Jim Smigiel Year-End Letter: UK version

Dear Client,

The past 12 months have been a period of significant change both at SEI and in the financial markets. Beginning with events at SEI, Ryan Hicke succeeded Al West as our chief executive officer on 1 June. After successfully leading the firm since founding it more than 50 years ago, Al transitioned to the role of executive chair, where he continues to play an active role in guiding the company’s growth. And on 11 October, we announced the global alignment of our asset management businesses under Wayne Withrow to capitalise on market opportunities and accelerate the company’s next chapter of growth.

While we believe the changes at SEI are positive developments that will help nurture growth for our clients and our company, the financial markets witnessed change in the opposite direction. Following an impressive, although choppy, recovery in 2021 as the worst effects of the COVID-19 pandemic faded, 2022 marked its place in history on a sour note, as inflation, war, supply-chain challenges, and rising interest rates took a toll.

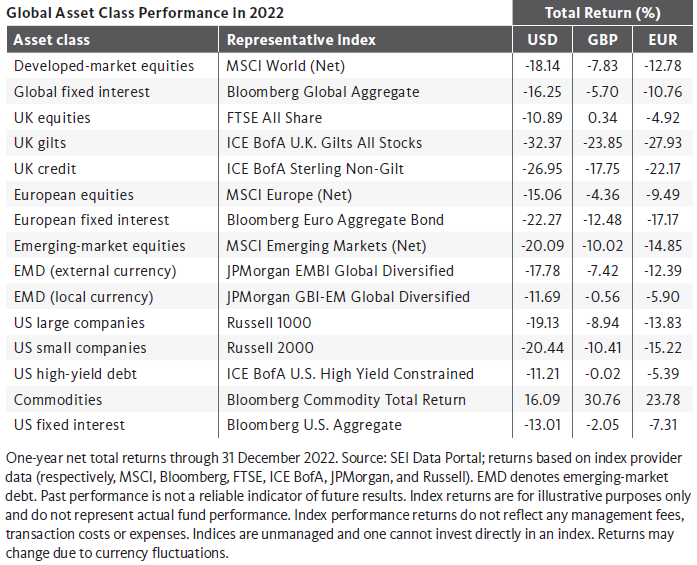

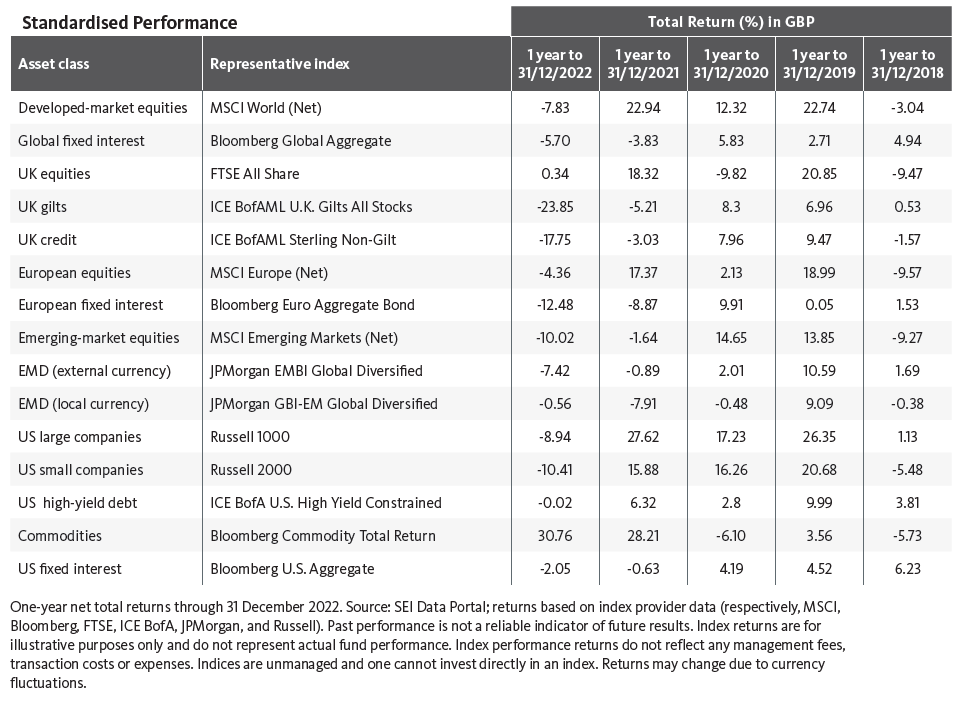

2022 performance

While 2022 was certainly a challenge, SEI’s equity funds had strong relative performance for the year:

- Active and factor-based US equity strategies were helped by a preference for value stocks over growth stocks. This positioning benefited from the risingrate environment because higher rates tend to diminish growth rates and lower the value of future expected cash flows.

- Global managed volatility dramatically outperformed due to its defensive positioning and value tilt—it was easily one of our top-performing funds.

- The performance of non-US-developed strategies was largely in line with the declines seen in the US—with the notable exception of UK equities, which were a standout performer in GBP terms. Meanwhile, emerging markets notably struggled—for much of the year, China’s zero-COVID policy weighed heavily on the region. Emerging markets have felt the global economic slowdown more acutely, while higher interest rates in the US have resulted in foreign capital outflows.

