Diversity, equity, and inclusion in asset management: Necessary measures for progress.

Diversity, equity, and inclusion (DEI) has become a huge focus within the asset management industry due to a general shift in social values—and because there have been few advancements made in the space. One of the key challenges in making advances is lack of data and disclosure within the industry.

In this paper, we look at industry data to draw observations and perspectives on:

- the state of DEI in the asset management industry

- implications for asset owners in general

- what this means for SEI and our clients given our underlying investment philosophy and process

- and what may lie ahead for the industry.

Coming into focus: Industry efforts accelerating.

Industry-related professional organizations have begun to take action on DEI issues.

Among the biggest indicators of just how seriously the investment industry has become about diversifying its intellectual capital is the CFA Institute’s publication of its Diversity, Equity & Inclusion Code (USA & Canada) in 2021, outlining a set of standards to improve diversity within the industry.

Another sign of heightened focus on diversity is the formation of the Institutional Investing Diversity Cooperative (IIDC), where SEI is a founding member. IIDC comprises a group of more than 25 institutional investment organizations that pledged to promote greater diversity in the industry by advocating for access to representative ownership and investment professional data.1 SEI additionally supports external programs such as Stepping Stones (which aims to empower underserved youth in the U.S. by providing positive adult role models, leadership experiences and skills necessary for success<sup>2</sup>) and 10,000 Black Interns (which extends opportunities to young black people for paid professional experiences in order to improve representation across sectors<sup>3</sup>).

The growing industry attention on DEI has caused investment consultants and wealth-management platforms to launch diversity initiatives that promote certain quotas or hiring efforts, targeting specifically sub advisors or money managers. Large institutional investors such as the Ford Foundation have committed capital to underrepresented or “emerging” managers.<sup>4</sup>

At SEI, we incorporate diversity into our own research process, with a focus on cognitive diversity (different ways of thinking) and the benefits it brings to decision making—a critical component of portfolio management. In our Diversity and Inclusion in SEI’s Manager Research Process paper, written in August 2021, we outline how we do this.

In order for diversity in the industry to truly improve, we believe that DEI needs to be addressed specifically and with intent.

CFA Institute’s Diversity, Equity & Inclusion Code (USA & Canada)

Principle 1: Pipeline

We commit to expanding the diverse talent pipeline.

Principle 2: Talent Acquisition

We commit to designing, implementing, and maintaining inclusive and equitable hiring a nd onboarding practices.

Principle 3: Promotion and Retention

We commit to designing, implementing, and maintaining inclusive and equitable promotion and retention practices to reduce barriers to progress.

Principle 4: Leadership

We commit to using our position and voice to promote DEI and improve DEI outcomes in the investment industry. We will hold ourselves responsible for our firm’s progress.

Principle 5: Influence

We commit to using our role, position, and voice to promote and increase measurable DEI results in the investment industry.

Principle 6: Measurement

We commit to measuring and reporting on our progress in driving better DEI results within our firm. We will provide regular reporting on our firm’s DEI metrics to our senior management, our board, and CFA Institute.

How do you measure DEI?

Now that industry standards are being promoted and organizations have taken action to improve DEI, the question is how to accurately measure progress. One of the challenges in doing so is that the types of data used to track diversity and inclusion are self-reported by investment managers on a voluntary basis.

For this paper, we analyzed manager data from eVestment, a global provider of institutional investment data, which started collecting diversity data on January 4, 2021.

Our analysis covered the following asset classes as of November 18, 2021<sup>5</sup>:

- Equity: U.S. large cap; U.S. small and small/mid-cap; global; developed markets excluding the U.S.; and emerging markets

- Fixed income: U.S.; global; emerging markets; and municipal

Looking at the proportion of diverse individuals (women and/or racial/ethnic minority) in leadership roles, we classified firm ownership and portfolio management teams as one of the following:

- Majority (>=51% diverse individuals)

- Significant minority (50%-21% diverse individuals)

- Minority (<=20% diverse individuals)

Race and ethnic data for minorities from eVestment encompass the following categories:

- Black

- Asian

- Hispanic/Latino/Spanish

- North Africa/Middle East

- Multi-race

What did we find?

Broader organizational diversity information (such as executive team, board of directors, or workforce composition) isn’t widely or consistently disclosed. In some geographies, reporting certain types of diversity information is prohibited by law.

We also discovered that firms offering equity products had better disclosure rates than firms offering fixed-income products, by approximately 10%.

Consequently, we do not have a full picture of DEI in asset management. While limited, diversity data is far more widely reported at the firm level than at the product level—which appears to have important implications.

