Global Equities: Why we Keep the Faith With Our Value Managers

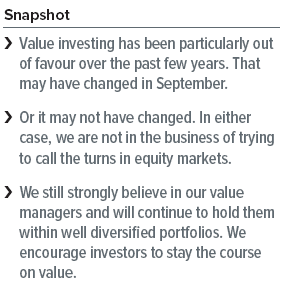

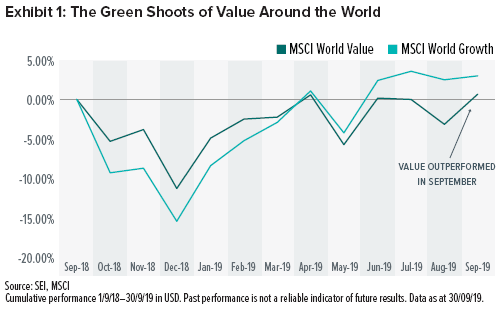

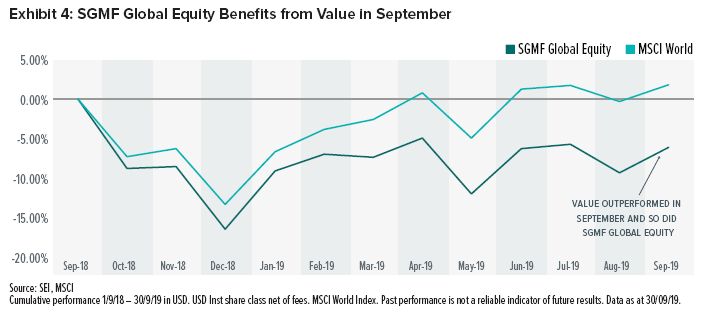

It may seem like value has been out of favour for as long as anyone can remember, but September saw a renaissance in value. On 9 September, global equity markets recorded the largest one-day payoff to value since the “Tech Bubble” began its implosion in March of 2000. One great day in a strong month for value doesn’t necessarily mark the turning point, and we’re loath to try to call the turn as that is generally a fool’s errand. Still, performance was encouraging in September and we were quite pleased with the overall performance of the value managers in our global equity portfolios.

September was not the only time in the past year that value outperformed growth as measured by MSCI and Russell indexes. The end of 2018 was also a strong period for value, but we note that it took place during a market correction (decline of at least 10%) and that the value indexes were led by the performance of utilities. In SEI’s view, utilities are relatively expensive and generally exhibit characteristics more associated with the stability alpha source. Index providers typically include utilities in their value indexes due to the slower growth in the sector. We’re more encouraged by September’s performance, as it was led by financials and energy stocks.

Confidence Remains

Although our value managers have predictably struggled over the past few years when compared to broad market or growth benchmarks, we remain confident in these managers. Each of the managers is subject to a thorough screening and evaluation process prior to being hired. Re-evaluation triggers are established, and we highlight that none of the value managers in our global equity portfolios have triggered a re-evaluation as of 30 September. It is important to keep in mind that simple performance is not part of the re-evaluation triggers. More typically, we are looking for personnel consistency, style purity, asset levels and organisational consistency. All of which these managers have maintained.

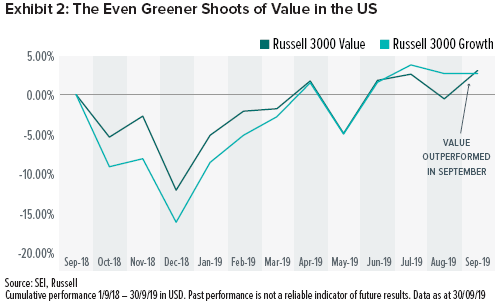

Meet the Value Managers

For global equities we have also chosen regional specialists as opposed to global generalists for implementation of the Value alpha source. Value may look different from country to country or region to region. We believe this specialist mandate allows a more pure implementation of value.

Alpha source is a term used by SEI as part of our internal classification system to categorise and evaluate investment managers in order to build diversified fund portfolios. An alpha source is the investment approach taken by an active investment manager in an effort to generate excess returns. Another way to define an alpha source is that it is the inefficiency that an active investment manager seeks to exploit in order to add value.

Momentum refers to the tendency of assets’ recent relative performance to continue in the near future.

Stability refers to the tendency of low-risk and high-quality assets to generate higher risk-adjusted returns.

Value refers to the tendency of relatively-cheap assets to outperform relatively-expensive assets.

