Managed Volatility in a Relative World: Q&A with Portfolio Manager Eugene Barbaneagra

Q. Managed-volatility strategies have struggled for quite some time. What is causing the strategy to now be out of favor?

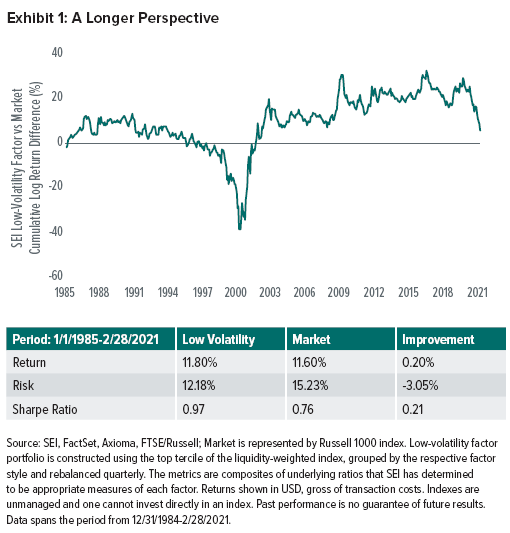

A. Managed volatility failed to deliver much downside mitigation in the first quarter of 2020 and, over the rest of the year, significantly lagged broader equity benchmarks as markets rebounded to new highs. Exhibit 1 shows that, after a long run of positive performance, the lack of risk reduction during the March selloff likely caught most investors in the strategy by surprise.

During previous market drawdowns, equities have reacted in somewhat predictable ways. That is, defensive sectors, such as consumer staples, utilities and telecommunications, have tended to perform better than economically-sensitive sectors like energy, financials or consumer discretionary. Those defensive sectors generally offer lower volatility. At SEI, we seek to optimize our managed-volatility funds and, in an effort to provide the best potential risk-adjusted returns, we tend to overweight defensive sectors. As such, our managed-volatility strategies are designed to outperform the broad market benchmark during market declines (that is, they are designed to experience a relatively less dramatic fall).

This year, we experienced something different from the normal economic cycle. A global pandemic caused by COVID-19 caused countries to shut down their economies in an effort to combat the virus. It became a global economic crisis, the root cause of which was an exogenous shock to capital markets around the world.

How global equity markets reacted was also different; there was less differentiation between sectors than there tends to be in a typical market environment, and smaller companies were hit particularly hard. Because we seek to optimize between returns and risk, we have a greater exposure to smaller companies as well as other factors (such as value, which has underperformed growth in recent years) than our benchmark. In our view, this made for a rare and extremely challenging environment for managed volatility.

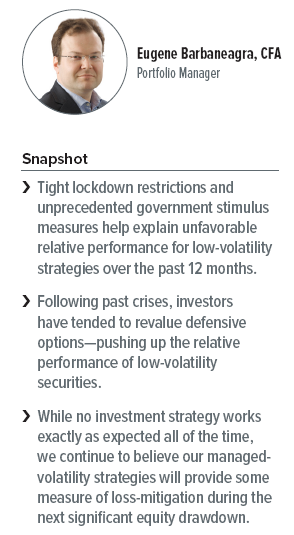

Following the decline in U.S. stock markets through March last year, equities rapidly recovered thanks to substantial fiscal and monetary stimulus—continuously reaching new all-time highs during the second quarter and through the end of 2020. Exhibit 2 shows that the rally was fueled by the strong performance of a small group of mega-cap technology stocks that have had increasing influence over the last few years—and which managed-volatility strategies, by design, tend to underweight. In short, this was the perfect storm for managed volatility to underperform.

