Monthly Market Commentary: Bargaining Breakthroughs in November?

Economic Backdrop

The financial-settlement leg of Brexit negotiations appears to have hit a magic number that both sides can digest despite its unpopularity in the UK—likely at least €50 billion in total payments from the UK to the European Union (EU) over the course of many years, which is roughly equivalent to the UK’s projected net EU contributions from 2017 to 2021. Two other aspects of the divorce—citizens’ rights and the possible reimposition of a hard Irish border—remained a source of grave contention among negotiators, which could preclude discussions from advancing to issues concerning future commercial relations. Elsewhere, German Chancellor Angela Merkel struggled to find a governing-coalition partner and considered calling new elections in the absence of progress. Nearly two dozen EU member states signed a mutual-defence pact made possible by Brexit’s removal of the UK as a roadblock to European military integration.

US congressional work on tax reform progressed throughout November, with passage appearing probable but contentious due to a thin Republican majority. The likelihood of a December government shutdown increased as a stopgap spending agreement wound down with little apparent appetite for the bipartisan compromises necessary to strike another budget deal. Canadian lumber exports to the US were subjected to tariffs amid renegotiation of the North American Free Trade Agreement, while Asia-Pacific nations reasserted their commitment to an updated Trans-Pacific Partnership trade deal—this time without the US—at a regional summit during the month.

The Bank of England’s (BOE) Monetary Policy Committee increased its benchmark rate for the first time in a decade in early November, and issued a quarterly report signaling expectations for above-target inflation to remain through 2020. BOE stress-test results indicated that major UK banks could be expected to continue operations, even amid disorderly Brexit proceedings. The US Federal Reserve (Fed) said it in its 1 November announcement that it made no changes to monetary policy, but Fed Chair nominee Jerome Powell expressed confidence during his confirmation hearing that conditions appeared to warrant a benchmark rate hike in December. The European Central Bank and Bank of Japan did not convene for monetary policy meetings during November.

