Kevin Barr's Year-End Letter

Dear Client,

The 2020s began with a roller-coaster ride. The global equity market set record highs in February as economic growth gained steam before COVID-19 resulted in an economic shutdown. The forced recession resulted in a typical overreaction, causing shares to plunge. As we learned more about the virus, investors saw opportunities.

Overall, the year was characterised by a polarised equity market. High-flying technology companies shared the spotlight with businesses that benefited from the pandemic. In both cases, a narrow band of extraordinarily high-priced shares led the market higher as reasonably priced, fundamentally sound businesses languished. In this environment, SEI maintained a disciplined approach to investing. Rather than seeking to time the market, we remained focused on quality companies selling at reasonable valuations—a long-term approach that was not the best-performing short–term strategy (as is often the case).

Financial markets adjusted to the pandemic, helped by the fast action of central banks and a big assist from government appropriators. Equities climbed rapidly, and fixed-interest spread sectors recovered almost without interruption from late March through the end of the year, spurred on by reopening economies and positive developments in therapeutics and vaccines.

Economic forecasts were an early casualty of the COVID-19 pandemic, and ours were no exception. Rather than review our expectations from last year as a set of hard predictions like we’ve done in the past, we can use them as a guide to track significant developments in 2020.

- We expected international markets to outperform US shares given the disparity in equity market valuations, but US equities continued to outpace major developed markets. American companies dominated the stay-at-home economy; the slowdown in business activity was comparably shallower in the US than in most other countries and the eventual rebound was stronger.

- On the geopolitical front, we expected rationality to prevail in the pursuit of a Brexit trade deal. It took until the final hours of the year, but a deal was reached. As for US presidential politics, Joe Biden’s candidacy—predicated on a relatively moderate policy platform—helped ensure minimal election-related volatility in financial markets.

- We predicted that China’s economy would stabilise and improve. Our frame of reference a year ago centred on the Phase One trade-war deal with the US and a steady progression of fiscal and monetary stimulus measures. As it turned out, the pivotal factor in China’s world-beating equity market performance was its government’s ability to orchestrate highly effectivelockdowns in the early months of the pandemic.

- The US dollar weakened, as we anticipated, although not before taking a detour in Marchwhen early news of the pandemic drove investors to the perceived safety of US currency. An alphabet soup of Federal Reserve (Fed) liquidity facilities, central bank swap lines, and the multitrillion-dollar CARES Act vastly increased the availability of dollars. This flood of greenbacks pushed the value of the dollar lower versus a trade-weighted basket of foreign currencies as the year progressed.

- Our expectation that value shares would outpace growth shares was dashed for most of 2020. The key requirements for supporting value—modest improvement in global economic growth, and a tendency for inflation and interest rates to move higher—were taken off the table by COVID-19. However, the record disparity in valuations between the most expensive equities and the least expensive only grew wider. We saw an early glimpse of how this valuation spread can act like a coiled spring—ready to snap back on evidence of inflation—when positive news about vaccines bolstered value shares.

- Perhaps our most consequential forecast centred on stretched valuations: “Even at low interest rates, we would consider a forward-earnings multiple on the S&P 500 Index of more than 20 times as a danger sign. Another stellar year for US equities in 2020 would be a source of concern rather than celebration.” While we did not anticipate the path that markets would take, US shares ultimately delivered above-average performance in 2020, and the S&P 500 Index finished 2020 with a 12-month forward P/E ratio of 22.1, according to FactSet. While this ratio appears elevated, averages can be misleading. A few companies with astronomical ratios overshadowed a large number with far lower multiples. In any case, low interest rates supported elevated valuations, but future US equity returns are likely to be muted.

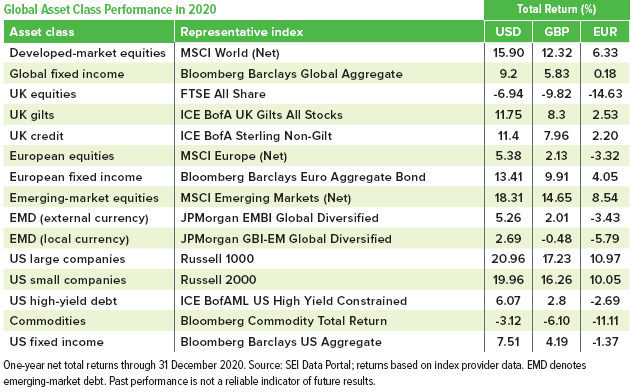

2020 Performance

Globally, emerging-market shares edged out developed markets for the year. China led among major markets, masking weaker performance in other emerging countries, particularly Brazil. The US set the pace for major developed markets, while the UK delivered a loss. We highlight the performance of our equity strategies with this in mind:

- Our active international developed-market equity strategies outperformed their respective benchmarks for the year, improving on the above-long-term average performance of developed markets in 2020. Our emerging-market equity strategies narrowly trailed the benchmark with absolute returns that were higher than the longer-term average emerging-market performance.

