Monthly Market Commentary: Equities and Bonds Slid Into the New Year on Icy Patch

Global equities tumbled into the New Year with the largest one-month decline since March 2020. Volatility increased slightly during the first half of January, then marched higher before jumping erratically at the end of the month amid dramatic intraday price swings.

The spectre of rising rates in the face of persistently high inflation, coupled with geopolitical uncertainty driven by Russia’s military encirclement of Ukraine, were widely cited as sources of investor consternation.

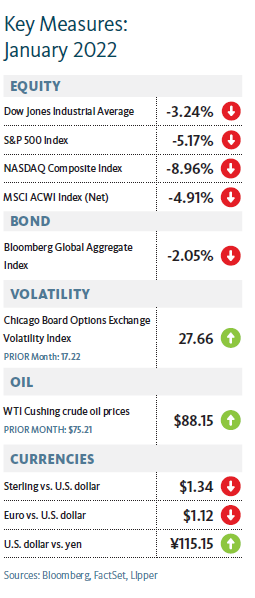

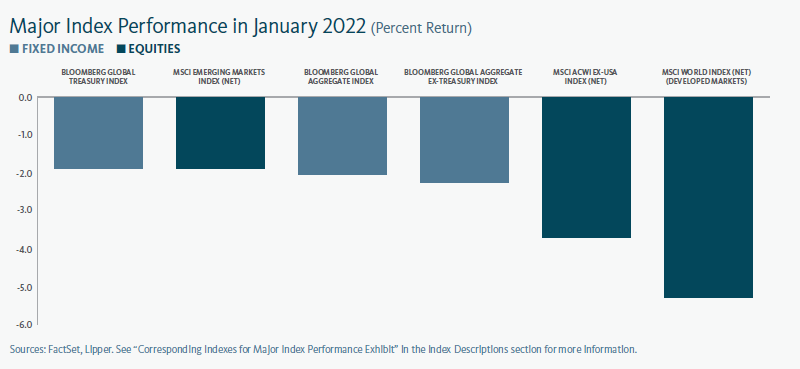

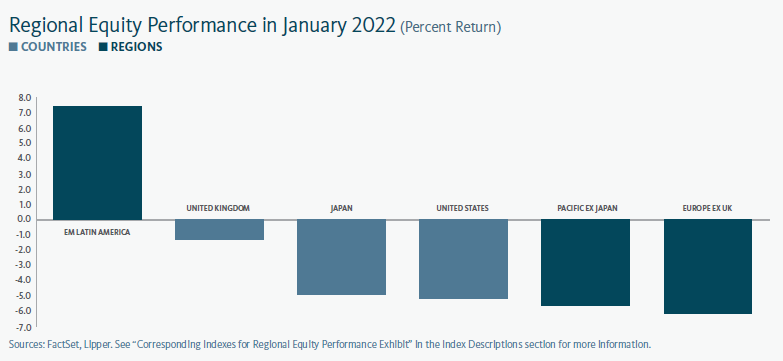

Hong Kong and UK shares stood apart from other major markets as both registered positive performance in January. In emerging markets, huge gains in Latin America more than offset plummeting shares in China; this resulted in a considerably smaller decline in emerging-market equities compared to the selloff in developed-market shares. Japanese equities fell by less than the US, while Europe lagged both.

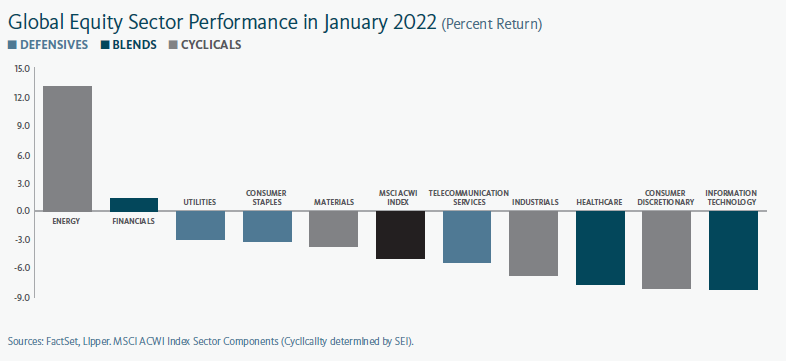

Value-oriented shares fell by considerably less than their growth-oriented counterparts.

