Evergrande: How Large is the Anticipated Fallout?

Investors have recently grown unsettled by the misfortunes mounting against Evergrande, one of China’s largest real estate developers. Evergrande has accumulated roughly $300 billion in debt primarily by borrowing to fund new domestic construction projects.

How did Evergrande’s situation grow so dire?

The People’s Republic of China introduced limits last year on the pace at which developers would be allowed to accumulate debt. These new regulations were intended to moderate a sharp debt-fuelled rebound in the Chinese real estate market following the country’s early first wave of COVID-19.

New limitations on borrowing, coupled with aggressive pre-sale practices that created a growing pile of unfinished projects, left Evergrande with more obligations than it could realistically afford to accommodate. Several banks began denying mortgages on these unfinished projects in July as Evergrande’s problems became more apparent.

Why has this become such a critical issue now?

Evergrande owes its creditors more than $100 million in interest payments over the next few weeks, and its credit rating was recently downgraded as the possibility of default has increased. As with any debt-centric crisis, default severely limits a debtor’s ability to borrow or refinance, and raises its future borrowing costs, increasing the challenges in an already-strained situation.

The overarching concern among investors centres on how Evergrande’s problems are ultimately resolved. There’s widespread agreement that the company’s debt load is unmanageable, but whether it tumbles into a disorderly bankruptcy, undergoes an orderly restructuring, or gets bailed out by the Chinese government remains to be seen.

Furthermore, is Evergrande’s looming default a symptom of a systemic problem? If so, is that problem limited to China, or could it have a significant international impact?

SEI’s View

We’ll address the most acute concern first: Evergrande does not appear to pose significant risk outside of China since it isn’t globally interconnected on anything remotely close to a Lehman Brothers scale. Foreign investor exposure is mostly limited to Evergrande’s $18 billion in foreign-currency bonds, which is certainly not enough to ignite a global systemic crisis.

The most likely outcome would be an orderly restructuring of Evergrande’s debts and unfinished projects rather than an unmanaged collapse or a government-backed bailout. State-backed media has cautioned that creditors shouldn’t expect to be made whole, however, and priority in restructuring is expected to be given to homebuyers, so there may well be steep enough creditor losses to push some of them into default.

Fortunately, a default on Evergrande’s unsecured debts would only dent China’s system-wide bank reserves, and a restructuring with a measure of Chinese government support would alleviate at least some of the pain to creditors.

We also believe President Xi Jinping is not going to sit idly by if a broader panic begins to pose a threat. The People’s Republic of China’s wide-ranging reforms this summer are already stressing the country, and Xi has the tools and power to put the necessary backstops in place if Evergrande appears poised to tip into a systemic threat. Evergrande certainly has company in terms of developers with high leverage and pre-sale practices, so it’s possible these developers and some of their creditors could encounter similar challenges.

There’s already evidence that the People’s Bank of China (PBOC) will lean into accommodation to help offset tighter financial conditions. China’s central bank began to ease its Reserve Requirement Ratio in July when Evergrande’s problems first reached a boil after remaining notably restrained compared to other major central banks throughout most of the pandemic. We expect a more active role for the PBOC if warranted by deteriorating domestic financial conditions.

We have historically not been great fans of Chinese markets due to their lack of transparency. If China’s over-indebted developers actually resulted in a round of bankruptcies it would be taken as a sign of healthy progress in the Chinese market’s development.

Beyond the immediate concerns associated with Evergrande, China’s recent struggles with the delta variant, tech-centred crackdowns, and now the property sector will likely shave a bit off of global growth at the margin. The size of China’s real estate sector is large enough that we can’t overlook the risk of a reverse wealth effect on the Chinese and global economies.

Other countries, like India, and the broader emerging Asia region, have recently benefitted from improving vaccination figures and will need to pick up the slack. Despite these concerns and general worries over “peak growth” we believe the outlook for global corporate earnings remains solid.

Longer term, however, China’s demographics are an important risk to its real estate sector and economic growth in general. While not identical, there are similarities between China’s emerging predicament and the end of Japan’s expansion in the late 1980s—specifically, a deteriorating demographic outlook against the backdrop of a highly levered property sector.

Most of the difficulties associated with that episode were largely confined to Japan, but they took a long time to work through.

It is also worth noting that Evergrande is not the only concern on the horizon. Equity markets have not sold off in a notable way for quite some time. The anticipated tapering of asset purchases by the U.S. Federal Reserve and the possibility of lingering heightened inflation are just as likely to serve as catalysts for a pullback as debt problems in China’s real estate sector.

Our Strategies1

We have no direct exposure to Evergrande in any of our investment strategies.

With regard to indirect exposures, our emerging-market equity strategy is underweight China (including Hong Kong) by more than 4% compared to the benchmark’s 33.8% allocation. The Chinese financials sector is underweight, representing an allocation of slightly more than 4% of portfolio value, while Chinese real estate is a bit more than 1% of the portfolio (in-line with the benchmark).

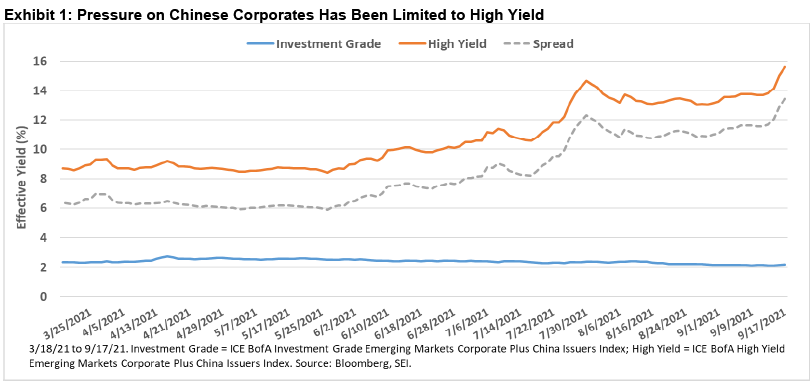

China represents an even smaller exposure within our emerging-market debt strategy (4.7% of portfolio value versus the benchmark’s 5.84%). Moreover, 99% of the portfolio’s China-issued holdings are rated investment grade by Moody’s. Exhibit 1 on the next page makes clear that the fears of bond defaults have been limited to high yield, where yields have climbed sharply since the spring, while investment-grade yields have actually declined in recent months.

Only 0.2% of the portfolio’s value is held in Chinese bonds that are not government issued, none of which is composed of Chinese real-estate bonds. We are also underweight Hong Kong, and our entire exposure there totals about 0.15% of the portfolio’s value.

Elsewhere, we have underweight exposure to Chinese bonds in our global opportunistic fixed income strategy. 99.7% of the portfolio’s China-issued holdings are rated investment grade by Moody’s.

Glossary of Financial Terms

Global systemic crisis: A global systemic crisis refers to a scenario in which failures in the financial system cross international borders.

Leverage: Leverage refers to the degree to which a company uses borrowed money to finance activities.

Real-estate bonds: Real-estate bonds refer to fixed-interest securities issued by companies in the real-estate sector.

Tapering: Tapering, in the context of central bank policy, refers to a gradual reduction in the scale of periodic asset purchases.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-interest investment.

Index Definitions

The ICE BofA High Yield Emerging Markets Corporate Plus China Issuers Index is composed of bonds issued in China by non-sovereign issuers that are rated below investment grade.

The ICE BofA Investment Grade Emerging Markets Corporate Plus China Issuers Index is composed of bonds issued in China by non-sovereign issuers that are rated investment grade.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Diversification may not protect against market risk. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”).

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.