LSV Asset Management: A Valued Relationship

Three academic researchers developed a value-oriented contrarian investment strategy based on deep-value analysis using a proprietary model to identify out-of-favour securities. The theory was based in solid research but had yet to be used in real-world portfolios. A chance meeting with SEI led to an early investment and a partnership that has lasted about 25 years.

Today, LSV’s employees own a majority of the firm’s equity, with the firm’s partners owning approximately 61% of the firm and SEI holding the remaining 39% (as at 30 September 2019, per SEI). While SEI’s longstanding relationship is that of a venture capital partner, the firm is not involved in LSV’s day-to-day management.

Early Insights into Value

LSV Asset Management (LSV) was established in 1994 by three academics in the field of finance to provide domestic, international and global value-equity investment management services through the application of its proprietary quantitative insights. The investment team developed its financial models through years of research in the areas of value investing and behavioural finance. LSV’s roots in these areas form its core investment philosophy and have driven the evolution of the LSV models over time. Josef Lakonishok, one of LSV’s founding partners, remains an active leader in the firm.

The unique relationship between SEI and LSV actively illustrates how SEI taps undiscovered managers that might not otherwise warrant attention. While traditional screening methods that require minimum assets under management and track records would have eliminated LSV as a potential partner early in the process, SEI took a unique approach to find value within the academic insights.

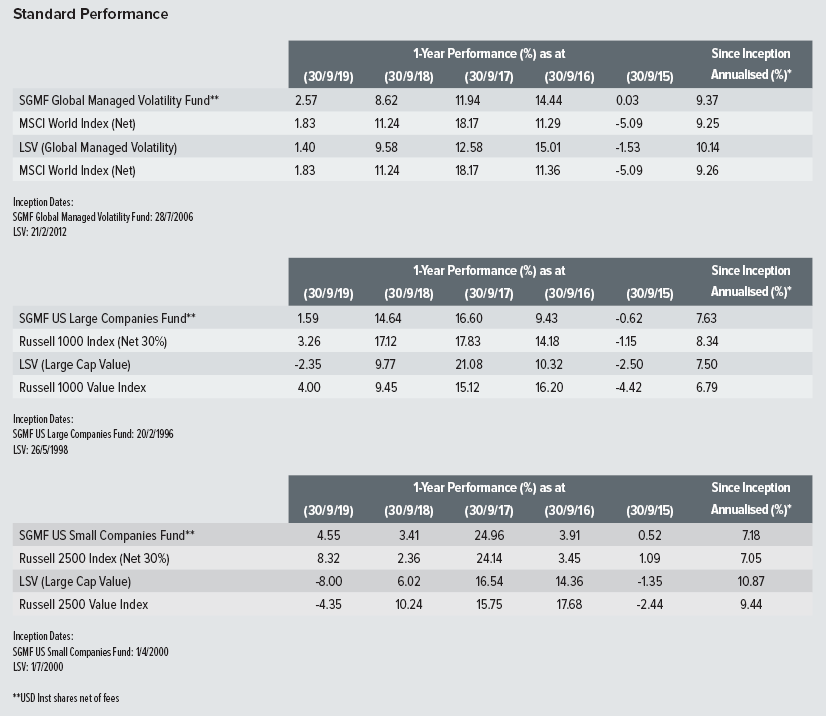

LSV is currently the specialist-advisor to portions of the SGMF Global Managed Volatility Fund, SGMF US Large Companies Fund and SGMF US Small Companies Fund, in addition to several other of our US and Canadian investment portfolios. Approximately 23 percent of the total assets managed by LSV relate to the firm’s sub-advisory relationship with SEI’s Funds (as at 30 September 2019, per LSV).

