Kevin Barr's Year-End Letter

Dear Client:

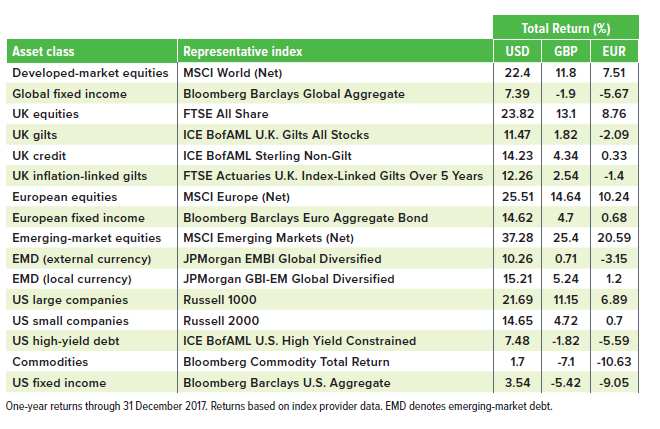

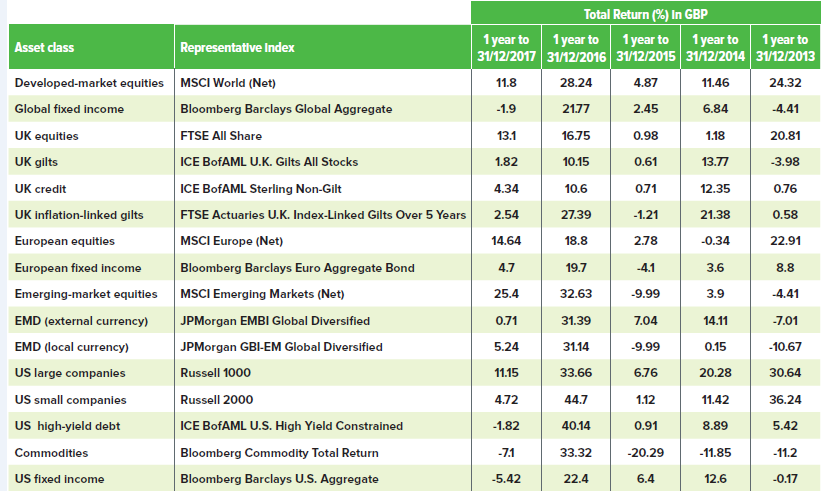

Financial markets completed 2017 without any enduring missteps in an environment defined by strong investor appetite for higher-risk market segments. Not all equity markets followed a steady upward path, but most finished higher than where they began. Fixed-income performance ran the gamut in terms of strength—with emerging-market debt at the top end and US investment-grade at the bottom, in keeping with the risk-on sentiment.

We were surprised by the absence of volatility around the world and across most asset classes in 2017, which was contrary to our expectations for the year.

Our other projections largely came to pass:

› We suggested that market sentiment would remain attuned to geopolitical developments; these accounted for the only significant exceptions to the global tranquillity trend.

› Equities almost uniformly continued to outperform fixed income. Our confidence that economic gains and accommodative policymaking would support earnings growth was rewarded. The energy sector’s return to profitability also helped, thankfully without stoking any sharp inflationary impulses.

› Centrism prevailed in elections for Europe’s most economically significant states, although not across the continent. Brexit negotiations were less important to investors globally than was Europe’s sustained economic expansion; while the euro’s appreciation versus sterling may offer a clue about the market’s perception of post-divorce relative advantages, both currencies gained against the US dollar.

Sterling appreciated by about 9.5% against the US dollar in 2017, driving substantial performance differences between those currencies. The euro’s appreciation versus the US dollar was even sharper, nearly 14%.

Emerging markets outpaced the developed world across asset classes in 2017 amid a synchronised global economic expansion. Equity markets registered gains in most regions, but performance diverged sharply from a sector standpoint. The most risk-oriented segments of the global fixed-income market outperformed traditional safe havens, and US dollar weakness played a decisive role in the leadership of non-US dollar-denominated bonds.

› Asia, particularly China, was the top-performing region for equity markets; Latin America had an astonishing rally during the third quarter before partially retreating into year-end; Europe and Japan were strong performers among developed markets.

