Has Value’s Run Just Begun? Part 5: The Value in Rising Rates

When the U.S. Federal Reserve increases its overnight lending rate for banks (the federal-funds rate), it effectively increases all other lending rates—and signals that the central bank is trying to temper building inflationary pressure and accelerating economic growth. This can have a range of implications on equity and fixed-income markets.

For fixed-income investors, rising interest rates provide an opportunity to generate higher returns as yields (the rate of interest paid to bond investors) move higher. Recently, for example, the yield on 10-year U.S. Treasurys jumped from an all-time low of about 0.5% in August 2020 to approximately 1.7% at the end of May 2021. On the other hand, most equity markets tend to struggle in rising-rate environments. As investors took advantage of the chance to earn higher returns on fixed-income investments (which do not require the level of risk typically associated with equities), valuations of growth stocks diminished over the nine months ending May 31.

Value stocks, however, behaved quite differently during that period—rebounding along with the rising interest rates to ultimately outpace the long-favored growth stocks, with the Russell 1000 Value Index returning 33.89% and the Russell 1000 Growth Index gaining just 10.90%. We believe that value stocks will continue to gain as higher interest rates continue to make the future cash flows of growth stocks less attractive.

Value and rates: Is there a connection?

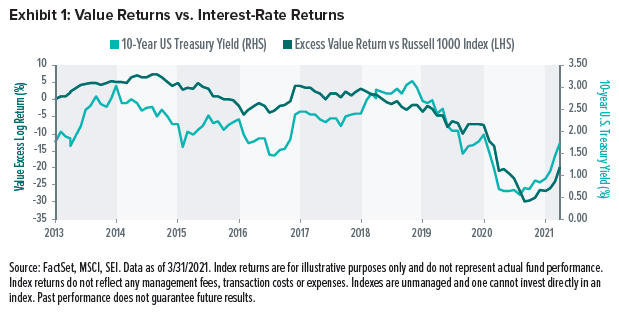

Over the past eight years, value stocks (as measured by the Russell 1000 Value Index versus the Russell 1000 Index) have moved in tandem with long-term interest rates (measured by the 10-year US Treasury yield) as the outlook for each have been generally in sync. This is illustrated in Exhibit 1.

This is not to say that investors should expect interest-rate movements to impact equity markets in the same way all the time; there are a variety of factors that can influence market trends such as economic growth and inflation expectations. With that said, there are consistencies in the ways investors have tended to behave in a given interest-rate environment.

Rising rates: Bad for most equities…but worse for growth and quality?

When interest rates are on the decline, investors typically flock to companies with faster-than-average earnings growth while disregarding valuation measures. Therefore—because lower interest rates tend to boost the current value of a company’s future expected cash flow—growth stocks generally have performed best amid falling interest rates and rising company earnings.

During higher interest-rate environments, on the other hand, investors have tended to regard valuation measures as important (we believe they are always important). Because while rising rates may reflect a healthier economy, they can also diminish the future value of a company’s earnings—making high-priced shares particularly unattractive to investors. The conventional wisdom, then, is that during periods of rising rates, value stocks with strong existing cash flows (which may have been overlooked when interest rates were low) have the potential to outperform growth and quality stocks (companies with high-quality fundamental characteristics) as investors grow more sensitive to valuations.

Another reason value tends to fare better in rising-rate environments is because of discounted cash flows. For stable compounders (quality stocks) and growth companies, future discounted cash flows are high when discounting at a low rate. For value companies, a low discount rate is irrelevant because their distant cash flows are small. Therefore, while all three asset classes may suffer from rising rates, value stocks would likely suffer less than quality and growth.

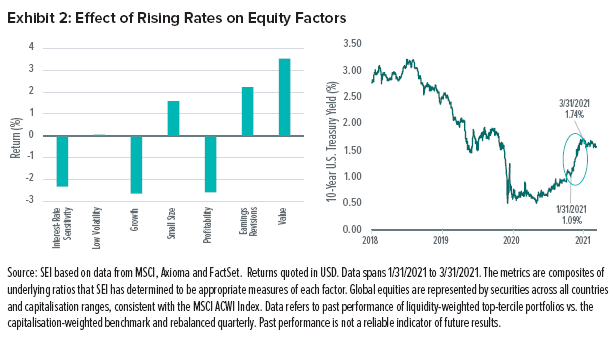

Exhibit 2 looks at the effect that rising rates had on several equity factors. Each factor can be thought of as an attribute of a security that can be used to help explain returns. The favorability of each factor may change as the economic cycle progresses through different stages. As you may expect, value stocks were the primary beneficiary of rising rates over the two months ending March 31. Small-capitalization stocks, which tend to be more value-oriented than large caps, also performed well during the period.

Outlook

We believe there is likely some short-term synchronization between returns to value and interest rates in the current market environment. Fixed-income markets are signaling improved growth prospects on the tail of higher interest rates. On the inflation front, inflation expectations are higher in the short term than in the long term which should provide a tailwind in the near future. If the acceleration in measured, and inflation proves stronger and longer-lasting than investors expect, bond yields could climb appreciably from today’s levels and generate further tailwinds for value.

Glossary

Composite metrics are metrics whose values are defined by a combination of quantitative assessments.

Discounted Cash Flow is a method used to estimate the value of an investment based on its future cash flows.

Earnings revisions refers to stocks whose earnings estimates show momentum in being revised higher.

Growth stocks exhibit earnings growth above that of the broader market.

Interest-rate sensitive stocks are likely to move higher or lower due to changes in interest rates.

Low-volatility refers to stocks that are less volatile than the broader market.

Profitability refers to stock that generates profits more efficiently than the broader market.

Small size refers to stocks with a market-cap smaller than the broader market.

Value stocks are those that are considered to be cheap and are trading for less than they are worth.

Index Definitions

MSCI ACWI Index measures the equity performance of large- and mid-cap stocks within the developed and emerging markets.

Russell 1000 Value Index measures the performance of U.S. large-cap value stocks.

Russell 1000 Growth Index measures the performance of U.S. large-cap growth stocks.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.