Has Value’s Run Just Begun? Part 3: Value stocks—still a good time to buy?

Early in 2020 as the COVID-19 crisis swept across the world, economies around the globe struggled amid government-mandated lockdowns and surges in remote working. Economically sensitive stocks (energy, financials, industrials) suffered too—while so-called stay-at-home equities, which comprise mostly growth and mega-cap technology names, benefited from the world’s suddenly acute dependence on the products and services that those companies provide.

By summer of the same year, as beaten down cyclical stocks began surprising with less bad earnings, the market began looking beyond the pandemic. Investor sentiment toward cyclical and value stocks strengthened at the expense of growth stocks, driven by building optimism for strong vaccines that began to calm the pandemic panic and offered a clear way out of the crisis for both politicians and investors.

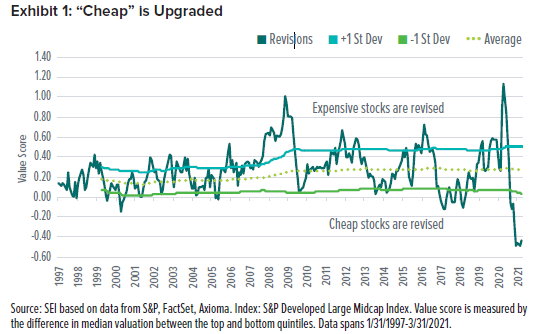

Companies began to project a brighter future and analysts started updating corporate earnings forecasts and upgrading their ratings on value stocks. In fact, Exhibit 1 demonstrates that cheap stocks are being upgraded at the fastest pace in 25 years. This sparked an equity-market rotation away from stay-at-home stocks and toward long-suffering economically sensitive value stocks, culminating in March 2021 with the two best quarters for value investing since 2001.

We believe that now is not the time to lock in your gains

Cheap (value) stocks tend to benefit from accelerating economic activity due to their higher exposure to cyclical businesses at economic troughs. For example, companies in the economically sensitive consumer discretionary sector (which includes furniture, travel, clothing and automobile companies) typically see an uptick in sales as the business cycle moves toward recovery and consumer spending increases.

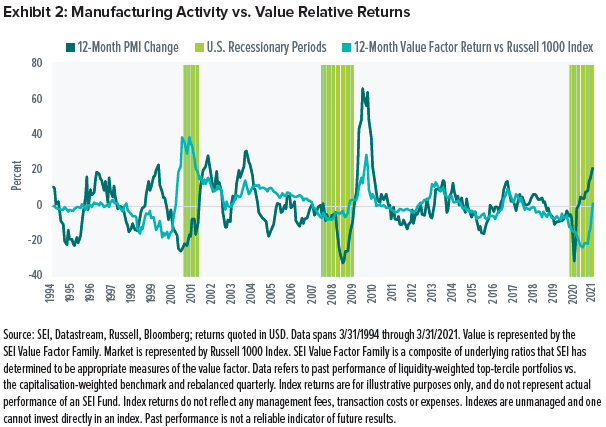

As illustrated in Exhibit 2, the rolling 12-month return on value stocks tends to be highly correlated with changes in the manufacturing activity, as measured by Markit’s US purchasing managers’ index (PMI). (We use this measure as a proxy to assess the global economy’s health because U.S. consumers purchase goods from across the world and represent the largest single block of consumers globally.)

Exhibit 2 also shows that manufacturing activity tends to go in a negative direction as the business cycle moves into recession, while it turns positive in the early stage of an economic recovery, such as in the 2008-to-2009 period. This was also the case in the early stages of the COVID-19 pandemic, with the PMI turning negative as the economy went into recession—nearing levels last seen in 2008—and moving sharply higher as economies began to reopen.

While we can’t say with certainty where the economy will go from here, we believe that a further acceleration in economic activity is likely due to continuing reopening, generous fiscal stimulus and pent-up demand—which should continue to benefit pro-cyclical and value stocks in the near term. Demand from Europe, which is mostly still under lock-down, is also likely to increase as vaccination programs finally get up to speed. The arrival of summer heralds a shift to outdoor activities in the Northern Hemisphere which should help to further slow virus transmission.