Government-bond rates rose across maturities in the UK, eurozone and US. Intermediate-to-long-term rates increased by more than other maturities within the UK and eurozone, while shorter-term rates were the largest gainers in the US.

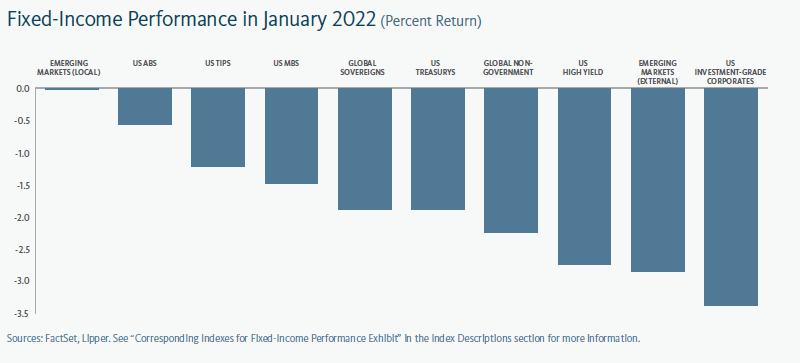

Local-currency emerging-market debt was essentially flat in January, halting a string of recent negative performance; the rest of the fixed-interest universe was negative. Investment-grade corporates had the steepest decline for the month.

Commodity prices continued a seemingly relentless climb. Brent and West-Texas Intermediate crude oil prices were up a respective 14.8% and 17.2% in January, while the Bloomberg Commodity Index advanced by 8.8%.

Shortly after January’s close, UK energy regulator The Office of Gas and Electricity Markets (Ofgem) announced that a cap on energy prices is set to increase by more than 50% this spring, effectively guaranteeing dramatically higher household energy bills. The UK Treasury reportedly intends to help counteract rising living costs via discounts on energy bills, accommodative loans to suppliers, and larger disbursements this year from a reserve established to help low-income households cover spikes in fuel costs each winter.

With a growing Russian military presence at Ukraine’s border, Nord Stream 2—Russia’s not-yet-operational (although completed) natural gas pipeline that runs along the Baltic seabed directly to Germany—became the subject of renewed Trans-Atlantic interest in late January given the leverage it would provide the Kremlin over Europe. US senators introduced a bill directed at preventing the pipeline from being put into service. German Chancellor Olaf Scholz has been scheduled to visit US President Joe Biden at the White House in early February.

US deliveries of liquefied natural gas to Europe via cargo ships accounted for nearly half of the Continent’s record imports in January—helping to restock depleted reserves as year-ago levels nearly tripled.

The US deployed 2,000 troops to Germany and Poland, mobilised 1,000 troops to Romania, and ordered additional troops to stand by for deployment at the beginning of February, after having prepared an initial 8,500 troops to deploy in January.

Economic Data

UK

- The expansion in UK manufacturing activity remained strong in January, generally maintaining the same rate since autumn.

- UK services growth continued at a healthy but subdued pace in January, in line with the prior month.

- The UK claimant count (which calculates the number of people claiming Jobseeker’s Allowance) declined in December for the tenth straight month, by roughly 43,000, lowering the claimant share of the population from 4.8% to 4.7%.

Eurozone

- Manufacturing activity in the eurozone sustained its sharp expansion in January, although at a softer rate than the surge that unfolded in the spring and summer of 2021.

- Growth in eurozone services activity remained modest during January after having returned to its slowing trend in December following a temporary burst of strength in November.

- The eurozone unemployment rate edged down by 0.1% to 7.0% in December, continuing a persistent decline that began in March 2021.

- Overall eurozone economic growth slowed to 0.3% in the fourth quarter from 2.2% in the third quarter, yet accelerated in the year over year to 4.6% from 3.9% in the one-year period ending September.

