Monthly Market Commentary: Early February Freefall Erodes January’s Jump

Economic Backdrop

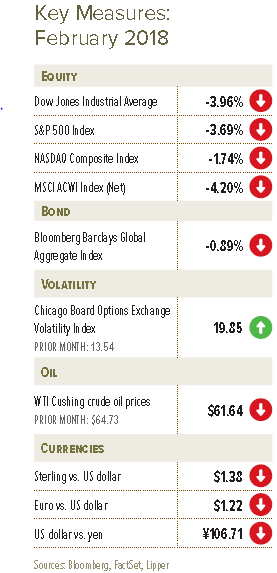

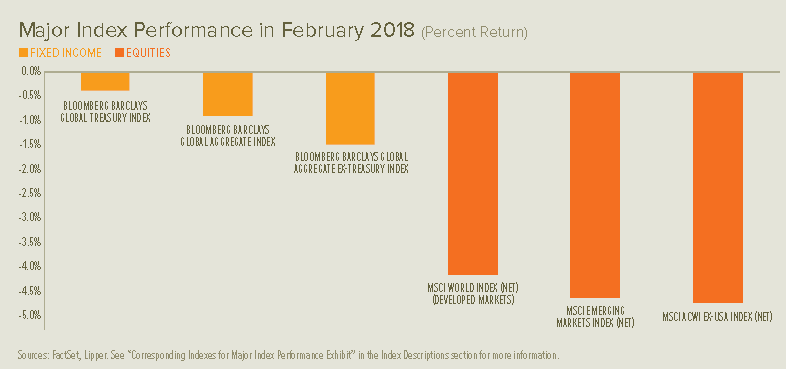

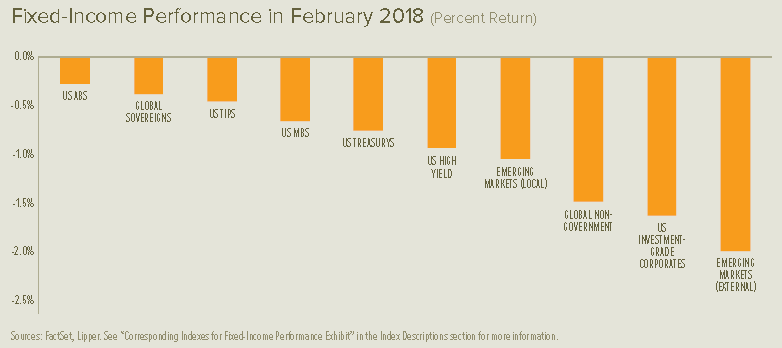

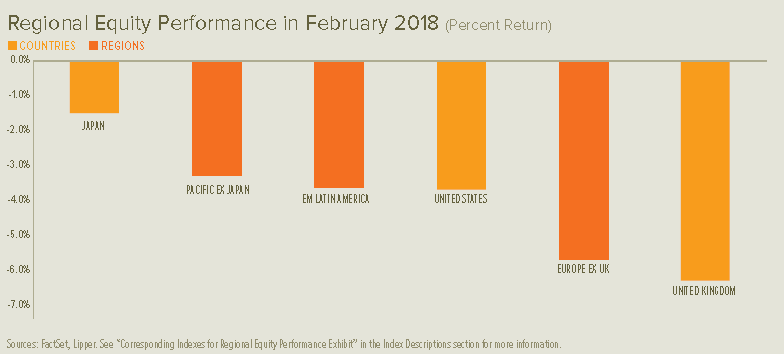

February began with all the ingredients for investor disappointment. Stocks plummeted globally right out of the gate as influential long-term US Treasury rates continued a steep climb, presumably in response to signs of rising inflation and expectations for a strengthening of the US Federal Reserve’s (Fed) counteractions. Investor concerns lingered longer than the actual selloff, however, which concluded within the first two weeks of the month. Yet February ended with a return to selloff mode, as all stock markets finished the month negative despite partial recoveries of varying sizes across regions; many, however, retained positive year-to-date performance thanks to sharp gains achieved in January.

The Irish border resurfaced as a dividing line between UK and EU negotiators following the circulation of a draft EU Brexit agreement, while the post-divorce trade relationship remained a key point of disagreement. The draft, which Prime Minister Theresa May rejected, sought to retain Northern Ireland within the EU customs union and, therefore, erect a trade barrier with the rest of the UK. It also aimed to prohibit the UK from striking third-party trade deals during the post-Brexit transition period. Prime Minister May offered indefinite leave as a concession for rejecting full rights for EU citizens who enter the UK after Brexit takes effect next March. She faced competing pressures at home; businesses and soft-Brexit proponents widely supported the Labour party’s plan to establish a UK-EU customs union, while hard-Brexit proponents sought no commitments to the EU following the divorce.