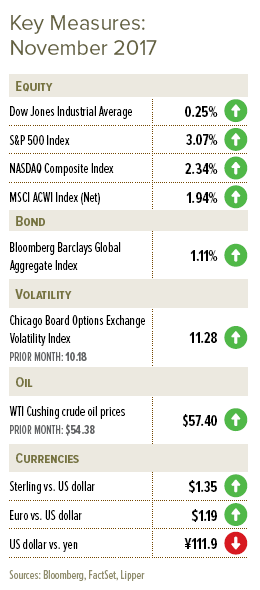

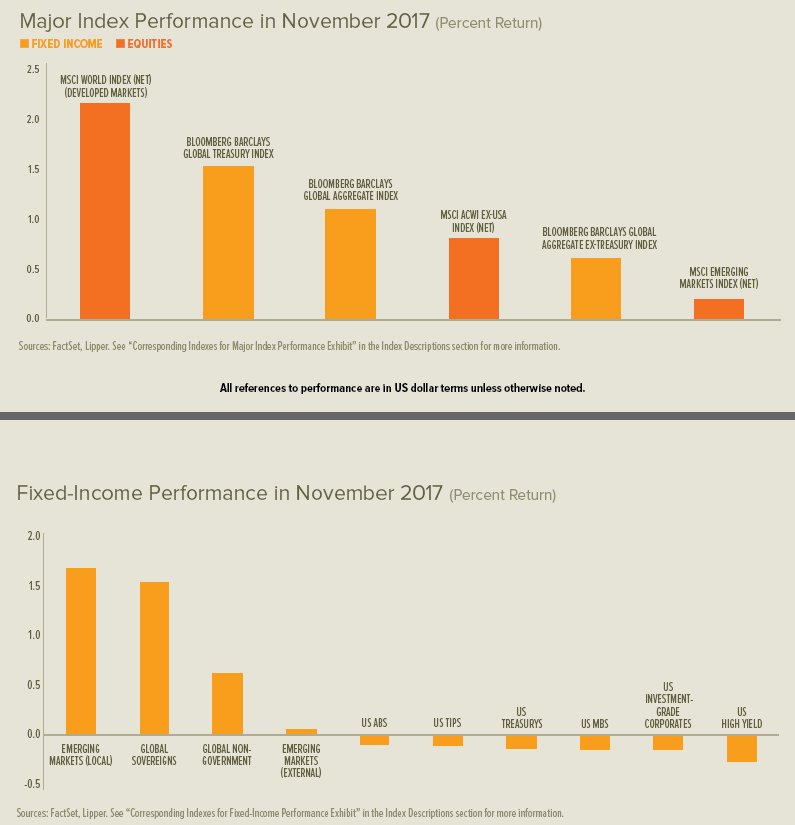

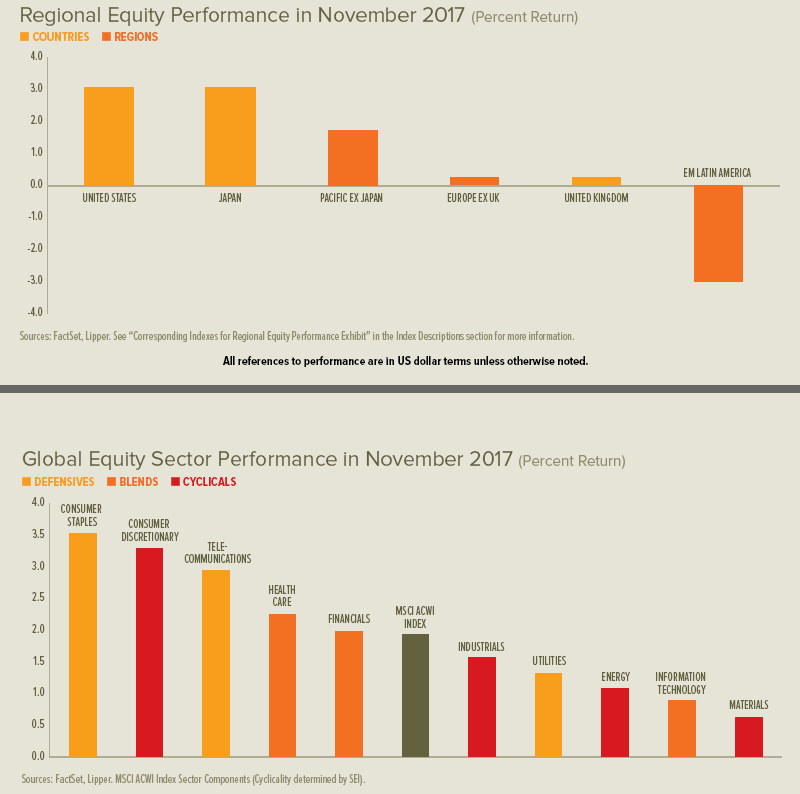

UK and European stocks declined in the first half of November but recovered by the end of the month, while US equities were flat for much of the month before advancing in the final week as tax reform came into focus; the rally started earlier and was more pronounced in small-company stocks given their sensitivity to US tax rates. Japanese and Hong Kong equities advanced during the month, while mainland Chinese stocks rallied in the first half of the period before dropping and finishing lower overall. Brazil had a negative month; volatility generally increased in emerging markets as November came to a close. Sterling, the euro and the Japanese yen all strengthened against the US dollar; sovereign yield curves flattened in the UK, eurozone and US as short-term rates generally increased and long-term rates declined. West Texas Intermediate crude-oil prices advanced in anticipation of a late-November agreement by the Organization of Petroleum Exporting Countries and non-member states to extend production cuts through 2018.

Expectations for UK retail sales in November looked strong after a betterthan-expected rebound in October. Manufacturing growth accelerated during November to its best overall showing in more than four years. October unemployment and earnings growth were unchanged for the second straight month. The country’s overall economic growth was unrevised at 0.4% for the third quarter and 1.5% year over year ending 30 September.

Eurozone manufacturing activity continued to accelerate in November, pushing output to its greatest level in almost seven years; new orders to 17-year highs; and exports, backlogs and headcount to record-breaking growth. Services sector growth also quickened. Economic sentiment extended an uninterrupted six-month advance, with improvement in both the industrial and consumer components.The latest reading of broad economic growth held at 0.6% for the third quarter and 2.5% for the one-year period ending 30 September.

US consumer confidence pushed to a 17-year high in November, as labour-market perceptions turned more optimistic in terms of the current environment as well as expectations. Personal incomes remained healthy in October, while consumer spending growth settled to more-normal levels. Core personal consumption expenditure prices—the Fed’s preferred inflation gauge—edged closer to reaching the central bank’s target range. Total economic growth was measured at a 3.3% annual rate, an improvement on already-strong preliminary readings.

Our View

Political dysfunction—up to and including the ongoing game of nuclear chess between US President Donald Trump and North Korea’s Kim Jongun— has done little to halt the ascension of the US equity market. To be sure, all good things eventually come to an end. Yet when we consider valuations, the upward momentum of the US economy and earnings, and the likely path of US Fed policy and inflation, we reason that the US equity bull market is not yet dead.

On the issue of valuations, there is no denying that US equities are trading at elevated levels. But the exceedingly low level of prevailing interest rates is an important mitigating factor. There has been a strong inverse relationship between bond yields and valuations over the past four decades, which we believe justifies structurally elevated valuations.

US equities also appear relatively expensive when comparing their valuations against those of other countries. Indeed, many other countries are on the cheap side—not only against the US, but also against their own histories. This is one reason we currently favour international equity markets versus US equities.

High valuations imply the US equity market could be a performance laggard in the years ahead relative to other stock markets; but they cannot predict an imminent downturn. We believe that valuations are a lousy timing tool for the simple reason that expensive markets can get more expensive.

The overriding question among investors is a simple one: is a recession on the horizon? We contend that the answer is “no.” Financial stress, a harbinger of recession, is virtually non-existent. Recent economic data also point to the continuation of slow-but-steady economic growth.

