Does the Presidential Election Move the US Stock Market?

Election year in the US is heating up. One common campaign promise from both parties is a soaring economy—which investors hope will translate into a rising stock market.

But does the election cycle actually impact investors’ portfolios?

A four-year cycle (and sometimes eight)

Economists and historians alike have attempted to answer this since the mid-twentieth century, leading to the development of the Presidential Election Cycle Theory in the late 1960s. According to historian Yale Hirsch, founder of the Stock Trader’s Almanac, this theory states that US stock market performance follows a predictable four-year pattern that correlates with the American presidential cycle.1

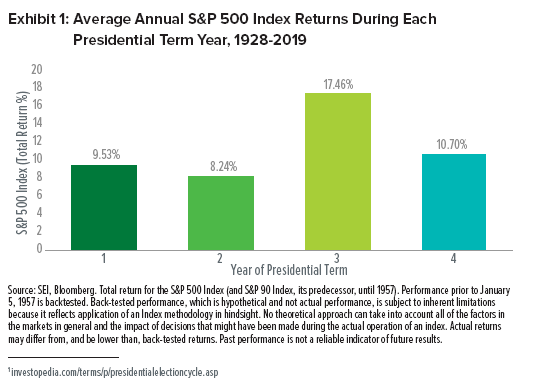

Until the twenty-first century, this theory held mostly true. However, the S&P 500 Index (an unmanaged, market-weighted index that consists of 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market) skyrocketed during the first year of the George W. Bush, Barack Obama and Donald Trump presidencies, as reflected in Exhibit 1.

First is (historically) the worst

Until the first year of President George W. Bush’s first term, investors tended to earn the smallest amount of stock market gains in the year immediately following a presidential election.

Yes, there is often a honeymoon period of optimism among Americans about new leadership that boosts the market. But policymakers under a new presidency may also begin to feel less restrained about introducing programs—some of which could be unpopular or restrictive—such as a tax hike or increased government spending. This may negatively impact business profits and consumers, causing the market to slump.

Second is better, third is best

During Year Two of a presidency, the economy has tended to level out. Year Three of a president’s term has generally been the best, performance-wise, for the US stock market. Researchers believe this is because the incumbent, thinking ahead to re-election, often introduces measures designed to stimulate the economy—to which the market tends to respond favourably. Since 1928, the third year following a election year has been positive for US stocks about 82% of the time.2

Fourth is fine…eighth, not so much

Market performance diverges in the fourth year of a presidential term. Incumbents are often re-elected, which creates less panic in the market compared to Year Eight of a two-term presidency, when markets tend to fall as investors despise uncertainty. Data from S&P Global Market Intelligence shows that since 1944, the S&P 500 Index has only risen 50% of time during the final year of a two-term presidency.3

More compelling may be the US stock market’s influence on the outcome of an election. According to Presidential Election Cycle Theory, the incumbent president has won 87% of the time (and every election since 1984) when the S&P 500 Index has advanced between 31 July and 31 October leading up to Election Day.4 Conversely, when the Index declined during the same period, the challenger unseated the incumbent.

Congress has the most clout

No matter who claims victory in the presidential election, their influence on the stock market is generally limited. US lawmakers, not the President, generally have more direct impact on stock-market performance.

According to Ned Davis Research, a split Congress has the biggest negative influence on US stocks, owing perhaps to term-length differences between the House and the Senate.5 House representatives are re-elected every two years, while senators are re-elected every six. If one political party’s approval rating drops amid economic policy missteps, it does not necessarily mean that it will lose both the House and the Senate simultaneously.

Don’t be bullied by the cycle

It’s easy to get caught up in every little market move. But for long-term investors, a four-year cycle—volatile or otherwise—should not have a lasting effect.

Theories about how the presidential cycle affect the US stock market are just that—best educated guesses. Even academicians and economists don’t always get it right. No matter what phase of the presidential cycle we happen to be in—or which candidate wins the election—stay focused on long-term goals and resist the urge to react.

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

This information is made available in Latin America by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.