Factor Investing: Finding Balance between Active and Passive

During the epic bull market that finally ended its record-long run in early 2020, there was a proliferation of index-tracking products—which left investors to navigate newly abundant information about the relative merits of active and passive investment strategies. At SEI, we allocate to both approaches in order to gain exposure to their respective benefits while offsetting their distinct limitations, in pursuit of improved risk-adjusted returns. Factor investment strategies fall between active and passive on the risk/return spectrum—transcending the pitfalls of each approach while reconciling their advantages.

Bridging the divide

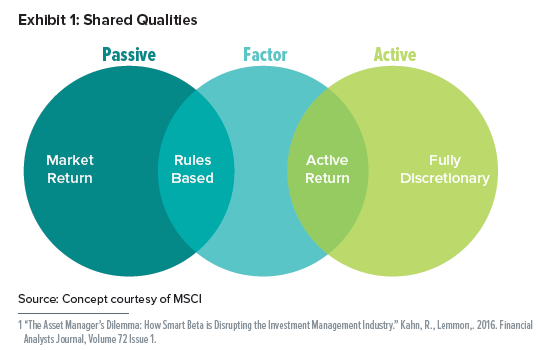

Factor investment strategies employ a transparent, rules-based approach to portfolio construction that provides systematic exposure to factors, that is, characteristics historically associated with excess risk-adjusted returns1 This means factor investing possesses beneficial attributes of both active (potential excess returns) and passive strategies (rules-based simplicity and lower costs). Exhibit 1 shows the areas in which these three approaches overlap.

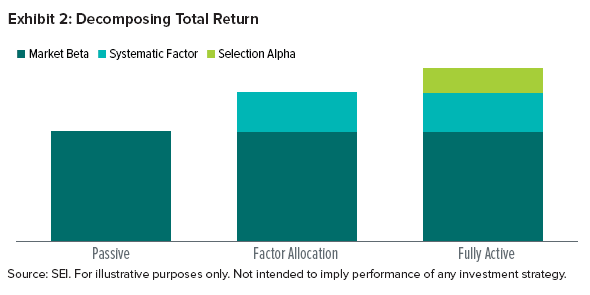

Exhibit 2 depicts a breakdown of total returns across these three approaches. We see that the return of passive strategies can be fully explained by market performance, or beta. Factor investing builds on this base by deriving potential excess return from systematic exposure to structural market inefficiencies. Active strategies build further still, also seeking potential excess returns, via both factor exposure as well as security selection.

Behaviour: Motivating factors

Where do factors originate? Behavioural finance theory posits that investors make decisions that tend to reflect concerns about fear and greed. Such behavioural biases, in aggregate, create inefficiencies at the overall market level, which can create opportunities for other investors to generate excess returns. These inefficiencies can be volatile over the short-term and are sensitive to cyclicality, but have also demonstrated historical long-term persistence.

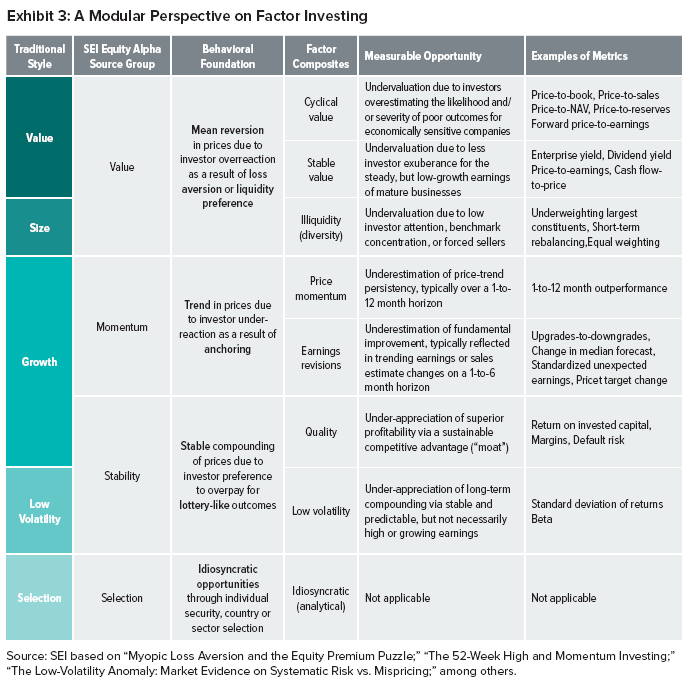

SEI categorises these factors into three primary families that have been empirically identified, along with the behavioural anomalies that drive their persistence:

- Value: Designed to exploit mean reversion. Investors tend to overreact to the low chance of a high-loss event (loss aversion). Longer-term investors can exploit this risk premium. Value factors help identify company stocks that are priced cheaply due to investors being overly cautious about recent market conditions2.

- Momentum: Designed to exploit investor anchoring and adjustment bias—two behaviours that typically result in medium-horizon trends. We seek to capitalise on this anomaly by measuring a variety of trends such as earnings growth and share-price performance3.

- Stability: Designed to exploit investors’ tendency to underestimate the compound-return benefits of investments that provide stable earnings over the long-term. These stocks are also often unloved and considered boring as short-term investors seek more immediate stock-market outperformance. We identify higher-quality business models, income statements and balance sheets, with strong interest-rate coverage and generally high solvency4.