A large portion of the world appears to be growing at a slightly better-thantrend pace. The breadth of the improvement is particularly impressive; as at September 2017, 68% of the countries that make up the Organisation for Economic Cooperation and Development’s (OECD) Composite Leading Indicator index have posted improvement over the past year—and 66% of the countries in the index came in above 100. This suggests above-trend growth could continue in the months ahead on a global basis.

According to the OECD’s calculations, Brazil’s economic situation is improving at the fastest rate. The eurozone as a whole looks set to grow above trend. China’s momentum remains toward the upside even though recent economic data suggest some deceleration. The US economy, by contrast, is growing somewhat below trend, while India is signalling a rebound toward trend-line growth. On balance, things are looking up in much of the world.

Economic growth of developed economies around the world is converging with that of the US. Although US monetary policy is further along the path toward tightening, other central banks have already begun to raise policy rates (the UK and Canada).

Market participants have adopted a far more sanguine view regarding the political stability of the eurozone following a series of national elections this year that enhanced the position of parties favouring further European integration. While confidence in the eurozone has increased, international confidence in the US has ebbed. The Trump administration’s decision to pull out of the Trans-Pacific Partnership and Paris climate accord was controversial in the US; it was especially confounding to those outside the US, and raised questions of whether it is relinquishing its role as leader of the free world. Confidence in the existing international economic order was also hurt by the threat of additional US trade discord with Canada, Mexico, South Korea and China. Trump was voted into office partially owing to his populist stance on trade; but we think a trade war could be as dangerous an economic blunder today as it was during the Great Depression.

We continue to expect a US business-friendly tax package to be enacted and signed by the Trump administration before the end of the year. However, the failure of such legislation could further dampen investors’ expectations for US economic growth—thereby causing a serious correction in the overall US equity market, especially hurting economically sensitive small-company and value stocks.

As noted above, the upturn in global economic activity is spurring the world’s major central banks to reassess their respective policy stances. The danger is in potentially making policy mistakes, either by acting too quickly or not fast enough. The BOE faces the greatest policy challenge, with an accelerating inflation rate at a time when its overall economic growth has been somewhat below that of the US and eurozone. Although the BOE has begun to raise rates, it is unclear whether the correct policy course calls for further tightening moves.

In the run-up to the National Congress of the Communist Party of China, the country’s economic policy has been geared toward growth. President Xi Jinping’s government has been focused on restraining rampant speculation in the property markets and curtailing growth of the shadow-banking system—with mixed success. As soon as China’s economy begins to weaken and financial markets exhibit signs of stress, its economic planners tend to reengage the accelerator.

It may be time to step on the brake again following the National Congress and the strengthening of President Xi’s political power coming out of that meeting. The inflation rate for manufacturing producer prices at the end of October was near peak levels recorded in 2004, 2008 and 2011. A cyclical slowdown in China’s economy would likely be bad news for commodity prices and other emerging economies. Since the overall consumer price index remained at less than a 2% rate through October, we expect the People’s Bank of China to try a gentle tap on the brake.

While we would not rule out a correction in asset values more notable than others that occurred in the past 19 months, our investment mantra of buying on the dip still holds.

Our equity strategies remain positioned for further cyclical improvement around the world. They generally have a smaller-company and value bias versus their benchmarks. We tend to favour momentum-oriented opportunities, and view equity markets outside the US as more attractive than US equity markets. Indeed, our caution toward equities is most pronounced in the US, where the outlook for earnings growth is more modest than elsewhere in the world.

On the fixed-income side, we expect yields will slowly move higher (yields move inversely to prices) as global growth becomes more entrenched and central banks begin to remove the extraordinary stimulative measures of quantitative easing and zero (or negative) interest rates. Our underlying managers are generally short duration versus their benchmarks, favour credit-spread strategies and are positioned for a further narrowing of the yield curve, especially in the US.

Glossary of Financial Terms

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to do so) and investor confidence is high.

Credit spread: Credit spread is the additional yield, usually expressed in basis points (one basis point is 0.01%), that an index or security offers relative to a comparable duration index or security (the latter is often perceived as “risk-free” credit, such as sovereign government debt).

Cyclical: Cyclical sectors or stocks are those whose performance is closely tied to the economic environment and business cycle. Managers with a pro-cyclical market view tend to favour stocks that are more sensitive to movements in the broad market and therefore tend to have more volatile performance.

Duration: Duration is a measure of risk in bond investing and indicates how price-sensitive a bond is to changes in interest rates. A long (overweight) duration stance indicates the portfolio duration is higher than that of the benchmark whereas a short (underweight) duration stance indicates a lower duration. Duration is measured in years; securities with longer durations are more sensitive to interest-rate changes.

Quantitative easing/tightening: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy; quantitative tightening refers to efforts by central banks to help decrease the supply of money in the economy.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Important Information

Past performance is not an indicator of future performance.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds.This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.