The global bull market: Is it time to get out?

Many investors are concerned that the global stock market may have recently peaked. This is one of the longest bull markets on record, with valuations appearing elevated by some measures and the global economy having avoided recession for almost a decade. At SEI, we regularly receive questions like: “How much longer can this last?” “Are high valuations a warning sign?” “Can the economy keep going?” “Should I sell my stocks?” While these worries are certainly understandable, it’s important to step back and assess them rationally.

Is the bull too long in the tooth?

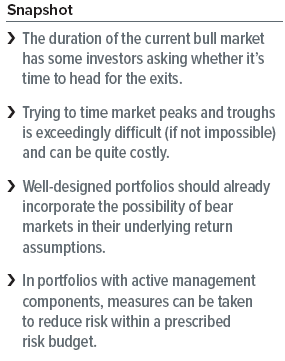

When measured from the bottom of the preceding bear market, the current bull market in global stocks (as measured by the MSCI World Index) is the longest on record. It stands third behind only the 1982-1987 and 1990-1998 bull markets in terms of cumulative returns (Exhibit 1).

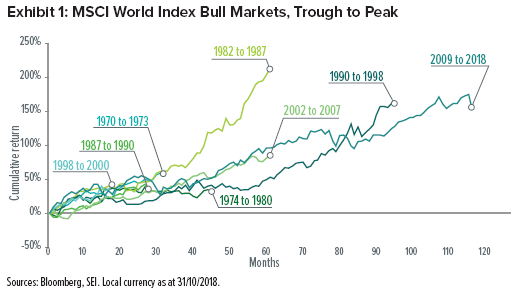

However, when measured from the peak of the prior bull market (an approach that allows us to incorporate the relative severity of the most recent bear-market decline), it is still the longest in terms of duration but less impressive in terms of cumulative return (Exhibit 2).

So, what do these findings tell us about the direction of the current environment? Standing on their own, not a whole lot. For one thing, the “peak to peak” approach in Exhibit 2 may be distorted by previous bull-market peaks that were driven by irrational investor exuberance and complacence. And most importantly, in our view, looking only at cumulative return and duration data constitutes a rather superficial analysis.

Bull markets don’t die of old age

Jim Solloway, SEI’s chief economist, has argued throughout the current cycle that bull markets are typically done in by misguided economic policies—not by old age. From that perspective, the picture is admittedly mixed. Some key central banks are stepping back from the accommodative monetary policies of recent years; this is especially true of the U.S. Federal Reserve which is expected to continue hiking its interest rate target, but it’s also true that the European Central Bank is tapering its asset purchases while the Bank of England recently hiked its interest rate target. There are some important geopolitical concerns at work, including a U.S.-China trade war, the direction of China’s domestic economic policies, Brexit, and the sustainability of the Italian government’s fiscal trajectory.

However, it’s also important to take note of the positives. Central banks are still relatively accommodative, China has been enacting more supportive domestic policies of late, recent fiscal stimulus in the U.S. should be a tailwind for a bit longer, corporate earnings growth is still healthy, and labour market conditions are positive in many countries. Fundamentals – expectations of future cash flows and what their appropriate values are in the present – are the core elements in assessing whether a market is cheap, fairly priced, or expensive. And while the global stock market has been a bit on the expensive side by those measures (less so after the recent correction), it’s not outlandishly so, and it continues to be supported by low interest rates and still-solid sales and earnings growth.

It’s hard to outrun a bear

Of course this bull will not run forever. At some point, the bull market will end and we’ll experience another bear market. When and how that happens is anyone’s guess. In contemplating this inevitability, the question that springs to the minds of many investors is, “What should I do when the next bear market arrives?” Nobody likes losing money, even if it’s just on paper. Research has found that humans tend to feel the pain associated with a loss far more than they feel pleasure resulting from a gain of similar magnitude. (We explain this in more detail in our paper, Behavioral Finance: Loss and Regret Aversion, September 2014.) For many, the knee-jerk reaction to any hint of significant market decline is all-out retreat. After all, investors would experience far less psychic discomfort if they could manage to outperform the market by substantially both avoiding the downside of a bear market and enjoying the upside of a bull market.