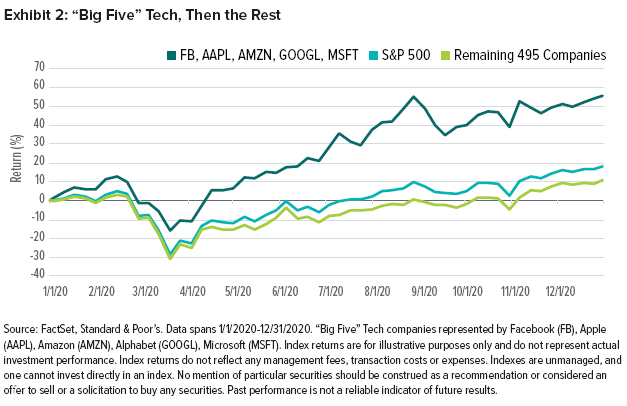

Consider a fund manager who invests entirely in companies with “problematic” outlooks and excessive amounts of debt. Imagine that this manager also has an affinity for businesses that squander capital and whose stocks are more volatile in the face of uncertain economic growth—precisely the companies that managed-volatility strategies tend to avoid. While it may seem ridiculous that anyone would favor such investments, those were the types of stocks that generally outperformed from November 2020 (after Pfizer’s vaccine announcement) through the end of February 2021. We do not see this as a sustainable trend and believe that, over a full market cycle, investors should shun these traditionally “problematic” stocks.

Q. Given our conviction in the strategy, and with value coming back into favor, could you elaborate on how our managed-volatility funds should be well-positioned moving forward?

A. Clearly, the COVID-19 crisis has not been like other crises of the recent past. Over the last 12 months, widespread lockdowns and work-from-home orders increased the role of online technology, which brought growth forward for many of these companies. Unprecedented fiscal and monetary stimulus by global central banks in 2020 likely impacted the traditional risk-return relationship for equities in the short term. However, as investors become increasingly conscious of the long-term uncertainties surrounding the riskiest securities, “boring” firms will (in our view) return to favor. Businesses that are sustainable, secure, and have reasonable fundamental and business models should weather a global recession if one ensues.

The global equity market implications of central banks’ stimulus measures will continue to reveal themselves over the coming years. Following past crises, investors have tended to revalue defensive options—which pushed up the relative performance of low-volatility securities. This was the case after the global financial crisis. We think this rerating of “boring” stocks will happen again in the short future.

Investors often question the value of diversification, particularly managed-volatility strategies, when stock prices are rising. At SEI, we have been a steadfast supporter of both diversification and managed volatility. We have always maintained that markets can turn quickly and that, when they do, diversification— including exposure to managed volatility—can help to soften the impact. If you find yourself questioning the short-term performance of a managed volatility strategy, you may be falling prey to the same behavioral factors that have long caused investors as a group to commit errors such as mispricing risk. When investors use inappropriate metrics in comparing managed volatility to other strategies, or make investment decisions based solely on prior short-term benchmark-relative performance, they are committing common investment mistakes that some institutional investors are even prone to making.

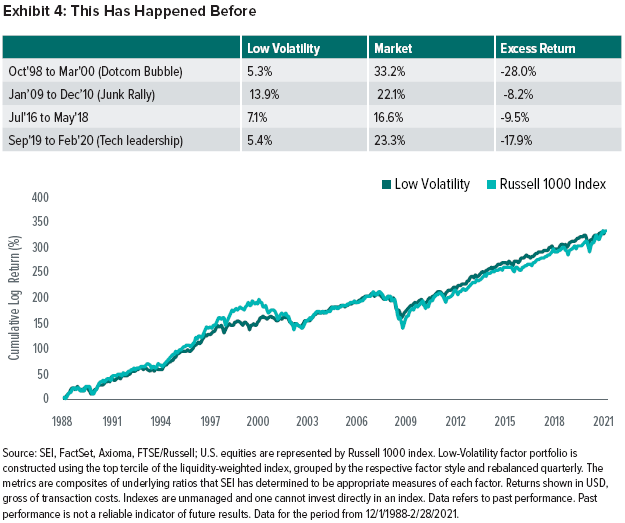

If the next crisis is triggered by an exogenous event, perhaps managed volatility will again fail to live up to expectations that it will mitigate losses. Yet, we have reason to believe otherwise. In some ways, we have been here before. In the run-up to the technology implosion in 2000, markets rallied as increased information technology spending and the novelty of internet stocks drove the market higher. The compelling storyline back then sparked a relative rout in low-volatility stocks. However, investors who stayed the course were rewarded in time as market behavior normalized.

We believe in our research. While no investment strategy works exactly as expected all of the time, our managed-volatility strategy has done so more often than not since inception—and we believe it will continue to provide some measure of loss mitigation during future significant equity drawdowns. Exhibit 4 shows that following previous crises, investors in U.S. equities have usually revalued defensive options, pushing up the relative performance of low-volatility securities. Periods of significant underperformance have happened before; however, over the long term, the strategy has delivered on its mandate of market-like returns with less volatility.