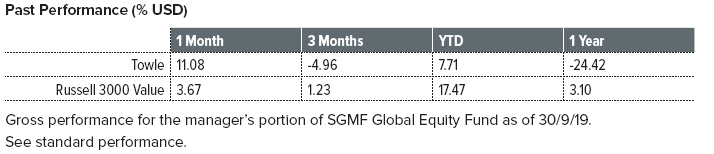

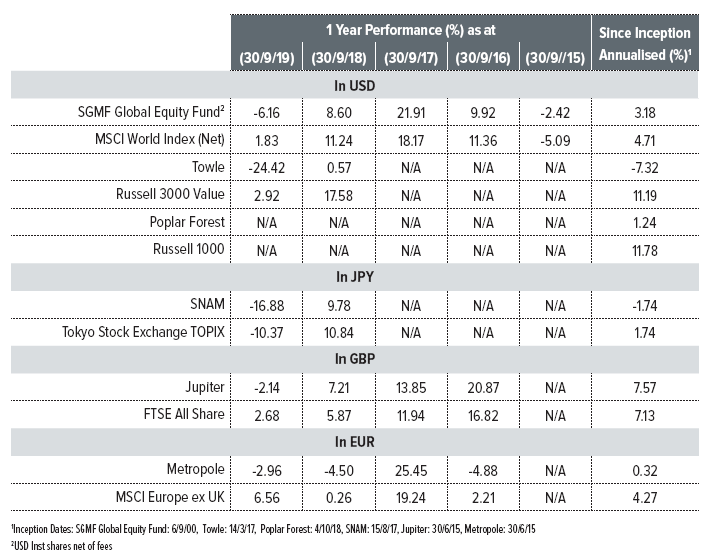

Towle & Co.–US All Cap Value (Information correct as at 30/9/19)

Strategy Description

Towle & Co. seeks to create capital at above average rates of return by investing in out-of-favour and underappreciated businesses in the public equity space. The firm does not manage its portfolio against the composition of a particular benchmark, but rather strives to invest in companies which meet its deep-value criteria and present attractive appreciation potential within a three-year timeframe. The US Value strategy is a slight variant of their flagship Deep Value strategy, with the primary difference being the elimination of microcap names and the flexibility to be All-Cap in nature.

What We Like

- Towle is dedicated to its deep-value philosophy. We have found few managers who have the willingness to invest in this segment of the market, so the exposure they provide is unique.

- The Towle family has a significant amount of assets (over $100 million) of its personal wealth invested in the firm’s strategies, aligning their interests with clients.

- Towle’s approach is research intensive, and it goes through a structured process that includes checklists and documented thesis drivers.

What We Don’t Like

- The portfolio is highly volatile and exhibits significant tracking error, which could be difficult for some clients to accept.

- The US Value product is a custom implementation for SEI that is similar to Towle’s flagship Deep Value product. While there could be risks with SEI as the strategy’s sole client, we are comforted that there is heavy overlap between the two products.

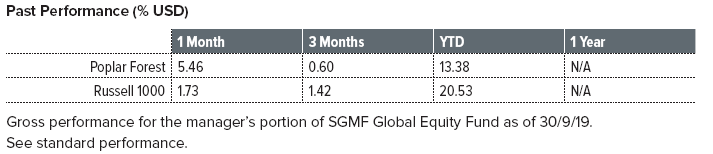

Poplar Forest Capital, LLC – US Value (Information correct as at 30/9/19)

Strategy Description

The Poplar Forest US Value Strategy will generally focus on out-of-favour and underappreciated companies. It has a long-term time horizon and is benchmark agnostic with a focus on normalised earnings and free cash flow. The investment team evaluates investment opportunities using bottom-up, fundamental analysis, paying particular attention to its belief about future normalised margins and free cash flow. The portfolio is concentrated and invests in the US large- and mid-cap segments of the equity market.

What We Like

- Poplar Forest founder Dale Harvey began his investment career in 1991. He worked at Capital Group for 16 years, where he ultimately became a portfolio manager responsible for over $20 billion in value-oriented assets. He has been through multiple market cycles, particularly as it relates to value investing.

- Poplar has a holistic, thoughtful philosophy around value investing and doesn’t take a “one size fits all” approach. Rather than just buying statistically cheap stocks, Poplar uses a normalised earnings method and seeks to buy companies that are under-earning and expected to revert to a mean level of profitability in the future. It is willing to balance quality and value depending on the current market opportunities which should help it better weather a full market cycle.

- All but one investment team member has ownership in the firm, and all analysts are dedicated to the contrarian value product. They all share a common value based investment philosophy. We believe Poplar’s structure and focus are advantageous compared to most peers.

What We Don’t Like

- Poplar has a narrow product offering and most clients know them only for their concentrated flagship value portfolio. The concentrated approach is suitable only for a select list of clients. Therefore the asset base could be at risk if clients are unable to tolerate the expected volatility. Additionally, given the shift from active to passive investing particularly in the US large-cap market, new clients could be hard to come by.