Firm-level revelations

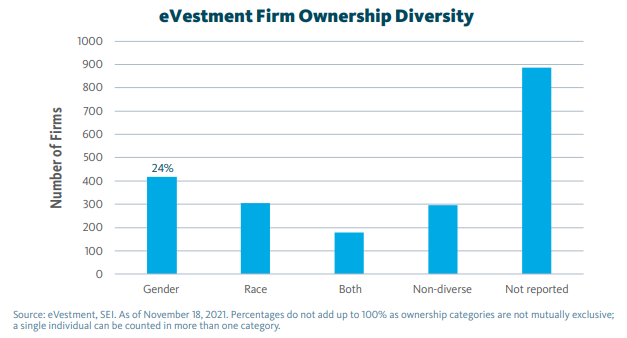

There are 1,737 firms that offer actively managed, open equity and/or fixed-income products with eVestment universe classifications as of November 2021.

Of these, a notable 887—more than half—did not report gender or race/ethnic ownership data. A closer look revealed that:

- 177 (20%) of those 887 non-reporting firms are publicly listed (or majority-owned by a publicly listed parent company) and simply cannot report such information as they do not know the racial or gender mix of their shareholders.

- An even larger portion—281 (32%) out of the 887 non-reporting firms—are 100% employee-owned that have thus far chosen to not report DEI ownership data despite having access to such information.

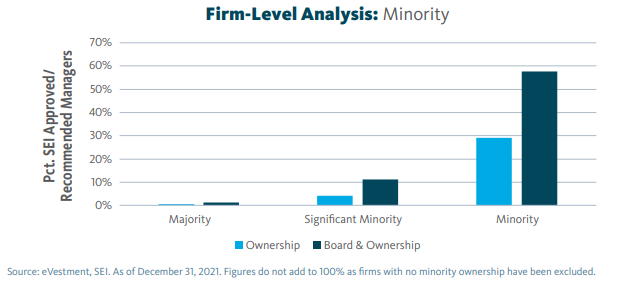

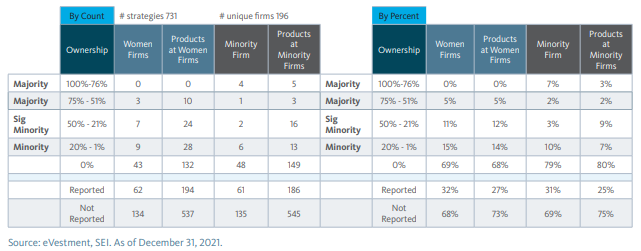

Based on the information that we do have, overall ownership diversity at the firm level looks as follows:

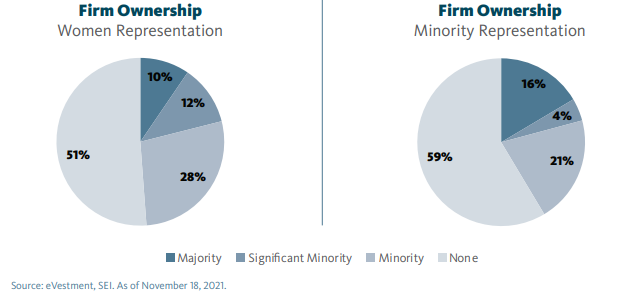

Digging a bit deeper into ownership representation across the 850 firms that report DEI data, we found the following:

Much of the effort that the industry puts forth to support diversity does not treat women and minorities as distinct areas of focus. Typically, they are regarded interchangeably, with improved representation of either group (or a combination of the two) accepted as meeting a diversity goal.

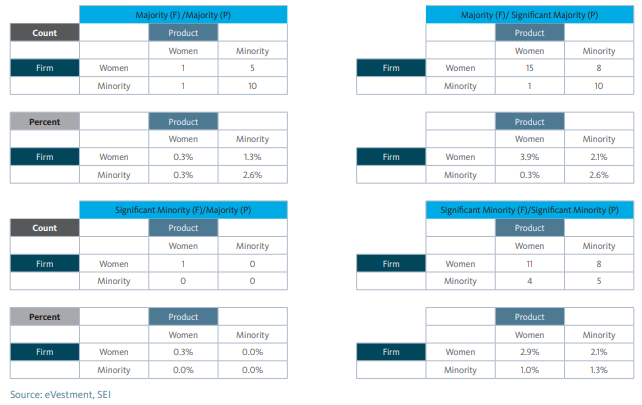

It is therefore no surprise that, based on the available data, there are remarkably few options for asset owners looking to invest in products offered by firms with ownership diversity at both the gender and race/ethnicity level:

- Only 17 out of the 850 reporting firms (2%) are majority-owned by both women and minorities.

- The opportunity set expands to 25 firms when the focus shifts to those with significant minority ownership by both groups.

- When relaxing the constraint to include firms that have either significant minority ownership or majority ownership by women and minorities, the total number of eligible firms jumps to 44—meaning a mere 5% of the 850 reporting firms offer some meaningful combination of women/minority ownership (comprising at least 21%).

