Factor Investing: A Cost-Efficient Alternative to Traditional Approaches

In 1976, the first index fund was launched. Today, a staggering one-third of European equity funds are passively managed. Nearly half of all equity funds in Asia and the US passively mirror an index.1 As passive investing has risen in popularity amid the longest bull market in history2, active managers—the driving force behind market efficiency (that is, share pricing that accurately reflects available information)—are on their way to becoming the minority.

But investors have options outside of these traditional investment approaches. Modern technology and data offer new ways to invest in a cost-efficient manner without relying on active trading to ensure price efficiency. Factor investing is one of those alternatives.

Better rules

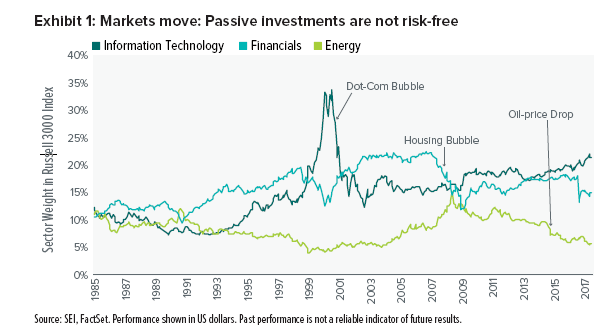

Factor investing is a simple, rules-based and transparent approach to building portfolios that provides consistent exposure to characteristics that have historically been associated with excess risk-adjusted returns.3 Traditional capitalisation-weighted indexes—and the passive investment vehicles that replicate them—have a single rule: The bigger the capitalisation size, the better. As share prices of successful (or overpriced) companies appreciate, their weights are automatically increased in the index. Out-of-favour, low-priced stocks are relegated to the bottom of the list. As such, market bubbles (that is, when prices of stocks within a certain sector like technology, for example, are dramatically inflated) inevitably acquire prominent status, while underpriced companies are underweighted in the index and, therefore, passive funds. Buying high and selling low is not typically a winning strategy. With the growing scarcity of active managers to ensure that share prices reflect available information (the market efficiency mentioned earlier), those bubbles are harder to foresee.

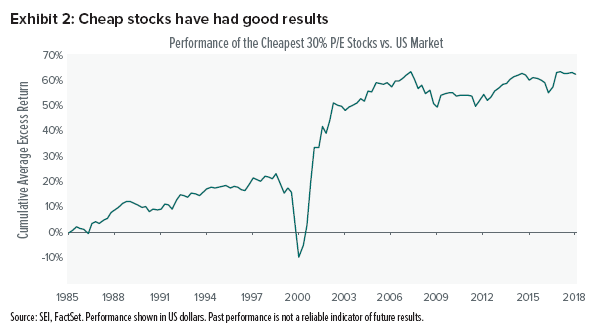

Some rules are better than others. If “buying high” is not a winning strategy, doing the opposite may work. Allocating a larger weight to companies with lower price-to-earnings (P/E) ratios—or, perhaps, to those that are more profitable—are just a few examples of such potentially “better” rules of building portfolios (rather than those based on size alone).

Consider the P/E ratio of a security (a “factor” in investment geek talk). By consistently buying the lowest-priced stocks (as measured by the P/E ratio) in the US market,4 we are not only able to steer away from the most prominent bubbles of the last three decades but also realise returns that typically exceed those of the traditional capitalisation-weighted index.

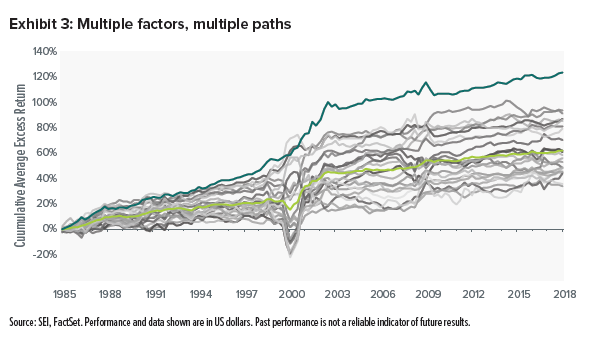

Relying on just one rule—even a good one, like not putting all your eggs in one basket—would be foolish, of course. Through review and validation of academic research and best practices amongst active investment management firms, we are able to collate a myriad of indicators (factors)—such as low P/E or high profit margins—that are both time- and science-tested to have shown better returns or lower risks. As Exhibit 3 shows, multiple factors don’t all work well at the same time; and yes, there are periods when they don’t work at all.

Most importantly, we use unemotional computers (albeit with humans watching over them) to crunch the data, rank the stocks and optimise portfolios to balance risk and return while reducing the transaction costs of managing it all.

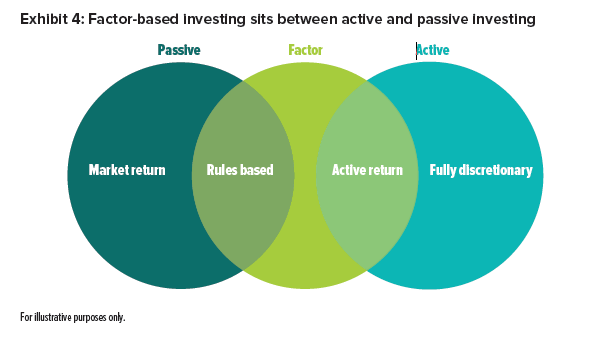

This approach has qualities of both traditional passive and active management. Factor investing, similar to passive investing, is rules-based and cost-efficient. And, like active investing, it seeks to allocate assets to the factors that have historically provided excess return (Exhibit 4).

