Making the Case for Managed Volatility Part 2: What Matters?

A combination of strong demand and global supply bottlenecks caused consumer prices to surge by 5.3% over the 12-month period ending July 2021, the fastest year-over-year pace in 13 years.1 Given that the U.S. Federal Reserve (Fed) has historically sought to manage inflation by governing interest rates—typically raising rates to slow the economy when inflation exceeds a target level—the timing of the Fed’s next interest-rate hike has come into sharper focus for many investors.

While the Fed has some ability to influence inflation, it can’t as easily control expectations for future inflation—a market-based measure referred to as the breakeven rate. The breakeven rate represents the difference between the nominal yield on U.S. Treasurys of a given maturity (interest payment before adjusting for inflation) and the yield on an inflation-linked bond (which inherently rises and falls with the rate of inflation) with the same maturity.

If the Fed were to start raising rates, a move it has indicated could come as early as the end of 2022, investors would view the move as a pre-emptive action to halt further inflation. Expectations for future inflation—the breakeven rate—show exactly this.

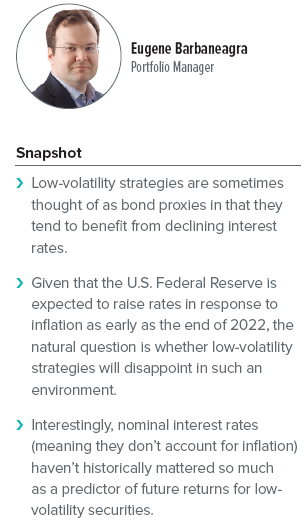

Exhibit 1, which tracks the 5- and 10-year US breakeven inflation rates, illustrates that expectations appear to have already climbed significantly over the past 18 months. At the end of September 2021, the 5-year breakeven rate was at 2.50% and the 10-year breakeven rate sat at 2.37%, indicating expectations that price increases may be somewhat transitory and that inflation could eventually decrease over a more extended period.

Why does this matter to managed-volatility investing?

With the Fed expected to raise rates at some point in response to inflation, investors naturally question whether their strategies will disappoint in a rising-rate environment. This may be particularly true for investors with low-volatility portfolios, which tend to be overweight defensive sectors like utilities and consumer staples. Low-volatility strategies are sometimes even thought of as bond proxies as they tend to benefit from declining interest rates.

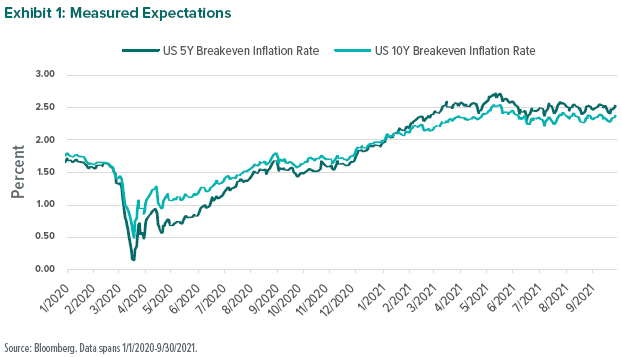

Interestingly, nominal interest rates haven’t historically mattered so much as a predictor of future returns for low-volatility securities. Exhibit 2, which plots changes in the yield on 10-yearTreasury bonds against relative returns for low-volatility securities, shows that nominal yield changes are not closely related to performance.

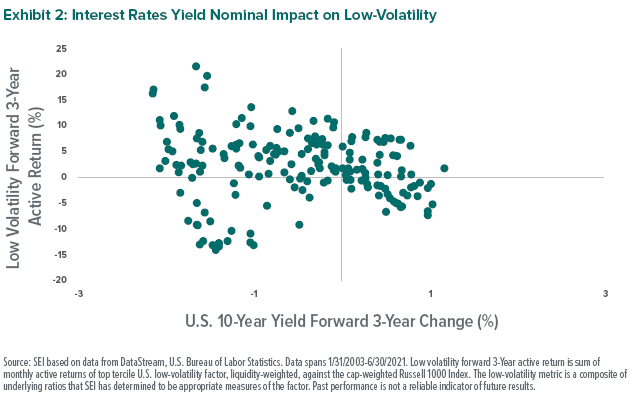

It has actually been changes in inflation expectations—not changes in interest rates—that have typically driven low-volatility performance. History shows that the environment can remain favorable for low-volatility returns when rates rise as long as inflation expectations do not also increase. Exhibit 3 plots changes in the 10-year breakeven rate against relative returns for low-volatility securities. As the chart indicates, declining breakeven rates have historically caused low-volatility returns to improve.

Our view

While a continuation of rising inflation expectations would likely prove challenging for low-volatility investments, we believe the worst has already come, and that expectations forhigher inflation are likely already factored into the market environment. As discussed in Part 1 of our series Making the Case for Managed Volatility, low-volatility securities have been trading at their lowest level since the so-called tech bubble of the 1990s. In our view,

This highlights the important role that low-volatility equites play within an investment portfolio, which is to produce attractive risk-adjusted returns compared to the stock market as a whole. Investors often question the value of diversification when stock prices are rising, particularly within managed-volatility strategies. But markets can turn quickly. And at SEI, we maintain that when they do, diversification—including exposure to managed volatility—can help to soften the impact.

-20-15-10-50510152025-3-113Low Volatility Forward 3-Year Active Return (%)U.S. 10-Year Breakeven Rate Forward 3-Year Change (%)

this should make them well-prepared in the event of a significant stock-market downturn.

Glossary

Bond proxies are investments that are thought to replicate the price stability of bonds.

Composite refers to a combination of several measurements or data types.

Risk-adjusted returns take into account the amount of risk that must be accepted to achieve a given return.

Tech bubble was a period of excessive speculation of internet-related companies in the late 1990s.

Tercile is a number that divides an ordered set of data into three parts, each containing a third of the values.

U.S. Federal Reserve is the central bank and monetary authority of the United States.

Yield refers to interest payments received on a bond.

Index Definitions

Russell 1000 Index measures the performance of the 1000 largest U.S. equity securities based on market cap; it is used to measure the activity of the U.S. large-cap equity market.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. Diversification may not protect against market risk.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.