US

- US manufacturing growth remained healthy in January but continued to slow from the feverish pace that prevailed for most of 2021, reaching the lowest rate of expansion since late 2020.

- The expansion in US services activity almost slowed to a halt in January after a long trend of healthy-to-red-hot levels that extends back to summer 2020.

- New weekly US jobless claims climbed, peaking at 286,000 in mid-to-late January, as receding seasonal employment and a cresting COVID-19 Omicron wave put upward pressure on joblessness.

- The broad US economy grew at a 6.9% annualised rate during the fourth quarter (up from the third quarter’s 2.3% pace) and a 5.7% rate for the 12-month period ending December.

Central Banks

- The Bank of England’s (BOE) Monetary Policy Committee (MPC) reconvened at the beginning of February for its first meeting since raising its bank rate in December 2021, and issued another increase—by 25 basis points (bps) to 0.50%—for the first back-to-back rate hike in 18 years. A large minority of MPC members voted for a larger 50 bps increase to counteract high inflation. The central bank also said it intends to reduce the size of its balance sheet by ceasing to re-invest proceeds from its asset-purchase programme.

- The European Central Bank (ECB) also held its inaugural meeting of 2022 at the beginning of February. It remained committed to the policy path it articulated in December—yet ECB President Christine Lagarde avoided affirming her recent expectation that a 2022 rate increase would be unlikely, and acknowledged that the widespread stress that inflation has caused will likely continue over the short term. She also said that asset purchases would need to conclude before rates can increase; this would necessitate a policy change as asset purchases are currently scheduled to continue on an indefinite basis once they decline in size over the course of 2022.

- The US Federal Open Market Committee (FOMC) met toward the end of January. In its post-meeting statement, the central bank affirmed its expectation that high inflation and a strong labour market will necessitate an increase in the federal-funds rate in the near future; Federal Reserve (Fed) Chair Jerome Powell echoed this in his press conference. The FOMC also confirmed a final $30 billion round of new asset purchases will take place in February before it can consider increasing rates, and it released a statement following its January meeting outlining its principles for reducing the size of its balance sheet. Powell had referred to high inflation as a severe threat earlier in January during his Senate reconfirmation hearing.

- The Bank of Japan (BOJ) was the first major central bank to hold a monetary policy meeting in the New Year, convening in mid-January. While the central bank’s policy orientation remained fixed—with the short-term interest rate at -0.1% and the 10-year government bond yield target near 0%—its expectations increased for higher inflation. The BOJ announced after its December meeting that it would revert purchases of corporate bonds and commercial paper to prepandemic levels beginning in April.

- The People’s Bank of China (PBOC) cut its one-year-loan prime rate by 10 bps to 3.7% in January after having made a smaller cut in December and reducing its reserve-requirement ratio (which dictates the amount of money banks are required to hold in reserves) in the same month.

SEI’s View

Although there have been pockets of speculative behaviour in some areas of the financial world, we do not see the sort of widespread frenzy that would point to a serious equity correction in 2022. The economy would have to slow precipitously for reasons other than the temporary impact stemming from COVID-19 mobility restrictions. The trend in earnings would need to flat-line or turn negative.

We expect a gain in overall US economic activity of around 4% in 2020 appreciably above the economy’s long-term growth potential of 2%. We also expect other countries to continue to post above-average growth as they recover from the past two years’ worth of lockdowns and shortages. With the major exception of China, which continues to pursue a zero-COVID-19 policy, most countries are unlikely to shut down their economies as fiercely or for as long as they did in 2020.

China’s performance in 2022 is one of the key unknowns that will influence global economic growth. Consensus expectations call for a soft landing of the Chinese economy, with gross domestic product (GDP) growing by about 5% in 2022 versus 8% in the past year.

The year ahead promises to be another one of extremely tight labour markets. We think more people will return to the workforce as COVID-19 fears fade, but there likely will still be a tremendous mismatch of demand and supply.