Fixed-income markets suffered through their worst year on record. Rate hikes and inflation reverberated across bond markets—some short-term and inflation-sensitive assets finished in positive territory, but they were the exception rather than the rule. The silver lining is that yields and valuations have not been this attractive since before the global financial crisis of the late 2000s as Bloomberg data shows.

- US and global fixed-income strategies struggled with the rising-rate and inflationary environment. Additionally, the strategies’ preference for nongovernment bond holdings generally detracted from performance.

- Riskier high-yield bonds actually outperformed investment-grade offerings as our high-yield fund modestly underperformed for the year. Their shorter maturities, higher yields, and some exposure to floating-rate securities helped to mitigate some of the effect of rising interest rates.

- Finally, our Dynamic Asset Allocation program finished another strong year thanks to positions in commodities and a strong bias toward higher US longterm interest rates in the first half of the year.

Looking ahead, there are numerous challenges for the global economy. Nonetheless, we believe any recession will likely be fairly shallow. Inflation may continue to run above its long-term trend for some time, but it appears that central banks have at least begun to rein it in. Value-oriented stocks had strong relative performance in 2022, and we believe they remain attractive. As inflation pressures ease and the pace of central bank interest-rate hikes slows, the fixed-income environment should be more compelling.

Our view

We are projecting a less robust global economy in 2023 than the one witnessed in the past year. Volatility is expected across asset classes as investors face familiar headwinds: inflation rates exceeding the targets of major central banks, interest-rate increases continuing throughout the first half of the year, and quantitative easing shifting to quantitative tightening. The expected result for many countries is stagnant or recessionary economies through 2023 and perhaps into 2024. While these obstacles are bad news for stock prices and depress the value of current bond holdings, there is good news for longsuffering income-seeking investors, as fixed-income markets now offer better yields than they have in decades as shown by Bloomberg.

In the US, wages are down in inflation-adjusted terms, the housing market is suffering a severe contraction, and some industries (notably within technology) are losing a significant number of jobs. However, the overall economy still isn’t declining in the pronounced, pervasive, and persistent manner that characterises a typical recession.

With regard to inflation, there is good reason to believe that inflation rates have peaked for most countries. We don’t expect to see inflation fall back to the 2% target that central banks of advanced economies set for themselves. This is especially true in the US and other countries challenged by exceptionally tight labour markets and already-high wage inflation.

Moving on to monetary policy, although Federal Reserve (Fed) Chair Jerome Powell and other members of the Federal Open Market Committee retired the reference to “transitory” when describing inflation, the central bank’s own (and investors’) forecasts still held onto the assumption that inflation pressures would ease substantially in 2022. Consequently, the Fed’s projections of the federal funds rate issued in December 2021 were significantly below the actual rate increases that the central bank implemented over the past year. Further monetary policy tightening is expected in 2023, with a year-end median prediction of 5.1%. Whether this proves sufficient to tame inflation remains to be seen.

The global banking system itself appears to be in decent shape following the regulatory and capital-enhancement reforms put in place after the global financial crisis. On the geopolitical front, energy prices posted surprisingly sharp declines. Natural gas prices in Europe are the exception. With the war in Ukraine appearing likely to drag on for the foreseeable future, the possibility exists for more surprises that will keep energy prices quite volatile, with current prices likely at the low end of a wide trading range.

Looking to China, we’re seeing an easing of the COVID-19 restrictions that have derailed economic growth and snarled global supply chains. We expect China’s economy to reaccelerate in the year ahead from last year’s tepid 3% performance. This should help offset at least partially the impact of a global slowdown in advanced countries. It also could exert upward pressure on commodity prices, especially for energy and metals. This would benefit commodity-oriented exporters in Latin America and the Middle East, along with South Africa, Indonesia, and Malaysia.

Our focus

The financial services industry is changing at an unprecedented rate, and SEI is changing with it. By more closely aligning our asset management business with our go-to-market strategy, we expect to foster the creation of new solutions and increase our speed to market in order to deliver solutions that help our clients solve problems.

In the year ahead, planned expansions to our investment offerings include the launch of additional alternative investment solutions to a broader audience of investors, an expansion of the exchange-traded fund offerings that we successfully launched last year, and the development of a series of costeffective, factor-based portfolios for our clients outside of North America.

I’m excited about 2023 and the opportunities it will bring. I believe we are well positioned to capitalise on growing market trends in the wealth, advisory, intermediary, and institutional markets. I want to thank you for your ongoing support and for your trust and confidence in SEI.

Sincerely,

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change. All information as of 31 December 2021.

This material may contain “forward-looking information” (“FLI”). FLI is disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. FLI is subject to a variety of risks, uncertainties and other factors that could cause actual results to differ materially from expectations as expressed or implied in this material. FLI reflects current expectations with respect to current events and is not a guarantee of future performance. Any FLI that may be included or incorporated by reference in this material is presented solely for the purpose of conveying current anticipated expectations and may not be appropriate for any other purposes.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”) SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.