- In 2019 Poplar brought on the two lead portfolio managers from the Nuveen NWQ Small Cap Value strategy, Phyllis Thomas and Greg Tenser. We have mixed views on this move. From a positive standpoint, this could be beneficial to the firm as it diversifies the product lineup and gives Poplar a potential new avenue of growth. From a negative standpoint, we need to be mindful of resource allocation. We are told that the Poplar analysts will continue to focus a majority of their time on the flagship large cap products which Dale oversees.

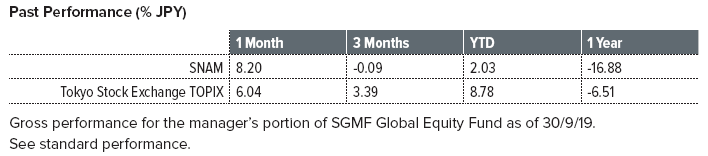

Sompo Japan Nipponkoa Asset Management CO., LTD (SNAM)–Japan Value Equity (Information correct as at 30/9/19)

Strategy Description

SNAM seeks to identify securities in the marketplace that have been damaged by market behaviour which leads them to an opportunity to exploit the aforementioned inefficiency. They begin their idea generation with the application of the Dividend Discount Model (DDM) which feeds to the portfolio construction process. In addition, the team uses a universe of 700 stocks that must have market capitalisations higher than 20 billion yen, have liquidity of more than 20 million yen per day and achieve a credit rating of BB or higher.

What We Like

- The well-structured and robust process, which features comprehensive coverage of factors and a strong emphasis on unbiased inputs, enables the manager to prioritise information and focus research efforts effectively.

- The portfolio construction process is disciplined and rigorous, which secures the consistent implementation of the manager’s investment philosophy.

- With catalysts serving as the driving considerations for both stock selection and sizing decisions, the manager has a proven track record of efficiently managing opportunity cost through buying and selling stocks close to their price inflection points.

- SNAM stands out as a middle ground between traditional domestic Japanese managers and the Japan equity subset of global asset managers: It enjoys the merits of abundant resources and local know-how while maintaining its consistent investment approach and relatively flat decision-making approach.

What We Don’t Like

- The team is exposed to the possibility of business risk and organisational instability, as SNAM is a subsidiary of a large firm with a history of dynamic organisational changes—although the concern is not immediate.

- The remuneration of the team’s investment professionals weakly aligns with the investment goal. However, we believe the negative impact is contained, as the Japanese working culture mostly mitigates the risk of talent loss. Also, the relatively inflexible job market strengthens the linkage between an individual’s career progression and capability of generating long-term alpha.

- While we believe the value bias is inherent in the manager’s belief, we remain concerned that the adoption of and reliance on the DDM model for stock selection could lead to investment style drift if there are significant outlier assumption inputs from the analysts.

- There is limited effort to evolve or improve the process.

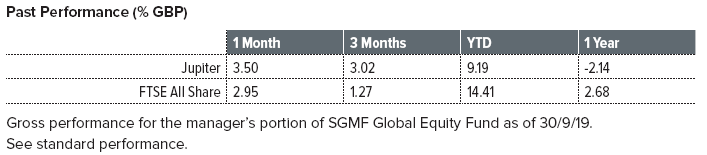

Jupiter Asset Management Ltd – UK Value Equity (Information correct as at 30/9/19)

Strategy Description

Jupiter takes an intrinsic value approach to UK equities based upon a normalised (as opposed to current/forecast) earnings measure. This is a well-documented, if not widely used, approach grounded in the principles of Graham & Dodd that has been shown to outperform other value strategies over time. The portfolio manager seeks to hold shares in out of favour and lowly valued companies, but ones that will typically have prominent franchises and sound balance sheets. Such shares will tend to be out of favour because they are unfashionable, have suffered a fall in profitability or are in industries where there are concerns on future prospects.

What We Like

- Core to the investment thesis is portfolio manager Ben Whitmore’s ability to effectively implement an intrinsic value approach based upon a normalised earnings measure. Assessing stocks on the basis of their long- term normalised earnings is a means of protecting against the ‘value traps’, situations when cyclical stocks appear misleadingly cheap while trading on peak margins.

- Quality is assessed subjectively (e.g. assessment of management quality) and objectively (balance sheet strength, free cash flow generation, accruals, return on assets, leverage, etc). Combining value with quality adds value over and above the value factor. Careful quality considerations have reduced the exposure to value traps and delivered more consistent performance.

- Whitmore has demonstrated his ability to outperform a mechanistically implemented factor-based strategy.