Italians prepared for a trip to the polls at the beginning of March with about 40% of voters undecided; early results showed a rebuke of the centre in favour of populist eurosceptic parties. Greece returned to international borrowing markets in early February for the first time since 2014, successfully raising €3 billion.

An early February US budget agreement ended the second government shutdown of 2018—this time lasting just overnight—providing new fiscal stimulus via $300 billion in spending increases over the deal’s two-year scope. President Donald Trump expressed intentions to apply tariffs to steel and aluminium imports as the month concluded, rattling equity markets as well as his fellow Republicans and many in his own cabinet—particularly as this followed a January announcement by his administration about tariffs on solar panels and washing machines; Canadian lumber tariffs that were applied late last year have already contributed to supply shortages, rising costs and upward pressure on new-home prices in the US.

The Communist Party of China proposed a change to the country’s constitution (widely expected to be adopted at the National People’s Congress in March) that would remove presidential term limits and provide President Xi Jinping with an open-ended tenure as China’s leader. Plans were also announced in February for the establishment of a domestic Chinese market for yuan-denominated oil futures that will be open to foreign investors.

The Bank of England (BOE) was the only major central bank to hold a monetary policy meeting during February. Its Monetary Policy Committee voted unanimously to refrain from making changes, yet its Quarterly Inflation Report depicted modest improvement in the economic outlook. New Fed Chair Jerome Powell, who took office in early February, offered a favourable economic outlook in his semi-annual testimony on monetary policy to Congress at the end of the month. His comments implied that the Fed may need to act more aggressively (that is, hiking rates faster than anticipated) to address the strengthening economy; financial markets responded to Powell’s comments with increased volatility.

UK manufacturing conditions remained firmly in growth mode, essentially in line with January’s pace of expansion, while activity in the services sector accelerated to healthier levels. Claimant count joblessness declined in January; the unemployment rate for the October-to-December period edged upward to 4.4%, while average year-over-year earnings growth for the 12-month period ending December was unchanged from the prior month’s year-over-year rate of 2.5%. The latest reading of overall economic growth for the fourth quarter was revised downward to 0.4% (and 1.4% year over year).

Manufacturing and services growth in the eurozone continued to expand at an impressive pace despite slowing somewhat in February; moderation was sharper in the services sector. The unemployment rate was 8.6% in January, matching December’s downward-revised report, although youth unemployment improved from 17.9% to 17.7%. The second reading of fourth-quarter economic growth remained 0.6% (and 2.7% year over year).

US manufacturing reports variously depicted a firm-to-sharp expansion in February, while growth in the services sector picked up convincingly. The unemployment rate held firm in January at 4.1%; average hourly earnings growth accelerated to a 2.9% year-over-year pace, the highest since the global financial crisis, from an upward revised 2.7%. Weekly jobless claims fell to the lowest level in 49 years during the second half of February. Economic growth for the fourth quarter was revised downward to a 2.5% annualised rate.

Our View

The global financial crisis finally appears to be in the rear-view mirror. In its place is synchronised expansion across most developed and emerging economies. Admittedly, developed economies continued to run at a rather sluggish pace of approximately 2% to 2.5% gross domestic product (GDP) growth (as of the latest available figures for the fourth quarter). This is, at best, a middling sort of performance in the context of the past five decades. Emerging-market economies, meanwhile, continued to expand at a clip well below that of the past 20 years.

Over the next year or so, we think global growth can still be vibrant enough to allow risk assets to perform well.

US tax legislation is hardly perfect: we do not expect it to be as stimulative as advertised since tax cuts are skewed toward upper-income tax payers who tend to have a higher saving rate than the median household. But the permanent corporate tax changes, repatriation holiday, and the full expensing of capital equipment purchases over the next five years are positive developments for economic growth and investment.

Security analysts, always an optimistic lot, are calling for an 11% rise in S&P 500 Index per-share operating earnings in 2018. Although earnings estimates tend to fade through the year as estimates adjust to reality, this time may be an exception because tax cuts have not yet been taken fully into account.

The major worry for investors comes down to the stock market’s valuation. A little more than three-fifths of the S&P 500 Index’s price gain in 2017 came from improving earnings, while the rest was due to a rise in the price-to-earnings (P/E) ratio. But elevated valuations can be justified by the low level of bond yields and the strong trend in profits growth. Of course the higher the valuation, the more vulnerable the stock market becomes to unexpected bad news.