Unfortunately, that scenario is extremely unlikely for any investor. Timing the tops of bull markets and the bottoms of bear markets with any meaningful (much less consistent) degree of accuracy is essentially impossible. Using economic turning points—exiting risky investments prior to the start of recession, for example—is equally fruitless, in our view. Consider that it has historically taken economists at the National Bureau of Economic Research anywhere from 6 to 21 months to declare that a recession has already occurred. To the extent that markets are able to discount the future, investors would be well into a bear market, or even into the next bull market, before anyone knew for sure that a recession was underway.

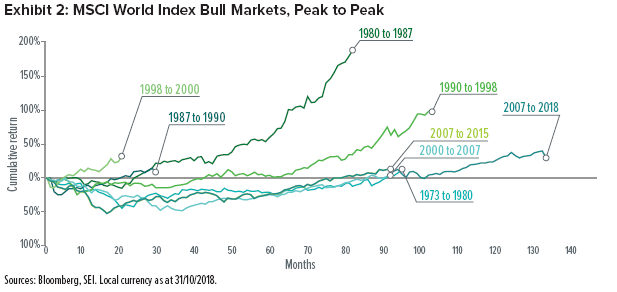

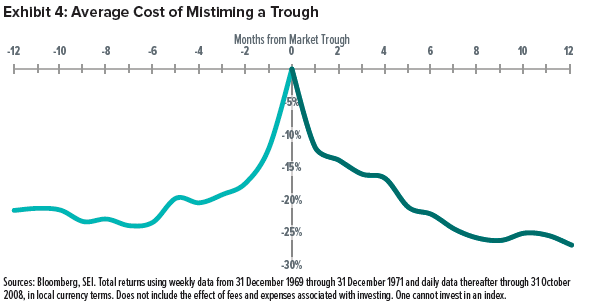

Even more importantly, there is a cost, in terms of lost returns, when trying to time market entries and exits. And judging by the historical behavior of markets around market peaks and troughs, those costs can be significant, as shown in Exhibits 3 and 4. The left-hand line in Exhibit 3 shows the average returns an investor would have foregone by trying to exit a maturing bull market. If timed perfectly, the loss would have been zero, as depicted at the center of the graph. The right side of the graph shows the cost for getting out after the peak. For example, an investor who exited six months prior to the bull market peak would have missed an average subsequent return of 7%, while an investor who exited six months after the bull market peak would have incurred an average loss of 15%.

Of course, an investor may be comfortable with selling a few months after a market peak; the line on the right side of Exhibit 3 shows that this might have at least preserved some capital. But this overlooks the dual nature—and dual risk—of market timing. Once an investor has exited the market, they have to decide when to reenter. And mistiming this decision can also be quite costly, as Exhibit 4 reveals. Again, perfect timing would cost nothing in terms of incurred losses or missed gains, as the center of the graph shows. But getting back in before the end of the bear market would naturally expose the investor to further losses, as the line on the left side of the chart depicts. And most importantly, as the line on the right side of the chart shows, getting back in after the next bull market has already begun can also be quite costly. In this example, a market-timing investor who reentered the market just six months prior to the bottom would have sustained an average loss of 23%, while one who reentered six months after the bottom would have foregone an average gain of 22%.

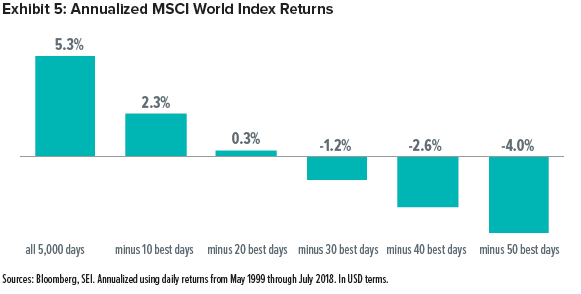

The risk of missing out on the start of a new bull market is also illustrated in Exhibit 5. Looking at a period of 5,000 trading days in the MSCI World Index, missing out on just the best 20 days would have surrendered almost all the returns accessed by more disciplined, strategically minded investors.

But even this analysis is imperfect, as it also assumes that an investor only makes two decisions: when to exit and when to reenter. In reality, nervous, impulsive investors who alternate between risk-seeking (greed-driven) and risk-averse (fear-driven) behavior could incur even steeper costs by attempting to time strategic exposures.

