How Brexit Affects Our Funds

The UK’s departure from the European Union (EU) promised to be messy and full of uncertainties from the start. This time last year, we had figured that some sort of deal with the EU would eventually be made in order to avoid a hard Brexit. That turned out to be the case, although the negotiations went on for as long as they possibly could before 1 January, when the Brexit withdrawal agreement is implemented.

The skinny on the skinny deal

The result is a “skinny” deal that allows the UK to gain preferential access to the EU market for its goods as long as it follows many of the EU’s rules and regulations as they apply to governance, labour and the environment. If those standards change in the future, the UK will be permitted to deviate from them and will be able to challenge future disputes in an independent court.

Despite years of talks, the deal only relates to traded goods (such as manufacturing and agriculture). This zero-tariff/zero-quota trade arrangement comes at a cost, as businesses that trade with the EU will now be burdened with additional expenses and red tape. Although politicians and the media will likely point to tariff-free trade, the UK’s significant—and higher value-add—services sector (which accounts for about 80% of the UK’s economy) will face challenges in continued access to the single market.

For financial services, meanwhile, the elephant in the room remains the concept of equivalence. The EU can unilaterally decide whether to allow UK-based financial businesses to continue selling directly to EU-based clients. It also reserves the right to withdraw equivalence at short notice. To mitigate this risk, some banks have already started moving assets and staff from London to EU financial centres, such as Frankfurt, Paris and Dublin.

In short, the deal avoids the prospect of an economic rupture, but at the cost of increased trade friction and ongoing uncertainty in several important areas.

The market’s response to the deal has been relatively muted—and is not easy to disentangle from the ever-changing news on COVID-19. Investors have had four years to digest the economic damage from Brexit; it is well understood by now and we believe it is reflected in the prices of UK equities and currency. One notable reaction was a sell-off in UK banking stocks, which implies that the market was hoping for a bit more clarity from the deal.

Our view

While the negotiated outcome is better than a no-deal Brexit, the UK has suffered from a long period of intense uncertainty (which continues to a degree, as the divorce from the EU addressed the transfer of goods, but not commerce in services). We still expect Brexit to weigh on economic growth in the years ahead, with the UK likely set to underperform other regions in the world, such as the US and Asia.

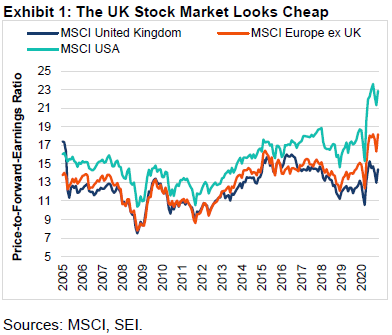

Earnings expectations follow the economic trends. Exhibit 1 looks at the forward price-to-earnings ratio of the MSCI United Kingdom, MSCI Europe ex-UK and the MSCI USA Indexes. UK equities appear cheap. But there are a few bright spots on which investors may choose to focus.

First, the development and distribution of the COVID-19 vaccines should drive the global economy to higher ground in 2021—and should benefit the large energy, materials and industrial multinationals that comprise almost one-third of the market capitalisation of the MSCI United Kingdom Index.

Second, the UK appears competitive versus other advanced countries when measured by various benchmarks, such as relative unit labor costs.

Finally, as a hard Brexit has been avoided, we also believe that investors may be more likely to hunt for bargains in 2021, pushing equity prices closer to global averages. This would also benefit sterling.

Sterling rallied in the days leading up to the deal announcement, but has since retraced most of its gains. UK government bonds, meanwhile, have been one of the strongest-performing G7 markets through 2020. However, there has been a noticeable decoupling from other core sovereign bond markets in December. Gilt yields have rallied (fallen), whereas government yields in the US, core Europe and elsewhere have sold off (risen). Developed-market government yields are usually correlated; therefore, this suggests to us that, despite the agreed-upon deal, investors are concerned about the UK’s future economic growth trajectory compared to its peers. The market has priced in an increased likelihood of another Bank of England interest-rate cut that could take the base rate into negative territory.