We won’t be really concerned, though, unless we see a more aggressive swing in Fed policy toward monetary tightness—something we don’t anticipate in the coming year. It’s possible that the US will see inflation pressures finally begin to build as 2018 progresses, but US companies have proven able to maintain profit margins without resorting to price increases.

In our opinion, Europe has more growth potential than the US. According to the World Economic Forum’s annual report on global competitiveness, the high-income countries of Western Europe have made important strides in improving labour-market efficiency over the last five years. We also would note that political concerns in the eurozone are far more muted compared with a year ago, although we have not yet seen the end of the heavy anti-establishment undercurrent.

Given our view that the region is a long way from employment levels that will stir inflation pressures, we expect monetary policy to be supportive of growth throughout the coming year—even as the European Central Bank proceeds with tapering its quantitative-easing programme. Since these asset purchases will continue at least until the end of September, it appears that policy rates will stay put until 2019.

We therefore believe the path is clear for further economic growth in the year ahead. The strong 2017 revival in corporate revenues and earnings should continue; the MSCI European Economic and Monetary Union Index (Total Return) forward P/E ratio was no higher as of December 31, 2017, than it was a year earlier. Solid economic growth and cheap equity valuations are usually a good combination for investors.

These have not been easy days for UK Prime Minister Theresa May. The divorce stage of Brexit talks appeared to have concluded late last year, with the UK mostly acceding to the EU’s demands, but even this stage appears vulnerable to renegotiation (as evidenced by the latest disagreement over the draft EU Brexit proposal). Parliament has also begun to flex its muscles—and disapproval there would force the parties back to the negotiating table. Keep in mind that any changes to the withdrawal agreement demanded by Parliament would require unanimous approval of the 27 members of the EU on the other side of the negotiating table.

The BOE’s Monetary Policy Committee forecasted only two rate increases between now and the end of 2019. While time will tell whether the central bank’s view regarding future policy moves are accurate, policymakers in the UK face tremendous challenges over the next few years. We think investors should tread lightly until there are clearer signs that inflation pressures have peaked and Brexit negotiations actually yield a favourable economic outcome for the country.

Japan is clearly benefiting from the global economic recovery. Exports to China are growing particularly quickly, and are now about equal to the share going to the US. Exports to the US and Europe also have accelerated, but not to the same extent.

Although there have been rumblings that the Bank of Japan would like to take a step away from the extraordinary monetary policies that have been in place since the financial crisis, the central bank may find it difficult to do so. Domestic demand remains weak and the population has begun contracting, a trend that will likely accelerate.

Japanese equities did well last year, with the TOPIX rising by 26.55%. Remarkably, the forward P/E ratio declined over the course of 2017 despite the improvement in economic fundamentals. It remains one of the more cheaply-valued stock markets among developed countries. Forward- earnings estimates have climbed sharply in the past year; we note that revenue estimates are also inflecting higher.

Emerging-market equities climbed significantly last year, with a particularly strong contribution from China. Despite some backsliding last year, China has continued to reduce its dependence on heavy industry and increase the value added to GDP from service-producing industries. While these macro statistics need to be taken with a grain of salt, it appears that China’s growth has accelerated significantly from two years ago and is advancing at its fastest clip since the 2012 to 2013 period. If China can maintain positive momentum, commodity prices should continue to rally as well.

We have held a positive view of risk assets for most of this long bull market. When speaking to investors who are nervous about the stock market’s valuation, we urge them to keep a longer-term focus. Timing the market in anticipation of a short-term correction should be discouraged. As we’ve seen in the past year, making a major de-risking move could result in a significant opportunity-loss when there are few, if any, signs of major economic imbalances or frothy valuations. Until we see a more significant deterioration in the economic and financial fundamentals that have underpinned the global bull market in risk assets over the past two years, our default investment stance is to stay the course.

There are many possible events and developments that could have a big negative impact, but most have a low probability of actually happening. We will therefore maintain our “risk-on” bias until we see evidence that such a stance merits revision.

Glossary of Financial Terms

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to do so) and investor confidence is high.

Forward price-to-earnings ratio: The price-to-earnings ratio is equal to market capitalization divided by after-tax earnings. The higher the price-to-earnings ratio, the more the market is willing to pay for each dollar of annual earnings. The forward price-to-earnings ratio relies on future earnings estimates.

Fundamentals: Fundamentals refers to data that can be used to assess a country or company’s financial health, such as amount of debt, level of profitability, cash-flow or inventory size.

Macroeconomic: Macroeconomic refers to the broad economy of a country or region, or the global economy.

Quantitative easing/tightening: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy; quantitative tightening refers to efforts by central banks to help decrease the supply of money in the economy.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.