Cost pressures have begun to rise

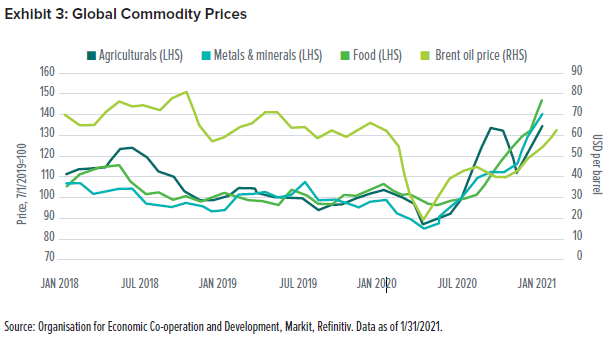

Supply-and-demand dynamics have shifted as consumers begin to return to their pre-pandemic buying habits. As illustrated in Exhibit 3, this has resulted in soaring commodity prices compared to their low points in 2020. Most significantly, by January 2021, the costs of food, agricultural raw materials and precious metals all exceeded their pre-pandemic levels. While oil remains slightly cheaper than it was before COVID-19 hit, its price has also increased significantly from its recent low.

Higher yields in the U.S. Treasury market appear to reconfirm this view. The rebound in value stocks has overlapped with the yield on 10-year U.S. Treasurys increasing from an all-time low near 0.5% in August 2020 to about 1.7% at the end of March 2021. Rising yields are a sign of both economic growth and inflationary pressure—and we believe value stocks will continue to benefit as higher interest rates make the future cash flows of growth stocks less attractive.

In the short term, it’s virtually impossible to say for sure whether, when, or with what speed inflationary pressures will remain. The reality is that inflation is currently rising and will likely continue higher in the near term.

Buying opportunity?

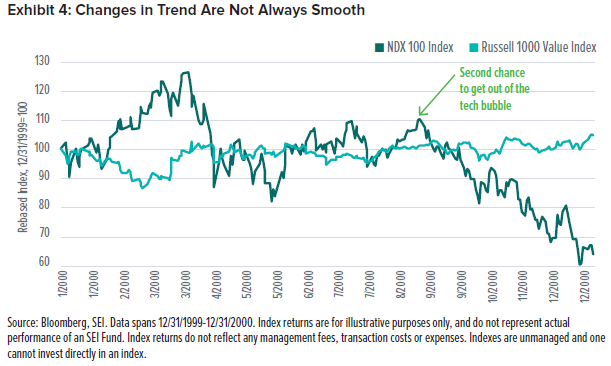

Exhibit 4 shows how changing trends have plenty of volatility over shorter horizons. We believe this new multi-year rally in value is not going to be an exception from the historic patterns. Short-term wrinkles in vaccinations or simply buying frenzies on dips in overvalued “glamour” stocks are inevitable. When that happens, long-term investors could treat such events as value-stock buying opportunities. We saw it in 2000, and we will likely see it again.

Our View

Value occupies one of the key strategic pillars in our investment philosophy. Yet sometimes, cheap stocks offer opportunities that go far beyond the strategic argument. We believe now is such time, supported by accelerating economic activity (good for cheap cyclicals), rising interest rates and inflation (bad for expensive growth and quality), and avoidance of exuberantly priced market segments (we recommend checking the prices on GameStop, crypto prices and SPACs for a measure of exuberance).

The next entry in this series—Has Value’s Run Just Begun?, Part 4: Value Stocks—We believe Now is the Time for Active Management—explores how value, quality and growth have different historical return patterns over the short and long term as rates climb.

Glossary

Crypto refers to cryptocurrency, a digital currency that uses an online ledger to secure transactions.

Cyclical stocks are those whose performance is closely tied to the economic environment and business cycle.

Economic trough is the stage in an economic cycle when the economy hits its low point and growth begins to recover.

Fiscal stimulus refers to actions taken by the government intended to raise economic output and incomes, such as lowering taxes or increasing public debt.

Great Rotation refers to the notion that investors may be trading out of expensive growth stocks and rotating into value and cyclical sectors.

Mega-cap stocks are companies with market capitalizations over $200 billion.

Pro-cyclical stocks tend to be correlated with the overall economy and typically increase when the economy is growing quickly.

Quality stocks are companies with more reliable earnings and low debt.

SEI Value Factor Family is a composite index of underlying ratios that SEI has determined to be appropriate measures of the value factor.

SPAC refers to a special purpose acquisitions company set up by investors to raise capital and acquire an existing company.

Standard deviation is a measure of risk used to gauge the volatility of an investment.

Value stocks are those that are considered to be cheap and are trading for less than they are worth.

Yield is the expected annual return of a fixed-interest security.

Index Definitions

Purchasing Managers’ Index (PMI) is based on a survey of manufacturing executives that is used to measure economic activity within the U.S. manufacturing sector.

NDX 100 Index is a capitalization-weighted index that measures the performance of approximately 100 of the largest non-financial companies listed on the Nasdaq stock market.

Russell 1000 Index measures the activity of the U.S. large-cap equity market.

Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe.

S&P Developed Large Midcap Index measures the performance of stocks representing the top 85% of float-adjusted market cap in each developed country.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.