- Our core active US equity strategies trailed their benchmarks but produced positive absolute returns in line with longer-term average market performance. A limited group of the largest, most expensive US shares were the top performers. Our large-cap strategies were generally underweight these shares on account of their excessive valuations, which detracted from relative performance.

- Our US small-cap strategies favoured higher-quality, lower-beta equities. These companies have stronger balance sheets, generate cash and pay dividends, but they were outpaced by loss-making companies that now represent more than 35% of the Russell 2000 Index market cap. This is a record market share for capital-burning companies over a historical baseline in the 15%-to-18% range.

- Historical returns show that expensive, larger, and loss-making companies haven’t outperformed over the long term. We believe a normalisation of the economic growth rate in 2021 could serve as a catalyst for the market to revert to the long-term drivers of investment returns: earnings, fundamentals and fair valuations. This would boost the relative performance of the less expensive and higher-quality shares that we’ve over weighted in our active US equity strategies.

- The performance of our factor-driven global equity strategies was restrained primarily by their strategic allocations and tactical over weights to the value factor. At a sector level, this translated into losses from positions in less expensive cyclical sectors that were directly impacted by COVID-19 disruption. As noted with our US equity strategies, we anticipate that normalization of economic growth will accrue to the benefit of our positioning, both strategic and tactical.

- Similar to the themes responsible for underperformance elsewhere, our UK, Europe and Asia-focused strategies lagged their benchmarks during the year. Economic normalization can be expected to favour less expensive, cyclically sensitive sectors, which we believe would benefit the positioning within these strategies.

- Our managed-volatility strategies achieved meaningful volatility reduction versus the broad markets in 2020, but lagged at a distance in terms of total returns. Low volatility was out of favour with investors during the year’s advancing market environment and provided less downside mitigation than expected during the early-year selloff as traditional defensive sectors (utilities, consumer staples) underperformed stay-at-home shares. We don’t foresee a repeat of this outcome because the COVID-19 market crisis was caused by an unpredictable, exogenous development that fell far outside the bounds of how markets usually react to risk-off shocks.

Central bank interventions succeeded in restraining a rapidly developing financial crisis in early 2020. Their actions—ensuring ample liquidity across markets and driving borrowing costs downward—created opportunities in rates markets, fixed-interest spread sectors and inflation-sensitive asset classes. We highlight the performance of our fixed-interest and multi-asset strategies with this in mind:

- Our core fixed-interest strategy improved on the aggregate US fixed-interest market’s already-elevated 2020 returns (relative to the benchmark’s long-term average performance).

- The performance of our multi-asset strategies was challenged by similar dynamics within their equity allocations as those that held back the relative performance of our active US equity strategies. Additionally, their commodities allocations struggled deeply during the early-year selloff, before mounting a strong but partial recovery. We see conditions shaping up for a global reflationary environment in 2021, which we believe would benefit the positioning within our multi-asset equity and commodity allocations.

- Our dynamic asset allocation strategy performed well during 2020, outpacing its US equity market benchmark. Timely rotations into commodities, particularly gold, were responsible for the majority of relative outperformance, but positioning for a steeper yield curve also contributed.

2021: Our View

Since September, shares that had been outpacing the market took a pause, and we saw a rebound by those that had been left behind. Value shares outpaced their growth counterparts to varying degrees across geographies and market capitalisations (most notably within US large caps). While we have observed signs of potential normalization that seem to support the prospects for a style regime change, it is probably too early to tell if this is the beginning of a major secular shift in equity investment themes. Still, we remain confident that the divergence in performance that was a hallmark of the past decade will be reconciled.