In addition to representational statistics, firms provided information on policies they have in place to promote diversity, support mentorship, and undertake pay assessment. Out of the 1,737 firms in the eVestment universe, we found the following:

- 607 (35%) have at least some policies to promote diversity in recruitment, workforce leadership and/or board representation.

- 324 (19%) offer mentorship programs.

- 219 (13%) have undertaken gender or race/ethnic pay-gap studies.

- 224 (13%) use key performance indicators to track diversity efforts (only half of those make that information public).

Interestingly, if we narrow the universe of firms down to those with significant minority or majority women/ minority ownership, the percentage with policies in place to promote diversity actually decreases slightly to 28% (compared to 35% of all reporting firms).

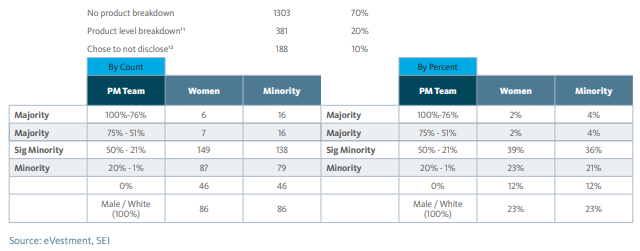

Product-level revelations

Across all eVestment-universe-classified equity and fixed-income products (14,484), less than 20% have disclosed diversity information. Recency of reporting suggests that early responders are those who have been tracking diversity data for some time and are likely to be those with diverse teams who care about such statistics. Therefore, current data are unlikely to be representative of the industry.

With that in mind, we found the following diversity data at the product level for equity and fixed income:

Equity

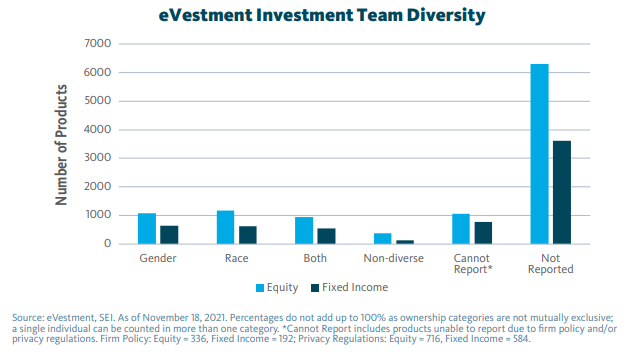

Across all active, open and eVestment-universe-classified equity products (9,216):

- Only 1,671 (18%) reported diversity statistics for the entire portfolio management team.

- 1,057 products (11%) were denoted by firms as being unable to report due to firm policy or privacy regulations for individuals in specific geographic locations.

- This left about 70% of products not addressed at all by firms.

Fixed income

Across all active, open and eVestment-universe-classified fixed-income products (5,268):

- Only 851 (16%) reported diversity statistics for the entire portfolio management team.

- 776 products (15%) were denoted by firms as being unable to report due to firm policy or privacy regulations for individuals in specific geographic locations.

- This left around 70% of products not addressed at all by firms.

The overall picture of diversity at the product level looks as follows:

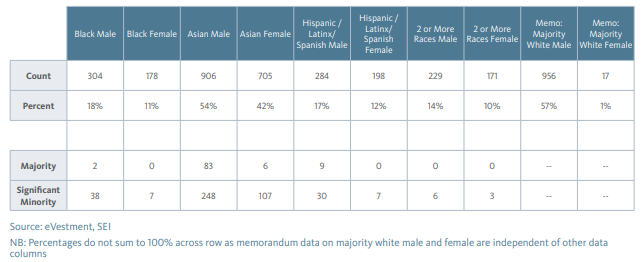

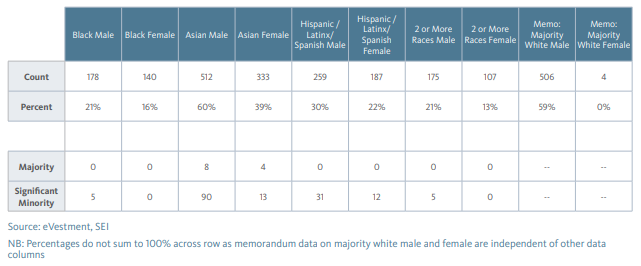

A closer look at the product-level data shows that:

- The best-represented minority racial group is Asian by a substantial margin for both males and females overall as well as at the majority and significant-minority levels.

- Disparity in female representation exists in all race/ethnic categories. Even white women—who have by far the largest percentage of representation compared to females in other racial/ethnic groups—are dramatically underrepresented relative to white males. It is particularly notable at the majority and significant-minority level; nearly 60% of products are managed by teams that are majority white male, while only 1% of products are managed by teams that are majority white female.

- While noticeable disparities exist, an encouraging 69% of all equity and fixed-income products (1,735 out of 2,522 reporting) have at least some percentage of female participants (minority or better).

