Jim Smigiel Year-End Letter: UK version

Dear Client,

Global equity markets delivered impressive returns again in 2024, with the U.S. far outpacing other global developed markets thanks to another banner year for the Magnificent 7 mega-cap tech stocks. Fixed-income returns struggled, with rising longer-term yields fostered by stubborn inflation and swelling government debt.

In our letter last January, we expressed our view that investors were overly optimistic on their expectations for equity markets as well as on the view that the annual inflation rate would drop to 2% or less. We were pleasantly surprised by equities and completely unsurprised by the stubborn inflation.

2024 Performance

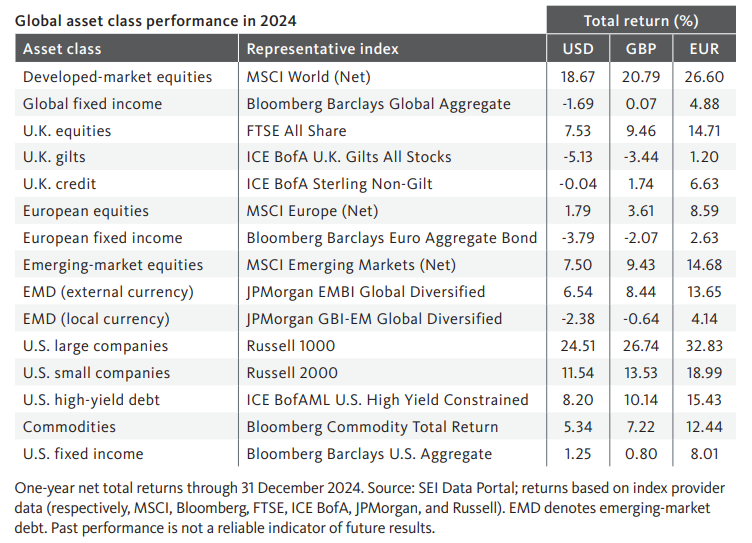

Full-year equity performance was dominated by U.S. large caps—specifically the artificial-intelligence-focused Magnificent 7. Our portfolios were generally underweight these mega-cap stocks on valuation concerns. Smaller companies notably trailed larger ones, but still posted impressive calendar-year gains. Our portfolios generally outperformed in this space due to strong stock selection.

Outside of North America, equities provided solid full-year returns. We had mixed results, with outperformance in developed non-U.S. markets courtesy of overweights to value and momentum, but underperformance in emerging equities due to underweights to China and India.

Core fixed-income portfolios lost ground in the fourth quarter in dramatic fashion as longer-term interest rates rose on speculation that a second Trump term could lead to sustained economic growth and higher inflation. As a result, investment-grade bonds ended the year with only modest gains. High-yield bonds benefited from generally risk-on market sentiment. Short-term portfolios performed well—despite the aforementioned central bank cuts—as interest rates have remained well above the lows of the global financial crisis of the late 2000s.

Our tactical positioning struggled throughout the year before paying off in the fourth quarter. Thematic positions anticipating more persistent inflation and diverging central bank policies significantly outperformed.

Overall, performance was strong in 2024, and the long-term performance of our diversified portfolios remains attractive.

Our view

This year, we find ourselves in a somewhat uncomfortable position of being in consensus with market expectations…at least in part. After two consecutive years of strong equity returns, most market strategists are predicting more of the same in 2025. While we do find ourselves broadly positive on risk assets (both equities and credit), we are keenly aware of the potential challenges.

We believe that the relatively robust state of the global economy, particularly in the U.S., combined with continued monetary stimulus measures from central banks around the world, create favorable conditions for investors. However, we see too many potential outcomes that lead to a reacceleration in inflation and higher long-term interest rates.

Guide for ‘25

The bond market seems to share our concerns, as long-term U.S. yields have risen since the Federal Reserve pivoted to lower interest rates in mid-September 2024. The yield on the 10-year U.S. Treasury is our guide for 2025. We will become concerned about equity markets once the yield reaches 5%, as tighter financial conditions may begin to weigh on economic growth prospects.

Within equities, we continue to expect a broadening of participation in the rally. Not surprisingly, we maintain our strategic recommendations for investors to stay diversified globally and focus on profitable companies with strong earnings momentum trading at reasonable prices.

Within fixed-income markets, tariffs and immigration reforms under the Trump administration may add additional fuel to the inflation fire early in the year. Therefore, given our outlook for higher long-term interest rates, we see headwinds ahead.

Our focus

In the New Year, we will continue to refine our approach to the marketplace to showcase all that SEI has to offer from technology to asset management. We will also continue to enhance our investment offerings, seeking to keep pace with changing preferences. At the same time, we will maintain our focus on providing diversified investments to help investors realize a positive client experience while pursuing their financial goals. Thank you for your continued support and we wish you a happy and prosperous 2025.

Important information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change. All information as of 31 December 2023.

This material may contain “forward-looking information” (“FLI”). FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.