Solid performance with downside mitigation

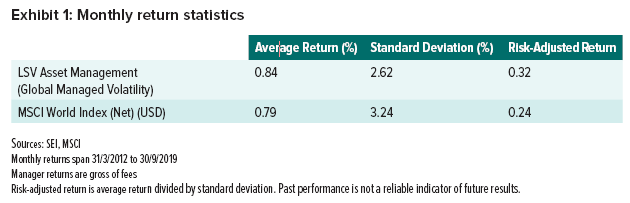

One of the historical benefits of the LSV mandate has been its improvement in risk-adjusted returns relative to its benchmark. There are different ways to calculate riskadjusted return, but the basic idea is to show the return an investor receives per unit of risk assumed. (Risk is typically measured as the standard deviation, or average dispersion, of a portfolio’s returns.) All else equal, a higher risk-adjusted return indicates that a portfolio has potentially struck a better balance between risk and reward. As shown in Exhibit 1, LSV’s mandate within the SGMF Global Managed Volatility Fund has done just that. Since its inclusion in the Fund, LSV’s average monthly return has been 0.84%—slightly higher than the average monthly returns on its benchmark, the MSCI World Index (Net) (USD). Our strategic focus is on the next two columns, however. The standard deviation of those returns was 2.62% for LSV, which is about 19% lower than the standard deviation of its benchmark. This lower volatility also enhanced LSV’s riskadjusted returns. As shown in the last column of Exhibit 1, the return per unit of standard deviation was 0.32 for LSV’s allocation within the SGMF Global Managed Volatility Fund. This is over 30% higher than the 0.24 generated by the benchmark.

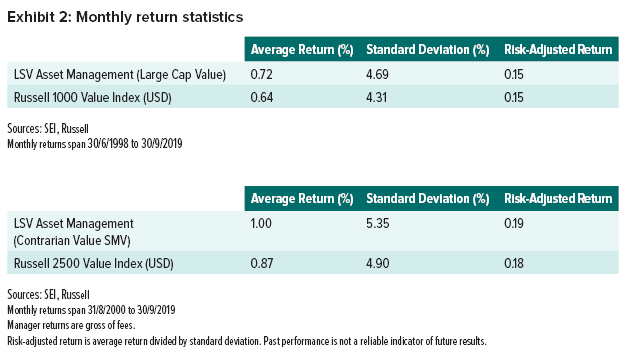

LSV’s Large Cap Value and Contrarian Value SMV mandates have also provided strong long-term performance and marginally improved risk-adjusted returns (Exhibit 2) since LSV’s inclusion within the SGMF US Large Companies Fund and SGMF US Small Companies Fund, respectively.

LSV Asset Management (Information correct as at 30/9/19)

Strategy Description

LSV believes that superior long-term results can be achieved by systematic analysis of the judgmental biases that influence the decisions of many investors. Manifested through its risk-controlled, bottom-up quantitative model, LSV chooses undervalued stocks that have the potential for near–term appreciation in the belief that superior returns will arise when future growth exceeds the market’s low expectations.

Potential Re-Evaluation Triggers

A change in the investment philosophy or a material change in ownership structure.

What We Like

- LSV is a true fundamental investor with deep accounting knowledge; the firm derives insights into investor behaviour through a disciplined quantitative process.

- LSV considers both statistical and fundamental volatility in portfolio construction. In addition, we believe that LSV sufficiently controls two pitfalls of value investing—opportunity cost and value traps.

- Research remains active at the firm, and we find little evidence of any slowdown or passion in its work. Lakonishok is very much involved and closely monitors portfolio holdings.

- There is a willingness to close strategies at reasonable asset levels in order to preserve alpha generation.

Portfolio

GLOBAL MANAGED VOLATILITY

Tracking Error Target: 8-12%

Benchmark: MSCI World Index

Number of Holdings: 150 to 200

Primary Alpha Source: Stability

LARGE CAP VALUE

Tracking Error Target: 2.5-4.5%

Benchmark: Russell 1000 Value Index

Number of Holdings: 100 to 150

Primary Alpha Source: Value

CONTRARIAN SMID CAP VALUE

Tracking Error Target: 3.5-5.5%

Benchmark: Russell 2500 Value Index

Number of Holdings: 125 to 175

Primary Alpha Source: Value

What We Don’t Like

- There is some key-man risk; the firm’s investment excellence is clearly tied to Lakonishok.

- LSV is close to capacity on select strategies.

Important Information

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.