Currently, there are 11.8 million US persons theoretically available to fill 10.9 million job openings—the smallest gap on record9. Wage gains, unsurprisingly, have climbed at their fastest pace in decades over the past year. In the short term, we expect wages to continue their sharp climb as businesses bid for workers.

The UK also is experiencing a pronounced upswing in its labour-compensation trend. We think Brexit and the departure of foreign workers back to the Continent are aggravating the country’s labour shortage. The disparity in compensation trends among the richest industrialised nations also means that policy responses are likely to diverge.

Predicting a bad inflation outcome for 2022 isn’t exactly much of a risk. Where we depart from the crowd on inflation is in the years beyond 2022. We are sceptical that the US Fed will be sufficiently proactive as it struggles to balance full and inclusive employment against inflation pressures that are starting to look more entrenched. We believe this will be the central bank’s biggest challenge in 2022 and beyond.

We also don’t think the Fed’s inflation and economic projections are internally consistent. Since it projects the economy to be even closer to full employment later into 2022 and beyond, we find it hard to understand why price pressures should ease so dramatically.

Even the central banks that are most likely to taper their asset purchases and raise policy rates in the months ahead (the Fed, the BOE and the Bank of Canada) will probably do so cautiously. By contrast, policy rates in emerging economies have already jumped.

It remains to be seen whether this pre-emptive tightening of monetary policy will forestall a 2013-style taper tantrum as the Fed embarks on its own rate-tightening cycle. Although emerging-market currencies have generally lost ground against the US dollar during the past six months, the depreciation hasn’t become a rout (with the exceptions of Turkey and the usual economic basket cases—Argentina and Pakistan). Still, the shift in Fed policy will probably represent a formidable headwind for emerging-market economies in 2022.

The People’s Bank of China (PBOC) cut a key interest rate in December and then again in January, both by modest amounts. These cuts followed a reduction in reserve-requirement ratios aimed at increasing the liquidity available to the economy; it will take a while for any beneficial impact to be felt on China’s domestic economy, and even longer for the world at large.

In addition to the start of a new monetary tightening cycle, some economists have expressed concern about the next “fiscal cliff” facing various countries, the US in particular. While there will be a negative fiscal impulse in the sense that the extraordinary stimulus of the past two years will not be repeated, we argue that the impact should be less contractionary than feared.

Perhaps economists should be more concerned about the negative fiscal impulse in the UK, Canada, Germany and Japan. They are all facing a potential fiscal tightening equivalent to 4% of GDP this year. By comparison, the International Monetary Fund predicts that the cyclically adjusted deficit in the US will contract by less than 0.5% of GDP.

We remain optimistic that growth in the major economies will be buoyed by the strong position of households. In the US, household cash and bank deposits were still almost $2.5 trillion above the pre-pandemic trend as at the end of September. This total is equivalent to almost 14% of disposable personal income. Excess savings in the UK, meanwhile, have reached 10.6% of annual personal disposable income. Euro-area bank balances aren’t quite as high, but still amount to 5% of after-tax income.

Investors always need to deal with uncertainty; we are focused on three main areas of geopolitical risk. We believe the most important flashpoint in terms of near-term probability and economic impact is the Russian build-up of troops on the Ukrainian border. An invasion of Ukraine could lead to a complete shut-off of gas imports from Russia to Western Europe, aggravating the existing energy shortage. It also could disrupt shipments of oil, which would have an impact across the globe.

Next is the ongoing tug-of-war for influence and military advantage between China and the US. The most worrisome flashpoint would be over Taiwan given its dominant position in advanced semiconductor manufacturing. An actual invasion is probably still years away, if it ever happens at all.

The third major area of concern is the Middle East and the negotiations with Iran over its nuclear development programme. Two things are clear: Iran is now much closer to having a nuclear bomb, and Israel still will not tolerate such a major change in the region’s balance of power. The risk of war may be low, but developments continue to head in a direction that could someday have catastrophic consequences.

International investors can be forgiven for being somewhat frustrated. Earnings growth in 2021 for developed- and emerging-market equities both exceeded the earnings gain for the US. As a consequence, the relative valuation of international markets versus the US has become only more attractive in the past year.

