Factor Investing in the Emerging Markets

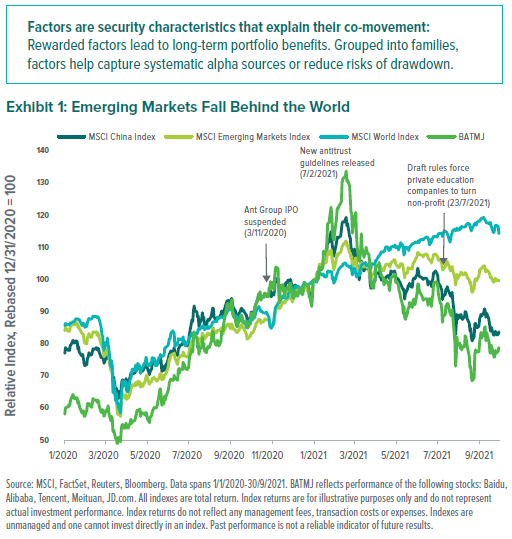

Recent regulatory changes in China focused on global tax optimization, data collection and natural monopolies have created headwinds for equities within the country. As seen in Exhibit 1, the sudden manner in which these changes were launched was disruptive to the entire emerging-market region, especially China. The MSCI China Index, which is heavily weighted in large technology names and makes up a significant percentage of the MSCI Emerging Markets Index, was down over 20% for the year-to-date as of September 30, 2021. The BATMJ stocks (an acronym used to refer to the five largest tech companies in China)—Baidu, Alibaba, Tencent, Meituan and JD.com)—were hit hardest. The decline was mostly in response to the potential impact that recent and future regulations could have on economic growth.

The bulk of the selloff happened over the past six months as China’s government turned most of the nation’s for-profit tutoring firms into non-profits. Investors seemed to be particularly surprised by how quickly the changes unfolded and the eventual scale of their impact. We think a structural shift in the market seems imminent and that it should serve as a clear wakeup call to investors regarding the regulatory risks of investing in the country.

Factor investing in emerging markets

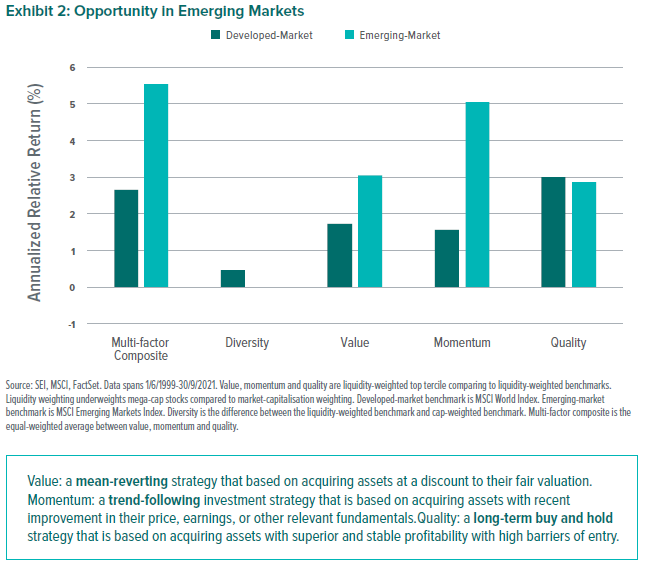

We believe that the emerging-markets asset class can provide opportunities for skilled investors due to pockets of inefficiency that tend to be present. Emerging markets generally lack some of the transparency of more developed markets and are therefore more likely to present opportunities for active management. As seen in Exhibit 2, factor investing in emerging markets has outperformed similar strategies in developed markets over the last 20 years.

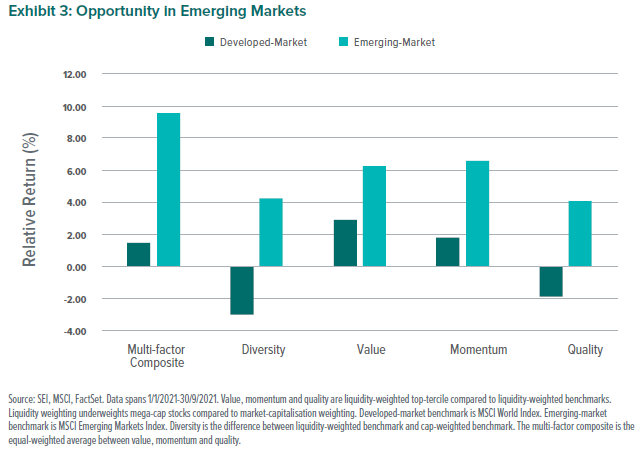

As shown in Exhibit 3, value, momentum and quality have performed well in the year to date through 30 September 2021, and exceeded their long-term return averages. Both diversity (underweight mega caps) and a multi-factor approach have also benefited.

Our Portfolio

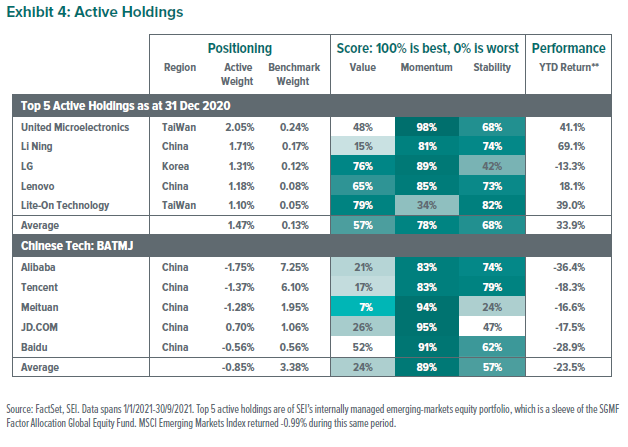

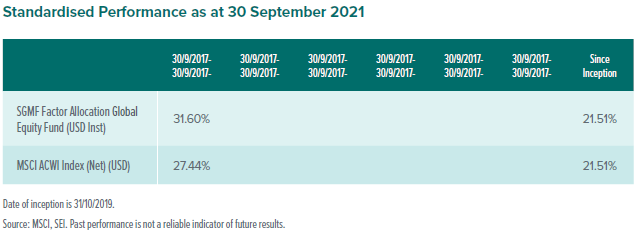

Exhibit 4 looks at the top holdings in SEI’s internally managed emerging-markets equity strategy, which is a sleeve of the SGMF Factor Allocation Global Equity Fund. The strategy has performed well for the year to date, outperforming its MSCI Emerging Markets Index benchmark by 7.6%, in line with the alpha style performance.

As current market leadership broadens beyond large-capitalisation technology stocks, the market should once again punish complacency and reward active stock selection. While passive flows create a high concentration of stocks that are more richly priced than their estimated fair value, our actively managed strategies are designed to capitalise on long-term drivers of market performance through their exposure to value, momentum and stability. The long-term viability of these alpha sources has been proven out by years of academic research.

The active holdings in our internally managed emerging-market equity strategies are generally underweight expensive technology names with high momentum scores. The portfolio is also more balanced and diverse than its benchmark.

Fundamentally, a portfolio that owns cheap, high-quality stocks should naturally enjoy a higher “safety margin” and be able to navigate through a period of changing market dynamics better than a portfolio owning expensive, low-quality names. This is even more important when investors face a market with less efficiency but also greater corporate governance risks.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.