Monthly Market Commentary: Equity Hot Streak Barrelled into Late Summer

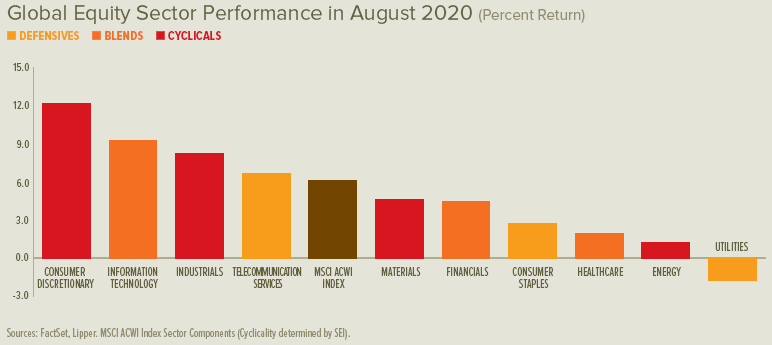

Strong equity-market performance continued around most of the world in August, led by Hong Kong, Japan and the US. Europe and the UK followed at a distance despite generating elevated one-month returns. Latin America suffered a sharp decline during the period as COVID-19 cases appeared to plateau at high levels there. A steep selloff in early September offset part of August’s gains, particularly among the US companies that had led the rally.

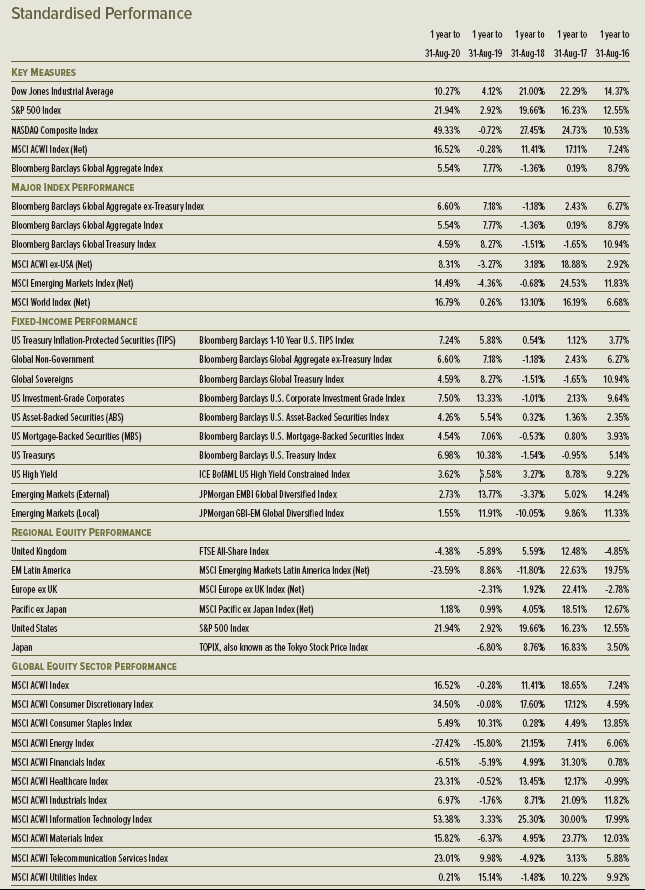

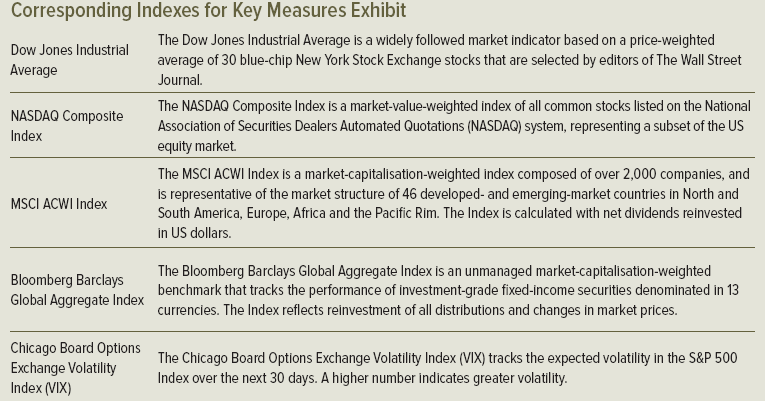

The S&P 500 Index (a broad measure of US shares) registered a new all-time high in late August, marking the fifth consecutive month of gains since the dramatic early-2020 selloff1. The US dollar continued to fall versus a basket of major currencies during August, albeit at a slower pace compared to its sharp July decline, settling at its lowest level in more than two years.

Government-bond yields increased around the developed world. In the UK, eurozone and US, long-term government rates rose by more than short-term rates, leading to steeper yield curves.

UK and EU representatives made only marginal progress toward a trade deal during August. Negotiations hit an apparent impasse as the EU made two demands that had previously been declared non-starters by UK negotiators: (1) continued EU fishing rights in UK waters, and (2) UK adherence to EU state-aid rules that would limit the likelihood of anti-competitive subsidies to UK industry.