Within the geopolitical realm, the last-minute Brexit deal succeeded in removing a measure of uncertainty in financial markets, although challenges remain as the deal addressed the transfer of goods but not commerce in services. Post-Brexit, UK prices will likely end up being a bit higher, gross domestic product a bit lower, and supply chains a bit more unreliable. UK equity valuations, in our opinion, reflect much of the bad news.

Like so many other relationships in the equity market, the underperformance of eurozone equities has been going on for a long time. The European economy is more cyclical, value-oriented and less dynamic than the US economy. But that certainly does not prohibit a rebound in performance against the US equity market at a time when the latter appears to be excessively tilted toward technology shares, the dollar is weakening and a global economic recovery is at hand.

While the pandemic finally forced Germany and other like-minded conservative countries to allow an expansion in fiscal policy, we think that there is greater need for other countries outside the eurozone to regain control of their finances. If those countries fail to do so, Europe could be the beneficiary of investment flows that would further prop up the euro and equity valuations.

Emerging-market equities have been racing higher since they bottomed out last March. However, the MSCI Emerging Markets Index is still just above its previous high-water mark recorded in January 2018. Frontier markets did not fare as well. The MSCI Frontier Emerging Markets Index (total return) has yet to surpass its most recent pre-pandemic high level recorded last January.

Fortunately, the combined efforts of global central banks prevented a liquidity crisis and drove borrowing costs down to near-record lows even as total emerging-market debt exceeded 200% of gross domestic product (GDP). As the world returns to normal, countries may need to raise rates in order to attract sufficient investment inflows to sustain their fiscal and current-account positions.

A weak US dollar is an important catalyst for emerging-market performance. We expect that the coming year will see emerging equities relative performance improve, partly because the dollar should continue to weaken.

Our Focus

No one was expecting last year to turn out the way that it did, but we retain our conviction in SEI’s approach to investment management. We believe diversification is a prudent approach to pursing financial goals in all market environments. Disciplined investing almost never produces the most admired performance in any given year, but we are confident that it will be rewarded in the long term.

We’re all looking forward to a better 2021. Investors appear ready to shrug off the likely prospect of more bad news during the difficult months ahead, which could include slowdowns or pauses in vaccine manufacturing, distribution, administration and uptake. Globally, we expect to see signs of a recovery reveal themselves as COVID-19 abates and economic activity normalises.

In the meantime, fiscal spending and accommodative global central bank policies should sustain GDP growth and eventually cause inflation to rise. As investors price in these developments, “long-duration” assets such as bonds and equities with high valuations should come under pressure. Momentum investors are likely to rotate into new themes, potentially adding fuel to the value rally that has emerged.

As always, we remain committed to our long history of innovation by continuing to explore innovative investment solutions. We thank you for your ongoing support and wish you a prosperous New Year.

Sincerely,

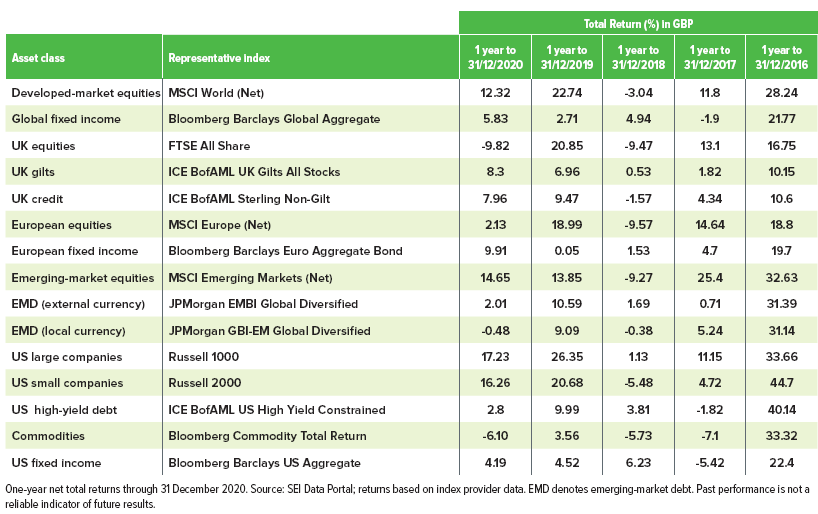

Standardised Performance

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change. All information as of 31 December 2020.

This material may contain “forward-looking information” (“FLI”). FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the “SFO”). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all of the risks applicable to our funds, please refer to the fund’s Prospectus. Please contact you fund adviser (South Africa contact details provided above) for this information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.