- There is no “house style” at Jupiter; UK Equity Value is purely Ben Whitmore’s product. We believe that Ben is a good value investor, as he has strong conviction in his approach and remains true to his style in exuberant times. He is thoughtful, measured and humble. Ben has displayed patience with respect to entering positions that look attractive, erring on the side of caution rather than trying to catch a quick reversal.

What We Don’t Like

- Since the original investment Jupiter IPO’d, as predicted. We have reviewed this with the former and current CEOs and there have been no adverse impacts of the floatation. We continue to monitor for signs of changing culture or aggressive growth plans, etc.

- The team launched their Global strategy in October 2016. If Global assets exceed UK assets, the team’s focus may shift. Therefore, the attention the UK strategy receives going forward is a concern, however the launch of the global product is consistent with Ben’s assertion that he would do so conditional upon Dermot Murphy being fully trained, which has occurred. Our concern is that the team is not sufficiently resourced to maintain in-depth coverage of the UK and build sufficiently deep coverage of Global names without adding resources.

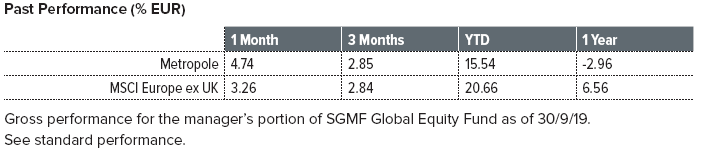

Metropole Gestion – Contrarian European Value (Information correct as at 30/9/19)

Strategy Description

Metropole is an independent, investor-owned firm that runs a high tracking error, concentrated European value equity portfolio. A team of seven investment professionals use a wide array of tools to identify cheap companies such as normalised multiples, sum of the parts, discounted cash flow, etc. keeping track of merger and acquisition developments to learn what companies, as opposed to just money managers, are willing to pay for a business and the right way of valuing it. Understanding and applying different valuation techniques to different industries allows the manager to create a more balanced portfolio of cheap stocks without a typical bias of overweighting industrials and other cyclicals. The portfolio manager and analysts have a clear understanding that buying cheap names alone is insufficient for constructing an outperforming portfolio and they recognise that identifying a catalyst is the most important part of the job.

What We Like

- Metropole’s philosophy is differentiated, pushing beyond traditional value. The objective is to understand the areas of controversy and seek to identify catalysts believed to reduce the extent of mispricing.

- Every stock in the portfolio has a thesis that identifies why it’s cheap, on what metric and what the catalyst will be to unlock value.

- There is a highly experienced and diverse team, who average 20 years of investment experience, led by Isabel Levy. Isabel demonstrates exceptional knowledge and understanding of European equities and value investing. Furthermore, the team is well resourced, with eight dedicated European analysts.

- Metropole is an investor-owned boutique based in Paris. 88.5% of the capital is held by the team, with most owned by CEO and founder Francois-Marie Wojcik and head of fund management Isabel Levy. All analysts are shareholders.

What We Don’t Like

- Isabel Levy is in her mid-50s and has indicated she wishes to retire at 60. Given that she is currently indispensable, we would need to build further conviction in her natural successor, Ingrid Trawinski, to gain comfort.

- There is no formal sector coverage assigned to the team. We view this as an opportunity cost when compared to specialised sector analysis that can develop more profound industry specific insights.

- The documents and process structure are basic. It is reflective of Isabel’s extroverted personality and works for the team, but we are concerned about whether available resources are utilised efficiently.

- The size of Francois-Marie Wojcik’s ownership stake, along with the fact that he is no longer actively involved in fund management, needs monitoring for potential sale/IPO or other personal plans.

Stay the Course

We readily acknowledge the past year has presented its share of performance challenges for the SGMF Global Equity Fund. Still we encourage investors to stay the course. In our view, the case for value has only gotten stronger. Nothing has changed with regard to our value managers; we still like their processes and portfolio managers, and they remain consistently committed to the value alpha source. September was an example of the potential rewards when it all comes together for value.

Standard Performance

Important Information

The SGMF Global Equity Fund is structured as an open-ended collective investment scheme and is authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The fund is managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, to provide general distribution services in relation to the fund. The SGMF Global Equity Fund may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Any reference in this document to any SEI funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI fund are reminded that any such application must be made solely on the basis of the information contained in the prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs.) A copy of the prospectus can be obtained by contacting your financial adviser, SEI relationship manager or by using the contact details shown below.

Data refers to past performance. Past performance is not a reliable indicator of future results. Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Returns may increase or decrease as a result of currency fluctuations. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

In addition to the usual risks associated with investing, the following risks may apply: Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments, securities focusing on a single country, and investments in smaller companies typically exhibit higher volatility.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice.

This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713). SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.