Inflation Risks Have Started To Come Into Focus

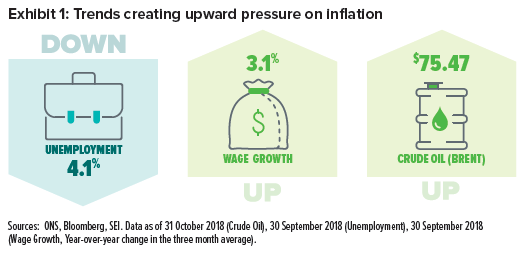

Considering the challenging environment for inflation-related assets in recent years—as evidenced by depressed inflation expectations, negative real yields, and the underperformance of inflation-linked versus nominal bonds—it’s fair for investors to ask “Is inflation dead?”. However, it is interesting to note that inflation risks have started to come into focus in recent quarters, and the outlook for inflation-sensitive assets may be improving. For example, mounting inflation pressures have been reflected in the U.S. consumer price index since the end of 2015 and in the producer-price index since the end of the following year. And while the U.S. labour market has endured a steady but painfully slow recovery since the global financial crisis ended in early 2009, it is now showing signs of substantial tightening; full or near-full employment could eventually put more upward pressure on prices, especially if wage and other employment costs finally start to accelerate. Meanwhile crude oil, as measured by Brent Crude Oil prices, has slumped recently they remain more than double their lows of 2016.

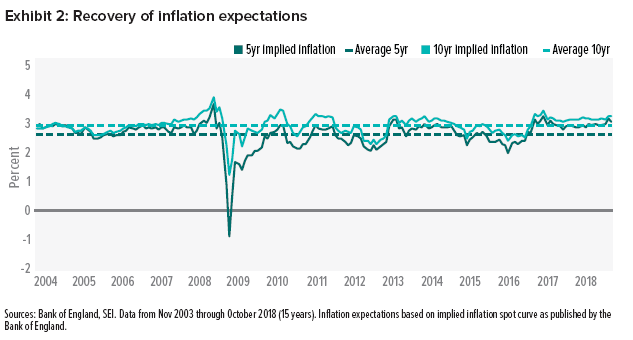

In 2018, after a protracted period of generally lackluster performance of inflation-related assets, investors have been increasingly focused on inflation risks. This can be seen in Exhibit 2, which illustrates that inflation expectations have trended steadily higher since 2016—putting them above their long-term averages.

When it comes to building strategic portfolios, much of the investment industry appears to regard inflation-sensitive assets as a less critical component compared to traditional stocks and bonds. Yet at SEI, we believe that inflation-sensitive assets play a crucial role in strategic portfolio construction. But we do not believe that investors should try to time allocations to inflation-sensitive positions; it is impossible to accurately time major inflation-sensitive asset allocation shifts, just as it is for all other asset classes. While no one can predict shifting market expectations for anything, including inflation, we can try to prepare our portfolios for that eventuality. As such, there are indications that the inflation-sensitive assets in SEI portfolios could come into focus sooner rather than later.

A strategic allocation to inflation-sensitive assets should improve a portfolio’s ability to weather whatever the markets may throw at it. This is not an inflation call or forecast—it is simply a reminder that the future is never certain, that most financial assets are negatively exposed to inflation, and that inflation risk (while missing in action the last several years) should not be presumed dead.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.