Q. You have said in the past that adding strategies based on managed volatility to an investor’s portfolio can add value over a full market cycle. Do current market conditions and performance change that view?

A. Managed-volatility approaches to investing, which are based on a long history of solid empirical evidence, offer investors a unique and compelling way to potentially earn stock-market-like returns with less volatility. SEI was a pioneer in the implementation of managed-volatility investing more than a decade ago, and we have continued to innovate as the investment style has evolved.

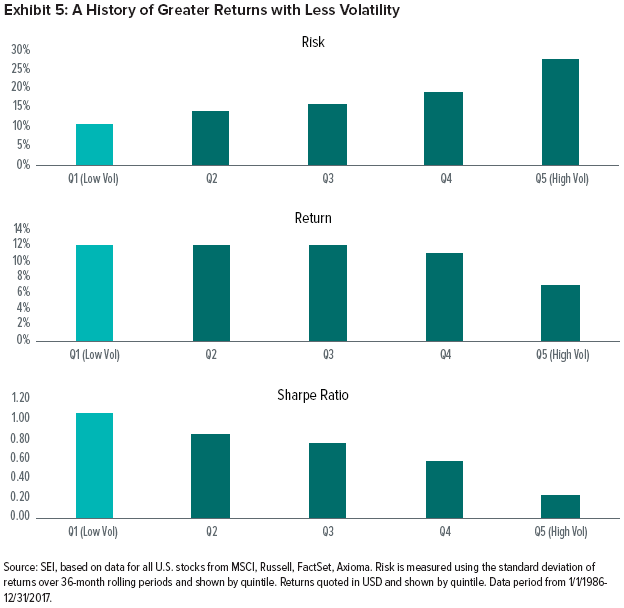

Analysis of real-world market data found that, as a group, investors historically overpay for higher-volatility securities and underpay for lower-volatility ones. Said another way, returns on high-volatility stocks were significantly lower, and returns on low-volatility stocks were higher than prevailing finance theories predicted. This was a significant and unexpected finding—an anomaly in financial parlance, as confirmed by subsequent studies using data from other time periods and other markets. Exhibit 5 shows this rather compelling upshot: An investor could potentially earn better-than-expected returns for a given level of risk.

When equity markets are in the midst of extended bull run, nobody wants to think about it ending. Yet, sooner or later it will end. While corrections and bear markets are a normal part of investing, investors do not like to lose any portion of their assets associated with these types of declines.

One way to potentially help dampen the impact of market downturns is to invest in managed-volatility strategies that focus on the more stable companies that have historically shown less downside risk. In our view, because it’s impossible to predict when such a decline with occur, it is important for investors to have managed-volatility exposure in their portfolios at at all times.

Q. Where does managed volatility fit into a portfolio’s asset allocation?

A. With the potential to deliver equity-like returns with lower expected volatility over the long run, we believe the appeal of managed-volatility exposure within a broader portfolio is apparent. Depending on how the allocation is funded (meaning which combination of traditional stocks and bonds are sold in order to purchase low-volatility equity), it can allow for potentially higher expected returns, lower expected volatility, or both. Naturally, higher risk-adjusted returns afford investors greater confidence in their ability to achieve their financial goals. Particularly at the lower-risk end of the spectrum, where many investors are concerned primarily with the risk of absolute loss, managed volatility can allow for the possibility of significant long-term growth with potentially smaller expected drawdowns.

We believe deviating from familiar capitalization-weighted allocations and including managed-volatility equity exposure has the potential to create more efficient total portfolios that are better equipped to meet the objectives of long-term investors. Given a sufficient time horizon, we believe it’s important for investors to focus on the longer term rather than short-term market fluctuations.

Definitions

Cumulative log return refers to the continuously compounded rate of return on an index or investment.

Factors are the inefficiencies that an active investment manager seeks to exploit in order to add value.

Fiscal stimulus refers to government policy measures—such as tax cuts or government spending—that are taken to improve economic activity.

Monetary stimulus refers to central-bank policy measures—such as lowering interest rates—that make it cheaper to borrow or invest.

Sharpe ratio is a measure of risk-adjusted return for a security, index or investment. A higher Sharpe ratio is considered superior to a lower Sharpe ratio.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.