Emerging-Market Tech Stocks Upstage FAANGs

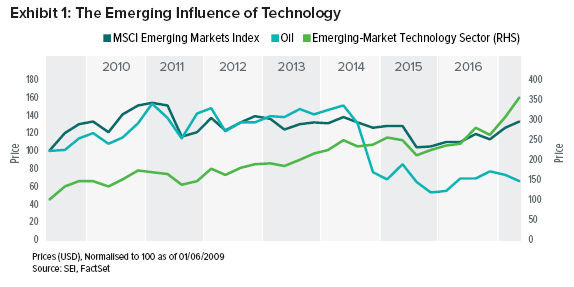

Twenty years ago, the MSCI Emerging Markets Index was made up of companies from a variety of sectors and countries that were traditionally associated with commodities and infrastructure. As a result, its performance closely tracked the price of oil. This all began to change in 2014, as oil prices trended sharply lower—and the Index began to more closely follow information technology shares as those companies grew in importance (Exhibit 1).

The recent outperformance of emerging-market technology companies points to the fact that technology is now the largest sector in the Index—and that top contributors to a given index tend to be from the same sector (while the opposite also typically holds true, as the biggest detractors during market declines usually fall within a single group.)

Tech Rises in Asia

Much has been made about the influence of the technology sector on US markets over the last several years—and understandably so, considering the so-called FAANG stocks (Facebook, Apple, Amazon, Netflix and Google) occupy about 9% of the Russell 1000 Index (US large-cap index) as of 30 June, 2017.

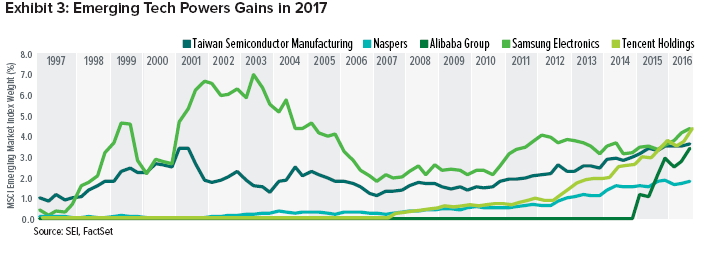

Yet the technology sector has gained an even greater presence within emerging markets. Over the past 20 years, technology companies went from comprising just 1.5% of the MSCI Emerging Markets Index market capitalization in 1997 to nearly 27% as of 30 June 2017. The top-five market-capitalization-weighted stocks in the Index are technology companies Samsung, Alibaba, Naspers, Tencent and Taiwan Semiconductor. Collectively, they make up nearly 18% of the Index. By comparison, in 1997, the top-five stocks by market capitalization were a mix of telecommunications and utilities companies that occupied just 10.5% of the Index.

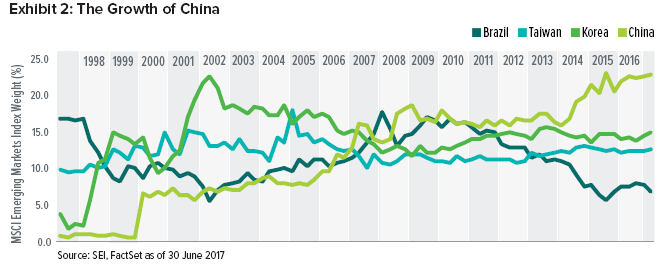

The MSCI Emerging Markets Index has also undergone a big transformation in geographical terms.

Driven by the growing importance of China in the index, it is now dominated by Asian countries (Exhibit 2). This reflects the rise of China’s economy, as well as the expanding reliance on internet usage across the globe. China’s weight in the Index is expected to continue to grow along with the gradual increase of the country’s renminbi-denominated A share stocks.

IT Drives Gains

Investors in both US and emerging markets who avoided technology stocks in the first half of 2017 would have struggled to keep up with the performance of the benchmark indexes. But the consequences were even greater for those who failed to invest in the largest five emerging-market tech stocks, with a resulting 32% loss of the MSCI Emerging Market Index’s overall return (in US dollars)—compared to a 21% loss of the Russell 1000 Index’s overall return driven by lack of exposure to US FAANG stocks. Exhibit 3 highlights the growing importance of selected emerging-market technology stocks through the first half of 2017.

SEI’s View

We believe emerging-market stocks offer compelling opportunities; their valuations have grown increasingly attractive compared to recent history and relative to those of developed markets, partly due to moderate global economic growth and a weakening US dollar—two trends we expect to continue.

Of course, it is important to remember that we cannot expect market movements to trend in the same direction forever. While technology stocks have taken the reins in terms of driving overall performance, at least for the time being, investors cannot count on a single group or sector to endlessly dominate benchmark performance. We believe diversification remains a prudent approach to investing—perhaps even more so in times when gains are driven by a highly concentrated group of sectors or securities.

The increased weight of the technology sector in the MSCI Emerging Markets Index is not the only cause of its enhanced influence. Another factor has been the expanding availability of emerging-market exchange-traded funds, or ETFs, which are designed to offer investors passive exposure to emerging-market companies. Because inflows into ETFs reward stocks in proportion with their weights, the top-five stocks concentrated in technology names have benefitted most—and therefore have had the largest effect on Index performance.

Definitions

Market Capitalization: Market capitalization refers to the total value of a company’s outstanding shares.

Important Information

Securities mentioned may be holdings of SEI Funds. Holdings are subject to change.

Diversification does not guarantee against a loss. Products of companies in which technology funds invest may be subject to severe competition and rapid obsolescence.

Past performance is not an indicator of future performance.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from Factset, Lipper, and BlackRock, unless otherwise stated.