore trades at an unusually wide 27% discount. Although longer-term growth differentials justify a structurally higher multiple for US equities, rebounding economies and rising interest rates should lead to a narrower valuation gap.

The jump in US bond yields this year has raised investor concerns that emerging markets will be the victims of a 2013-style taper tantrum. Rising rates are a headwind, but we believe emerging economies are generally in a better position to withstand the pressure than they were eight years ago. Strong growth in the world economy over the next year should help lift most emerging markets.

World trade volumes, for example, had already reached pre-pandemic levels by the end of last year. Over the course of 2021, the expansion in trade should continue. When trade volumes are strong, developing country equity markets tend to perform well against those of economically advanced countries.

We believe the economic backdrop strongly supports cyclical and value oriented equities in the emerging markets, just as it does in developed markets. The MSCI Emerging Markets Value Index (total return) is highly correlated with industrial commodity prices, which have already vaulted higher from their year-ago lows.

Demand for metals and other commodities will be stoked by strengthening manufacturing and construction activity in the US and China, recovery in Europe and Latin America as vaccines become more widely available, the global push into electric vehicles and other climate projects, and the major infrastructure package that is next on the Biden Administration’s to-do list.

Emerging economies also look less susceptible to a 2013-style taper tantrum because their external positions are much healthier. Current account balances as a percentage of GDP are generally much smaller than they were eight years ago.

Emerging-market local-currency and US dollar bond yields have moved higher in the year to date, but the increase has been modest so far. Option-adjusted spreads are still near their lows of the past three years, certainly not qualifying as a taper tantrum.

Granted, some big countries face continuing problems. Besides Turkey, debt dynamics among the larger countries appear most worrying in Brazil and South Africa. However, most of the debt in these two countries is denominated in local currency, allowing their governments to engage in some form of financial repression (like quantitative easing) in order to temper the pressure on their bond markets.

SEI’s base case is an optimistic one. Developing countries will likely take longer than developed nations to reopen fully due to vaccination distribution challenges. Yet, even these countries will benefit economically from the upswing in developed-market consumer demand.

Having confidence is not the same as being complacent, however. Beyond COVID-19 concerns, we expect investors will be increasingly focused on the next multi-trillion dollar US spending package, which will include tax increases on corporations and high-income households. Compromises will be needed to keep the Democratic caucus unified.

Generally speaking, the tax and regulatory changes championed by the Biden administration are not considered business- or equity-market friendly. But the same could be said of the economic policies pursued during President Barack Obama’s administration. That did not prevent one of the strongest and most enduring bull-market runs in US history. We caution against making broad asset-allocation changes based on perceived shifts in the political winds.

As for monetary policy, we will be watching whether the US Fed can maintain its stance of a near-zero federal-funds rate through 2023. If the acceleration in inflation proves stronger and longer-lasting than investors expect, bond yields could climb appreciably from today’s levels.

If the Fed accelerates policy rate hikes, we would expect a neutral-to-negative reaction in equities and other risk assets. Suppressing the rise in bond yields through even more aggressive policy actions, on the other hand, could lead to a weaker US dollar and a sharper investor focus on inflation-hedging. Equity valuations could get even more expensive than they are now as investors grow even more exuberant. Interesting times, indeed.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Cyclical stocks: Cyclical stocks or sectors are those whose performance is closely tied to the economic environment and business cycle. Managers with a pro-cyclical market view tend to favour stocks that are more sensitive to movements in the broad market and therefore tend to have more volatile performance.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Forward price-to-earnings (PE) ratio: The forward PE ratio is equal to the market capitalisation of a share or index divided by forecasted earnings over the next 12 months. The higher the PE ratio, the more the market is willing to pay for each dollar of annual earnings.

Hedging: Hedging is an investment technique designed to try to limit potential losses from swings in market value (price changes) of stocks, bonds, commodities or currencies.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Mortgage-backed securities: Mortgage-backed securities (MBS) are pools of mortgage loans packaged together and sold to the public. They are usually structured in tranches that vary by risk and expected return. Agency means that the debt is guaranteed by a government-sponsored entity.

Options: Options are contracts that provide a buyer with the right, but not the obligation, to buy or sell a security at an agreed-upon price.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset-purchase programme of private and public sector securities established by the ECB to counter risks to monetary-policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Purchasing managers’ index (PMI) survey: A PMI survey is compiled from responses to questionnaires sent to a panel of purchasing managers working, for example, in the manufacturing and business services sectors.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Taper tantrum: Taper tantrum describes the 2013 surge in US Treasury yields, resulting from the US Federal Reserve’s announcement of future tapering of its policy of quantitative easing.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Index Descriptions

The Bloomberg Commodity Index is composed of futures contracts and reflects the returns on a fully collateralized investment in the Index. This combines the returns of the Index with the returns on cash collateral invested in 13-week (3-month) U.S. Treasury bills.

The MSCI Emerging Markets Value Index measures the performance of large- and mid-cap stocks exhibiting overall value style characteristics across 27 emerging-market countries.

The MSCI USA Index measures the performance of the large- and mid-cap segments of the US market. The Index covers approximately 85% of the free float-adjusted market capitalisation in the US.

The MSCI World Index is a free float-adjusted market-capitalisation-weighted index that is designed to measure the equity-market performance of developed markets.

The MSCI World ex USA Index is a free float-adjusted market-capitalisation-weighted index that is designed to measure the equity market performance of developed markets, excluding the US.

The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.