Is there nothing an investor can do?

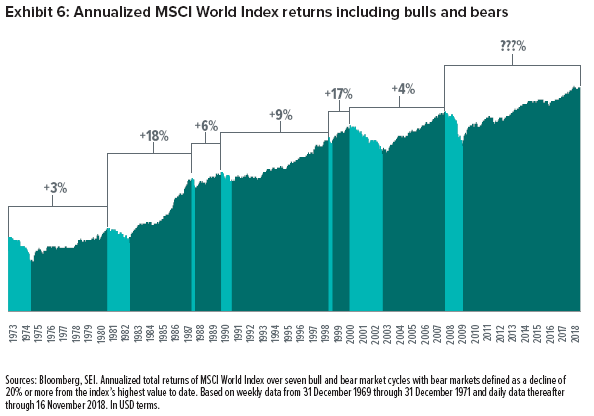

There are two answers to this question. The first is to reorient investors’ thinking when it comes to bull and bear markets (Exhibit 6 takes into account both bull and bear market performance). The second is to keep in mind that active management can be used—within a disciplined risk-budgeting framework—to take advantage of perceived opportunities in markets, including raising or lowering the amount of risk taken (Exhibit 7 provides examples of SEI’s ability to actively manage risks).

The desire to avoid the pain of a bear market is a natural human response to our innate fear of loss. Meanwhile, a well-designed investment strategy already accounts for the fact that markets have return distributions that extend from negative to positive and, importantly, are centered above zero. In other words, equity markets have historically produced positive long-term returns, and the likelihood of both bull and bear markets should be fully reflected in the risk and return expectations used to build a portfolio.

A Better Way to Think About Bulls and Bears

Although this is one of the longest bull markets on record, it’s not clear that it’s “long in the tooth.” Valuations do look a bit extended, but we think strong fundamentals should be supportive. While bear markets have often coincided with economic downturns, it’s impossible to consistently and accurately predict when economic recessions and recoveries will occur and how markets will respond to these cycles. Most importantly, it’s easy to overlook that trying to time market exits and entries is not free. Unless they are timed almost perfectly, there are potentially significant costs in terms of lost returns. In other words, it is exceedingly difficult to come out ahead when trying to time financial markets. It’s also important to keep in mind that portfolios are designed using long-term return, volatility and correlation expectations for various asset classes. As long as these expectations are realistic (and adjusted when appropriate), they should account for bull-market returns, bear-market returns, and everything in between. Holding a thoughtfully designed, well-diversified portfolio should allow an investor to ride out the ups and downs of financial markets with the greatest probability of success. We believe that active management can play a meaningful role in positioning around valuation, economic, and other concerns—but should be done within a well-defined risk budget that still keeps a portfolio close to its strategic intentions.

Important Information

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited (“SIEL”) acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global, Limited, an affiliate of the distributor. SIEL utilises the SEI Funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI Funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application must be made solely on the basis of the information contained in the Prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs.) A copy of the Prospectus can be obtained by contacting your Financial Adviser, SEI Relationship Manager or by using the contact details shown below.

Data refers to past performance. Past performance is not a reliable indicator of future results. Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Returns may increase or decrease as a result of currency fluctuations. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

In addition to the usual risks associated with investing, the following risks may apply:

Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments, securities focusing on a single country, and investments in smaller companies typically exhibit higher volatility.

Issued by SIEL 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. This document and its contents are directed only at persons who have been categorised by SIEL as a Professional Client for the purposes of the FCA Conduct of Business Sourcebook. SIEL is authorised and regulated by the Financial Conduct Authority.

SEI sources data directly from Factset, Lipper, and BlackRock, unless otherwise stated.

Important Notes:

The SEI Funds may not be offered or sold to the public in Argentina, Brazil, Chile, Colombia, Mexico, Peru, Venezuela or any other country in Central or South America. Accordingly, the offering of shares of the SEI Funds has not been submitted for approval in these jurisdictions. Documents relating to the SEI Funds (as well as information contained herein) may not be supplied to the general public for purposes of a public offering in the above jurisdictions or be used in connection with any offer or subscription for sale to the public in such jurisdictions.