Our funds

Equities

It’s worth remembering that the UK equity market is not representative of the UK economy. With the exception of banks, the largest benchmark constituents are global energy, materials, consumer staples and pharmaceuticals stocks. That sector make-up largely explains why the UK equity market is trading on a relative discount (certainly to the US)—investors are seeking high-tech growth stocks (of which the UK has close to zero representation) rather than those in financials, commodities and low-growth defensives.

The shadow of Brexit has also hurt investor sentiment towards many stocks that are not exposed to Brexit risk directly due to their global footprint. This poor sentiment towards the UK market (due to sector make-up and Brexit woes) has created opportunities for value-aware stock pickers, as the concerns are arguably already priced in.

The UK Equity Fund has a definite domestic bias and is overweight economically-sensitive cyclical stocks, such as those in the financials, industrials and consumer discretionary sectors. It is underweight global sectors—such as consumer staples and health care (largely on valuation grounds, as these sectors are cheap, particularly given the potential earnings growth from any cyclical recovery)—as well as energy and materials on quality considerations. Any adverse impact on the UK economy that arises from the new trading regime is likely to affect the Fund.

The Europe ex-UK Fund does have some off-benchmark UK exposure—a combination of domestic industrials and global media-related stocks. These are held on valuation grounds; however, given the low exposure and the range of stocks held, these stocks should not be notable drivers of Fund performance.

The Global Equity Fund and Global Select Equity Fund are exposed to UK equities through their value-oriented managers who purchase undervalued securities and avoid the expensive parts of the market. We expect these managers to benefit from a likely economic recovery in 2021, which should add significant fuel to the nascent value rotation.

A bursting of the tech bubble would also be relatively beneficial as our managers avoid the richly valued securities in that sector. Our currency specialist Rhicon is trading purely on technical indicators and should continue benefit from an environment of rising foreign exchange volatility; however, the manager may experience headwinds if risks subside.

Finally, we do not take directional bets on the UK equity market, and we hedge our country exposure back to the MSCI World Index.

Fixed income

Our global bond funds’ benchmarks have single-digit exposure to sterling-denominated bonds.

We currently have an underweight bias to UK duration, but a modest overweight to sterling. UK assets have been unloved for a number of years (for understandable reasons) and this is reflected in the currency, which remains undervalued according to most long-term valuation metrics. We therefore see some potential upside from here; although we acknowledge that negative sentiment could continue to weigh on sterling for some time.

The underweight to UK duration is based on the view that UK gilts offer poor value, pushing investors out to 7 years on the curve to find positive yield. We think we can find better value in other sovereign bond markets, where real yields are more attractive (in other words, less negative) and the debt dynamics less burdensome.

Issues outside of the UK account for nearly half of the UK Credit Fund’s benchmark, and contribute close to 40% of the benchmark’s spread. Foreign issuers in the benchmark include US-based McDonald’s and Comcast, EDF in France (which is partially owned by the French government) and Korea Development Bank and East Japan Railway Company. These issuers take a global currency approach to funding their balance sheets, opportunistically tapping attractive funding rates. As a result, the Fund benefits from a globally diversified portfolio of companies with sterling exposure common to investors’ base currency.

The Fund’s spreads have tightened within their January 2020 starting point, and are now marked at 99 basis points over UK gilts. There has been marginal risk reduction; although the Fund continues to maintain its focus on financials and securitised sectors.

Important Information

Past performance is not an indicator of future performance.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The views and opinions within this document are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission ("SFC")

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to "institutional investors" pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to "relevant persons" pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the "SFO"). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.

SOUTH AFRICA

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa. A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all of the risks applicable to our funds, please refer to the fund’s Prospectus. Please contact you fund adviser (South Africa contact details provided above) for this information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

SEI sources data directly from Factset, Lipper, and BlackRock, unless otherwise stated.