Why now? Evolution.

The concept of unemotional, rules-based investing has existed since the 1930s, promoted by Columbia Business School professors Benjamin Graham and David L. Dodd. For the investment geeks amongst us, Graham’s 1949 book The Intelligent Investor describes how factors can be easily mapped to value, quality or momentum factor families. For example, it says:

- To capture quality, focus on companies with total debt-to-current-assets ratios of less than 1.10.

- To capture momentum, focus on companies with positive earnings-per-share growth in the last five years with no earnings deficits.

- To capture value, focus on companies with P/E per-share ratios of 9.0 or less.

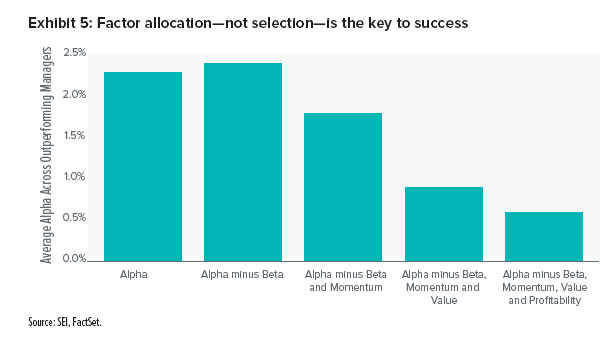

Today, we have better technology to deploy when applying such rules to investing. We also better understand the sources of active manager outperformance. In Exhibit 5, we analyse outperforming managers in the US market.

It turns out that success (remember, we are only looking at outperforming managers here) is mostly a function of exposure to favourable characteristics (factors) and, to a much smaller extent, specific stock selection.

This should not be a surprise. It agrees with our 1986 research by Gary Brinson and Gilbert Beebower about the dominance of allocation as a determinant of success. Stock selection has its place, and skilful active managers should be able to deliver stock-specific excess returns. However, factor allocation should be able to leverage modern technology and science to provide access to attractive areas of the market in a cost-efficient manner.

About the SEI Factor Allocation Global Equity Fund

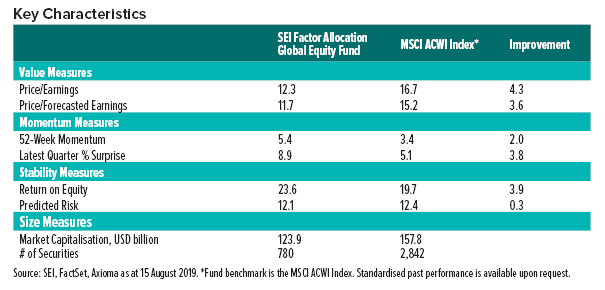

The SEI Factor Allocation Global Equity Fund (the Fund) seeks long-term growth of capital and income through investment in a broadly diversified portfolio of global equity securities. The Fund’s base currency is US dollars. It launched as at 14 August 2019.

The Fund invests directly in equity securities using a model-based approach in facilitating investment decisions, taking into account environmental, social and governance factors. It categorises and selects securities based on certain characteristics (factors), such as volatility, value, size or share-price performance. Based on market opportunities and at the Fund’s discretion, we may tilt its factor exposures by changing its allocation to the factors.

Background

SEIGL is part of the SEI Investments Company (SEI) group of companies, which was founded in 1968 and is headquartered in Oaks, Pennsylvania. SEI Investments Management Corporation (SIMC) is the investment advisory arm and wholly-owned subsidiary of SEI. As at 30 June 2019, through its subsidiaries and partnerships in which the company has a significant interest, SEI manages, advises or administers $970 billion in hedge, private equity, mutual fund and pooled or separately managed assets, including $335 billion in assets under management and $630 billion in client assets under administration. For more information, visit seic.com.

Glossary

Alpha source: Alpha source is a term used by SEI as part of our internal classification system to categorise and evaluate investment managers in order to build diversified fund portfolios. An alpha source is the investment approach taken by an active investment manager in an effort to generate excess returns. Another way to define an alpha source is that it is the inefficiency that an active investment manager seeks to exploit in order to add value.

Momentum: Momentum stocks are those whose prices are expected to keep moving in the same direction (either up or down) and are not likely to change direction in the short-term.

Price-to-earnings ratio: Price-to-earnings ratio is the ratio of a company’s share price to its earnings over the past 12 months, which can be is used to help determine whether a stock is undervalued or overvalued.

Quantitative: Quantitative analysis is based on computer-driven models.

Value: Value stocks are those that are considered to be cheap and are trading for less than they are worth.

Important Information

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the ”SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may only be marketed to the general public in the United Kingdom.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Any reference in this document to any SEI funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI fund are reminded that any such application must be made solely on the basis of the information contained in the prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs.) A copy of the prospectus can be obtained by contacting your financial adviser, SEI relationship manager or by using the contact details shown below.

Data refers to past performance. Past performance is not a reliable indicator of future results. Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Returns may increase or decrease as a result of currency fluctuations. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

In addition to the usual risks associated with investing, the following risks may apply: Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments, securities focusing on a single country, and investments in smaller companies typically exhibit higher volatility.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice. This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).