Each primary factor family represents a set of more narrowly-defined factors, or sub-factors, that we combine into factor composites. We measure the presence of these factors in the stocks that make up our investment universe by using a series of corresponding metrics. Exhibit 3 connects the primary factors with their causal behaviours, linking both to the composites and metrics we employ to systematise our strategy.

A globally diversified approach to factor investing

Factor performance is sensitive to market developments and cyclical pressures because of its exposure to varying macro and behavioural forces. For example, between 2000 and 2007, value’s market sensitivity (beta) shifted from defensive (low beta) to highly cyclical (high beta). By the end of this period, investor performance-chasing attracted so much attention to value-oriented strategies that the expected compensation for taking additional cyclical exposure eroded—right before the bear market began in 2008. In the later years of the recent bull market, investors were directing their tendency to chase performance toward stability- and momentum-oriented strategies, again without consideration of the potential consequences.

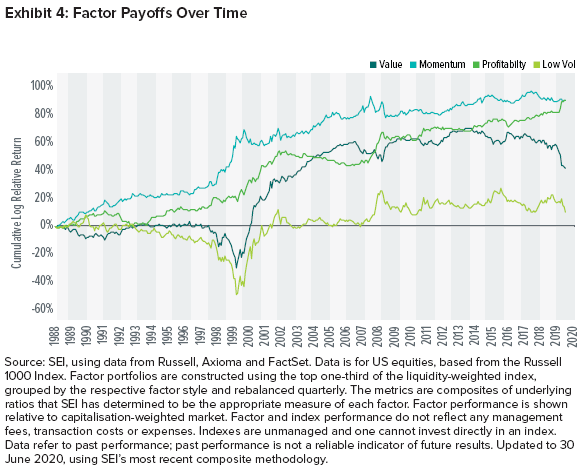

Exhibit 4 depicts the changing favourability of the primary factor families across major developed equity markets over time. This volatility reinforces the merits of global diversification, which remains as integral to successful outcomes in factor investment strategies as it does in traditional approaches. SEI believes a well-constructed factor investment strategy should seek to balance the contributions to expected returns from each factor so that they are approximately equal.

SEI’s approach to factor investing and our competitive strengths

Assessing the investment universe through a factor-based framework is familiar territory for SEI. Factors have been a core component of our active investment-manager evaluation structure for more than 25 years. This has provided us with a broad foundation for understanding how to effectively identify and manage factor exposures in a portfolio. In fact, our views on factor positioning are essentially identical across directly-managed and multi-manager implementations.

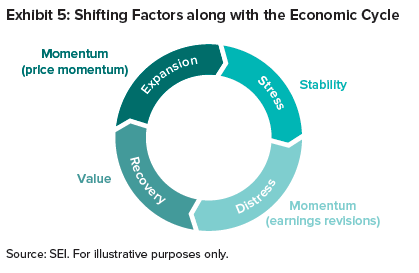

Exhibit 5 provides a high-level reference for changes in factor favourability as the economic cycle progresses through different stages. We believe forward-looking investment strategies that shift portfolio weights dynamically among factors provide the framework necessary to capitalise on the available opportunity-set. SEI conducts factor-specific scenario analyses to measure performance across economic cycles, which helps inform the timing and sizing of our factor allocation decisions.

In 2004, we believe SEI served as a factor-based pioneer when we introduced our managed volatility strategies—the first of their kind, we believe—seeking to capitalise on some of the inefficiencies described above in the stability factor composite. As at 30 June 2020, we oversee more than $3 billion in managed-factor strategies.

Traditional passive products typically rely on market capitalisation to dictate index construction. Factor investing employs a combination of metrics, each tied to a particular sub-factor for which our analysis provides ever-evolving weighting guidance. We recognise the appeal of systematic, rules-based strategies to investors who prefer passive implementations, as they provide transparency and typically come with lower costs than active strategies. Factor investing offers both features, while also retaining the potential for excess returns.

With these benefits in mind, SEI believes incorporating factor investment strategies into traditional equity implementations could help improve long-term risk-adjusted returns.

Global Equity Factor Allocation at a Glance (as at 30 June 2020)

Investment Universe

- Approximately 6,000 global stocks

- Benchmark = MSCI World Index

Multi-Factor Scoring

- Employs multiple measures to assess value, stability and momentum

- Weighted strategically in accordance with the strategy’s long-term risk-return profile

Active Allocation

- Factor allocations are adjusted dynamically in an effort to capitalize on current market environment

Portfolio

- Approximately 300 to 600 stocks

- No large single-stock holdings

- Customised risk models

- Designed to complement other investment approaches

- Implemented efficiently

Important Information

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited (SIEL) acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global Limited, an affiliate of the distributor. SEI Investments (Europe) Limited utilises the SEI Funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI Funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application must be made solely on the basis of the information contained in the Prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs.) A copy of the Prospectus can be obtained by contacting your Financial Advisor, SEI Relationship Manager or by using the contact details shown below.

Data refers to past performance. Past performance is not a reliable indicator of future results. Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Returns may increase or decrease as a result of currency fluctuations. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

In addition to the usual risks associated with investing, the following risks may apply: Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments, securities focusing on a single country, and investments in smaller companies typically exhibit higher volatility.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice.

This information is issued by SEI Investments (Europe) Limited (SIEL) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).

SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.