How Do You Handle a Bear? Patience and Diversification

Swift selloffs have a way of letting fear obscure reality. The global stock-market plunge that began in mid-February has been primarily defined in broad headline-grabbing terms, tying financial-market conditions to the COVID-19 outbreak—and ignoring underlying details about how different parts of the market have behaved.

We can explore this more nuanced story by looking at sector-level performance of the global stock market. While impossible to conclude with any degree of certainty if or how much further stocks will fall, a sector-specific analysis shows that different segments of the market have been contending with a variety of pressures that extend beyond COVID-19 containment.

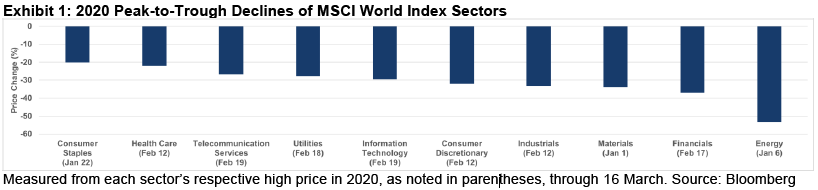

Defensives Have Fallen By Less

Despite the recent all-encompassing declines, traditional defensive sectors (consumer staples, health care, telecommunication services and utilities) held up better, as expected. Exhibit 1 shows each sector’s decline from its 2020 high price through 16 March, as well as the date of its peak.

Notably, information technology has suffered only a middling decline despite being the highest-flying sector in the year-to-date prior to the downturn.

The Rest of the Pack Has Fallen By More

Cyclical sectors (consumer discretionary, materials and industrials) have fallen more sharply than their defensive peers. The materials sector, in particular, has failed to attain a new high in 2020.

Financials—while not a traditional cyclical sector—have performed quite poorly. Higher interest rates are generally considered advantageous for financial companies, which can increase their net-interest margins. Interest rates have been falling around the globe for most of the year-to-date, and plummeted to historic lows as the stock-market selloff accelerated, putting a great deal of pressure on financials.

The Energy Sector

Investor concerns about the growing economic fallout were compounded by the breakdown of OPEC+ (that is, the Organization of the Petroleum Exporting Countries, or OPEC—led by Saudi Arabia—plus Russia) during the first week of March. The expanded cartel, which succeeded in stabilising oil prices after their declines from mid-2014 through early 2016, has essentially dictated conditions on the supply side of the market (along with non-aligned US producers) for the last five years. Apparently, Russia did not acquiesce to Saudi Arabia’s plans for a shared production cut intended to stabilise prices in the face of declining demand, so Saudi Arabia responded by increasing production.

While the move may seem counterintuitive—and resulted in the largest one-day oil-price crash since 1991 (in both West-Texas Intermediate and Brent prices)—the goal appeared centred on driving high-cost producers out of commission. In fact, as a whole, the energy sector never fully recovered from the energy price collapse that began in 2014: the MSCI World energy sector’s all-time high was attained in June 2014, and it has declined by about 70% through 16 March 2020.

SEI’s View

We recognise the fear-inducing impact that steep, sustained stock-market selloffs can have on investor temperament. A deeper look at conditions in different corners of the market can help provide a reminder that the headlines often miss the full story. With this in mind, we can see cause for optimism in some areas of the stock market along with a combination of explanations for the volatile conditions in other areas.

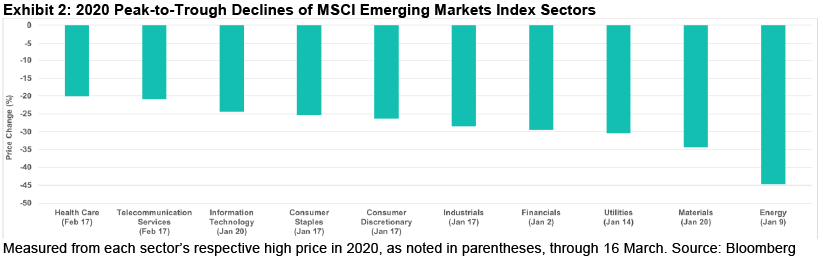

There’s no getting around the tough conditions of the past few weeks as performance patterns have been similar in developed and emerging markets. Exhibit 2 shows emerging-market sector declines, which generally started earlier (besides health care and telecommunication services) as China’s frontline battle against the COVID-19 outbreak had an outsized impact on emerging-market performance.

The divergent performance across sectors around the globe encapsulates the importance of taking a diversified approach to investing. An investment portfolio concentrated in the worst-performing sectors would have fared much worse than a more broadly allocated alternative.

Looking ahead, there are two ways to respond to this state of affairs: stick to your long-term plan or sell.

We believe it’s deeply inadvisable to sell for a couple reasons. First, it’s entirely possible that stocks are closer to the bottom than the top. If you’ve remained invested up to this point, then you have already borne much of the decline. Second, if you decide to sell, when will you re-invest? If you can’t provide a realistic answer to that question, then it’s probably better to remain patient with your long-term plan in anticipation of the eventual recovery. It’s better to sit tight with the vast majority of your portfolio than to sell at low prices today and buy back in at higher prices later.

Important Information

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.