The US presidential election cycle formally progressed to its final phase before Election Day, as President Donald Trump accepted the Republican Party’s nomination and former Vice President Joe Biden accepted the Democratic Party’s nomination at their respective quadrennial conventions during August. Fresh off the July commencement of the United States–Mexico–Canada Agreement (USMCA), the Trump administration announced in August a re-imposition of a 10% tariff on Canadian aluminium that was suspended in May 2019 during USMCA negotiations.

Tensions between the US and China spilled into the social-media sphere as the Trump administration took a series of actions to wrest control of the US branch of TikTok, a popular video-sharing app owned by Beijing-based Bytedance. In early August, President Trump signed an executive order to bar Americans from conducting business with ByteDance after mid-September. Several major US companies in the software, retail and private-equity industries announced intentions to bid on TikTok’s US operations; by late August, ByteDance sued the US government over its impending ban and forced sale. China, for its part, contended that any sale of TikTok assets to a US company is subject to Chinese government approval.

Aside from social-media drama, the US-China relationship was strained after a recent Beijing-imposed national-security law drove the Trump administration to end its extradition treaty with Hong Kong. In addition, the US imposed sanctions on senior government officials in China and Hong Kong, including Hong Kong’s Beijing-appointed Chief Executive Carrie Lam, over their suppression of political dissent in the territory. Finally, the US formalised accounting rule changes, mandating that US-traded Chinese firms comply with US accounting standards by 2022 or else de-list from US securities exchanges. With regard to the ongoing global pandemic, the US and Hong Kong each reported their first confirmed case of COVID-19 re-infection.

In late August, Japanese Prime Minister Shinzo Abe announced his intention to resign due to issues with his personal health. Abe is the longest-serving prime minister in Japan’s history and a chief proponent of a multi-pronged policy approach to the country’s economic revival, which was dubbed “Abenomics.”

Economic Data

- The UK’s healthy rebound in manufacturing activity accelerated during August. A preliminary report on activity in the services sector during the same month depicted an increase in the UK’s already-strong growth. UK mortgage approvals jumped to 66,300 in July from 39,900 in June, while consumer credit grew by £1.2 billion in July after contracting during the prior month; both measures exceeded consensus expectations for July.

- The eurozone’s recovery in manufacturing activity remained slow during August. Services sector activity eased to a near standstill, according to an early report. The number of loans granted to non-financial corporations increased by 7% in July, keeping pace with the prior two months. The eurozone unemployment rate inched higher from 7.7% to 7.9% in July.

- US manufacturing activity improved during August on July’s modest growth, despite a persistent contrast between strong new orders and shrinking employment. A preliminary report showed that activity in the services sector accelerated during August after halting in the prior month. New US jobless claims briefly dipped below 1 million per week in mid-August before rising back to about 1.1 million later in the month. Existing US home sales surged by 24.7% in July amid historically low mortgage rates; by contrast, the number of delinquent mortgages insured by the US Federal Housing Administration reached 16% in August, the highest level on record since 1979.

Central Banks

- The Bank of England’s Monetary Policy Committee voted to leave its key lending rate unchanged at 0.1% and to maintain its existing level of asset purchases at £745 billion. The central bank also lowered its economic outlook—from expecting a complete recovery by mid-2021 to anticipating a return to pre-pandemic levels of economic activity no earlier than late 2021.

- The US Federal Open Market Committee (FOMC) did not hold a meeting in August; however, it announced major updates to its monetary-policy approach. The most significant change centred on the US central bank’s new average inflation target, which highlights its explicit willingness to allow above-target inflation following periods of below-target inflation. This change indicates that the FOMC will let the US economy run hotter than in the past before taking policy action to temper growth.

- Neither the European Central Bank (ECB) nor the Bank of Japan (BOJ) held monetary policy meetings in August after having both made no changes at their respective mid-July meetings.

SEI’s View

Despite mounting rates of infection, hospitalisation and death amid an ongoing pandemic, and the unprecedented side effect of a frozen global economy—stock markets around the world have managed to make a resounding recovery.

Our working assumption is that there will likely be another significant wave of infections going into the so-called flu season throughout autumn and winter in the northern hemisphere. The question is, how disruptive will it be to the global economy?

Even if a sustainable economic recovery gets under way, investors seem to be ignoring the possibility that it may be a long time before most companies achieve previous levels of profitability. The after-tax profit margins of US domestic businesses were already on a declining trend before the onset of the virus and shelter-in-place orders.

Profit margins around the globe will likely remain well below their previous peaks as long as COVID-19 remains a severe health threat. Most businesses are expected to endure varying degrees of lower sales, higher costs and a decline in productivity. There also will probably be an extra burden on industries that anticipate needing extra inventory on hand in the event of future shortages and supply-chain disruptions caused by periodic flare-ups of the virus. “Just-in-time” inventory management will likely turn into “just-in-case” inventory management, thereby tying up cash. Supply chains will likely be diversified over time, a process that was already under way as a result of the trade war between China and the US.