The trajectory of S&P 500 earnings growth probably will slow in 2022, but a gain in the 8%-to-12% range seems consistent with our macroeconomic call for continued above-average growth and inflation.

In our view, the real anomaly in the financial markets is the ultra-low levels of interest rates in the face of higher inflation and above-average growth in much of the world. This may force central banks to adopt more aggressive interest-rate policies than they and market participants currently envision.

We have pencilled in a rise of 50 to 75 basis points in 10-year US Treasury bond yields for 2022. That gain should not derail the bull market in equities, but it could catalyse a shift away from the most highly valued, interest-rate-sensitive areas of the market into the broader grouping of stocks that have been neglected for the past several years.

Glossary of Financial Terms

Asset Purchase Programme (APP): The ECB’s APP is part of a package of non-standard monetary policy measures that also includes targeted longer-term refinancing operations, and which was initiated in mid-2014 to support the monetary policy transmission mechanism and provide the amount of policy accommodation needed to ensure price stability.

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Commercial paper: Commercial paper is a type of short-term loan that is not backed by collateral and does not tend to pay interest.

Cyclical stocks: Cyclical stocks or sectors are those whose performance is closely tied to the economic environment and business cycle. Managers with a pro-cyclical market view tend to favour stocks that are more sensitive to movements in the broad market and therefore tend to have more volatile performance.

Fiscal cliff: A fiscal cliff refers to the reduction or withdrawal of government spending, an increase in taxation, or both.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Forward price-to-earnings (P/E) ratio: The forward P/E ratio is equal to the market capitalisation of a share or index divided by forecasted earnings over the next 12 months. The higher the P/E ratio, the more the market is willing to pay for each dollar of annual earnings.

Hawk: Hawk refers to a central-bank policy advisor who has a negative view of inflation and its economic impact, and thus tends to favour higher interest rates.

Inflation-Protected Securities: Inflation-protected securities are typically indexed to an inflationary gauge to protect investors from the decline in the purchasing power of their money. The principal value of an inflation-protected security typically rises as inflation rises, while the interest payment varies with the adjusted principal value of the bond. The principal amount is typically protected so that investors do not risk receiving less than the originally invested principal.

International Monetary Fund: The International Monetary Fund (IMF) is an international organisation of 189 member countries that promotes global economic growth and financial stability, encourages international trade, and reduces poverty.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Mortgage-Backed Securities: Mortgage-backed securities (MBS) are pools of mortgage loans packaged together and sold to the public. They are usually structured in tranches that vary by risk and expected return.

OPEC+: OPEC+ combines OPEC—a permanent intergovernmental organisation of 13 oil-exporting developing nations that coordinates and unifies the petroleum policies of its member countries—with Russia, a major oil exporter, to make collective high-level decisions about oil production levels.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset-purchase programme of private and public sector securities established by the European Central Bank to counter the risks to monetary-policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Price-to-earnings (PE) ratio: The PE ratio is equal to the market capitalisation of a share or index divided by trailing (over the prior 12 months) or forward (forecasted over the next 12 months) earnings. The higher the PE ratio, the more the market is willing to pay for each dollar of annual earnings.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Sovereign: A sovereign refers to government-issued debt.

Summary of Economic Projections: The Fed’s Summary of Economic Projections (SEP) is based on economic projections collected from each member of the Fed Board of Governors and each Fed Bank president on a quarterly basis.

Taper tantrum: Taper tantrum describes the 2013 surge in US Treasury yields resulting from the US Federal Reserve’s announcement of future tapering of its policy of quantitative easing.

Transitory inflation: Transitory inflation refers to a temporary increase in the rate of inflation.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Index Descriptions

The Bloomberg Commodity Index is composed of futures contracts and reflects the returns on a fully collateralised investment in the Index. This combines the returns of the Index with the returns on cash collateral invested in 13-week (3-month) US Treasury bills.

The S&P 500 Index is a market-capitalisation-weighted index that consists of 500 publicly-traded large US companies that are considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any

action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.