› The technology sector led globally; cyclically-oriented sectors like materials, industrials and consumer discretionary also delivered favourable performance. Energy lagged, along with telecommunications.

› Local-currency-denominated emerging-market debt was the top-performing fixed-income segment thanks to a combination of risk appetite and beneficial currency effects. US dollar-denominated debt was challenged by the weak US dollar, especially within low-yielding investment- grade segments.

We highlight the performance of our strategies with these developments in mind:

› Developed-market equity strategies—particularly those focused on Europe, Japan

and the UK—substantially improved upon already-strong benchmark performance. Emerging-market strategies also performed well in benchmark-relative terms.

› On a similar note, our emerging-market debt strategy handily outperformed the leading fixed-income market segment due largely to a preference for local-currency debt, which benefitted from the weak-US dollar trend in 2017, and beneficial positioning.

› Our fixed-income strategies generally outperformed their benchmarks. We correctly positioned for a flatter yield curve, while a preference for credit risk was beneficial as credit spreads continued to decline.

› US equity strategies were mixed; our small-cap strategy outperformed the market while our large-cap strategy lagged. Both gained a material tailwind in the third quarter that rewarded active stock selection. This appears to have been driven by the US Federal Reserve’s commencement of balance-sheet reduction, thereby rolling back a policy that has provided massive market stimulus and supported high stock correlations and low stock dispersion.

2018: Our View

Looking ahead, we think global growth can remain vibrant enough to provide continued support to risk assets. Developed economies continued to run at a rather sluggish pace of 2% to 2.5% gross domestic product growth, and emerging-market economies continued to expand at a clip well below that of the past 20 years.

Until we see a more significant deterioration in the economic and financial fundamentals that have underpinned the global bull market in risk assets over the past two years, however, our default investment stance is to stay the course.

We list below, in terms of decreasing likelihood, the events and developments that would alter our optimistic near-term view:

› An unexpected acceleration in global inflation that forces the US Federal Reserve and other central banks to step up the pace of interest-rate increases beyond those already projected

› A harsher investor reaction to attempts by the US Federal Reserve and European Central Bank to normalise their balance sheets (that is, a 2013-style taper tantrum)

› A melt-up in stock prices that pushes the S&P 500 Index 12-month forward P/E ratio beyond 20 times earnings

› Signs of sharp deterioration in before-tax profit margins as wages and interest rates rise

› A policy mistake in China that causes a credit crunch in its financial system and the property markets, leading to a sharper slowing of economic growth than intended

› A disruption in US trade relations with China or NAFTA partners Canada and Mexico

› A geopolitical event (for example, military action in South Korea, or a spike in oil prices toward $80 to $100 per barrel in the event of war in the Middle East between Saudi Arabia and Iran)

› Evidence revealed by US Special Counsel Robert Mueller that leads to an impeachment attempt of President Donald Trump, especially if Republicans lose their majorities in the House and Senate in November 2018

While these developments would have a big impact, we believe they have a low probability of actually happening. We will therefore maintain our risk-on bias until we see evidence that such a stance merits revision.

Our Focus

Enhancing existing offerings and launching new strategies to meet the ever-changing needs of the marketplace are core tenets of our operations. We will continue to build out additional asset allocation and alternative investment strategies. We will also continue to enhance our manager research capabilities.

As always, we remain committed to our long history of innovation by continuing to explore innovative investment solutions. We thank you for your ongoing support and wish you a prosperous New Year.

Standardised Performance

Important Information

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global, Limited, an affiliate of the distributor. SEI Investments (Europe) Limited utilises the SEI Funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI Funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application must be made solely on the basis of the information contained in the Prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs.) A copy of the Prospectus can be obtained by contacting your SEI Relationship Manager or by using the contact details shown below.

Data refers to past performance. Past performance is not a reliable indicator of future performance. Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Returns may increase or decrease as a result of currency fluctuations. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

In addition to the usual risks associated with investing, the following risks may apply: Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments, securities focusing on a single country, and investments in smaller companies typically exhibit higher volatility.

This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority.

SEI sources data directly from Factset, Lipper, and BlackRock unless otherwise stated.