The extraordinary March-to-April economic lockdown in the US necessitated fiscal measures unparalleled in both scope and speed of implementation 4. The result has been a tsunami of red ink. As of 2 September 2020, the Congressional Budget Office projected the deficit will reach 16% of US GDP in 2020, and improve to 8.6% of US GDP in 2021. US debt relative to GDP is forecast to rise to 104.4% by the end of fiscal year 2021 versus 79.2% at the end of fiscal year 2019.

These are unsettling numbers. Many investors may wonder whether such a surge in government debt will provoke an economic crisis even after the pandemic runs its course. We don’t think that it will. The US has a large, dynamic economy and deep capital markets.

The policies pursued by the Federal Reserve have also served to keep interest rates low. Its balance sheet has ballooned this year, far exceeding the increases logged by the ECB or the BOJ.

The US certainly is not alone in engaging in a huge fiscal response that is then monetised by the central bank. In our opinion, governments are treating the fight against COVID-19 like they would a war. As many resources as possible are being thrown into the fight, supported by debt issuance that is absorbed primarily by the central banks.

Those who remember the 1970s are understandably worried by the inflationary potential of such extraordinary debt monetisation. If it does lead to inflation, it probably won’t be any time soon, in our opinion. Given our view that the economy will remain below full utilisation of labour or productive capacity for the next few years, we believe inflation is unlikely to break out of the 0%-to-3% range of much of the past decade.

Investors do not seem too concerned about the speed of Europe’s economic recovery or the impact of the health crisis on countries’ fiscal positions. The bond yields of the most economically-fragile countries remain close to those of German bund yields, although spreads have widened from pre-pandemic levels. The ECB has been quite successful in short-circuiting the liquidity crisis and flight-to-safety that threatened the euro area’s financial structure.

COVID-19 has pushed Brexit concerns off the front pages. Yet as the 31 December transition deadline nears, the post-divorce settlement could become an economic factor nearly as important as a second wave of the virus. The UK and EU should probably reach a deal on their trading relationship by at least 31 October to allow time for countries to approve the treaty into law before the end of 2020. Any free-trade agreement would require the UK to agree to permanently align its rules and regulations to those of the EU on an array of matters. The UK would essentially bear much of the EU membership cost without having a voice at the table that sets the rules. It is becoming increasingly likely that there either will be a modest agreement that includes tariffs, or (in the worst-case scenario) a no-deal result that falls back on the World Trade Organization’s most-favoured-nation rules.

While many factors determine equity performance, it has correlated in the emerging-market space with the extent of economic disruption caused by the virus. Asian and central European countries have pulled back the most on their mandates to restrict movement and social interaction. Latin America and India have eased some of those constraints, but not nearly as much as the other two regions. We continue to keep close tabs on China, as it was the first to mandate lockdowns and first to unlock activity. We expect recovery patterns elsewhere in the world to follow that of China.

Central banks in the emerging world are also doing their part to help restore their economies. Interest rates have come down in almost every country in recent months, to record-low levels in many cases. In addition, a long list of emerging-country central banks—including those with shakier reputations, such as South Africa and Turkey—are either buying or planning to buy their government’s debt. We think this debt-monetisation may lead to a future inflation problem.

It’s been said many times that bull markets climb a wall of worry. Maybe now they must learn to swim through waves of worry that include:

- The possibility of a second wave of COVID-19 infections (or, arguably, a continuation of the first wave in some countries) that may force another round of extensive lockdowns and shelter-in-place orders, which could lead to a double-dip recession

- A possible breakdown of political consensus regarding the way forward as economies struggle to regain strength

- The likelihood that economic recovery will take at least a year, and likely longer—and that few economies are apt to rebound to pre-pandemic levels, even if most countries manage to avoid a disruptive second wave of the virus

- Expectations that companies will face higher costs and increased inefficiencies as taxes will almost certainly rise across many economies in the years ahead, and bankruptcies and defaults will climb after government aid programs expire

We believe that an ebb and flow of assorted concerns in the coming months will continue to spark volatility across financial markets. Such periods of instability are expected in any long-term investing plan; as such, we are just as prepared as always at SEI to navigate the current wave of deep uncertainty.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Congressional Budget Office (CBO): The US CBO produces independent, nonpartisan analyses of budgetary and economic issues to support the US Congressional budget process through reports and cost estimates for proposed legislation.

Debt issuance: Debt issuance is when companies or governments raise funds by borrowing money from lenders. The borrower, or issuer, agrees to pay the lender (or bondholder) interest along with full repayment in the future.

Federal Open Market Committee (FOMC): The FOMC is responsible for the open market operations of the US Federal Reserve’s monetary policy tools.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal Stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

The United States–Mexico–Canada Agreement (USMCA): USMCA is a trade deal struck by the three named counties, which took effect on 1 July, thereby replacing the North American Free Trade Agreement (NAFTA).

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.