- 100% of white male or female teams show a skew between equity and fixed income. Equity tends to run between high 20s and low teens across equity universes evaluated, while fixed income runs 10% or less across fixed income universes evaluated.

- We did not find a bias for women-owned or minority-owned firms (majority or significant minority) to employ more diverse portfolio teams (as majority or significant minority).

What role does DEI play in SEI’s manager research?

We have been tracking engagement with managers on a meeting-by-meeting basis since mid-2015. Such meetings normally entail discussions about the manager’s firm, people, product, and process. Therefore, almost any such engagement would give us the insight necessary to form at least an initial investment opinion and whether we wish to pursue further discussions.

Based on majority or significant minority women-owned firms, since mid-2015 we’ve engaged with 49% of them (87/179) across equity and fixed-income universes in eVestment, and 31% of minority-owned firms (55/177). At the minority ownership level, the figures are 66% (156/236) and 94% (117/125), respectively.

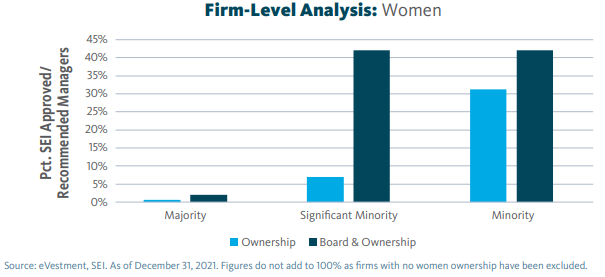

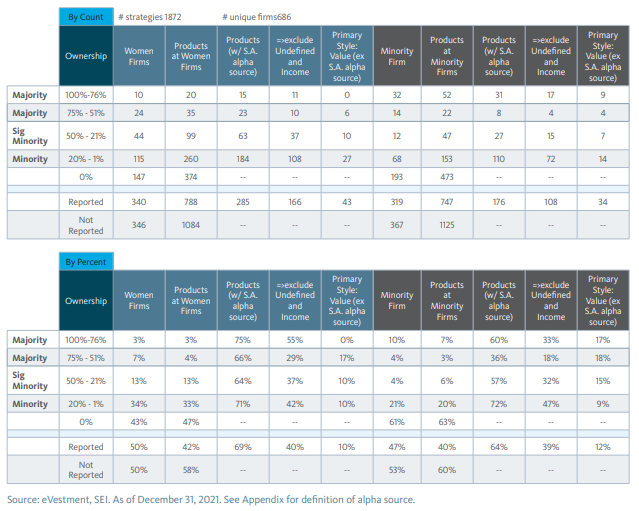

As of December 31, 2021, SEI deploys capital for its clients across 144 Recommended and Approved managers. The denominator is from eVestment data and reflects the numbers of firms meeting the thresholds for minority, significant minority and majority. The distribution of firms based on levels of ownership and Board composition is as follows:

The distribution of those same firms by degree of minority representation in firm ownership and board composition is as follows:

On strictly a firm-ownership level, we can see that SEI’s managers have a generally higher rate of diversity than that of managers in corresponding eVestment universes:

- Almost 40% of SEI’s 144 managers have at least minority ownership by women—compared to just over 21% of the 850 reporting managers in the corresponding eVestment universe.

- Nearly 35% of SEI’s 144 managers have at least minority ownership by minorities—compared to slightly less than 21% of the 850 reporting managers in the corresponding eVestment universe.

When incorporating board diversity data—a surrogate for diverse decision-making at the corporate strategy level when ownership data cannot be reported (our preferred measure)—the representation rates of SEI’s 144 managers jump dramatically higher:

- 86% of SEI’s 144 managers have at least minority representation by women.

- 70% of SEI’s 144 managers have at least minority representation by minorities. At the product level, where we evaluate the portion of women or minority portfolio managers, we found that.

- 20% of the 401 actively-managed Recommended or Approved products on SEI’s platform (excludes internal mandates) have women representation.

- 28% of the 401 active products on SEI’s platform (excludes internal mandates) have minority representation.

- Data from eVestment are not directly comparable as they measure the entire portfolio management team, not just decision-making portfolio managers.

Conclusions: We cannot improve what we cannot measure.

At SEI, we maintain that the more we know about a manager’s products, the better placed we are to include that manager in our searches and due-diligence work. As the CFA Institute notes, “what gets measured gets evaluated and managed, particularly in a data-driven industry such as investment.<sup>”6</sup>

Therefore, we think it crucial that asset owners, consultants, outsourced chief investment officers (OCIOs), and others who allocate capital to asset managers should not only encourage and promote broader reporting and tracking on DEI status, but do the same with regard to programs and initiatives to support and advance DEI efforts (such as talent acquisition, training, retention, and compensation).

With that said, DEI initiatives can result in unintended consequences if not crafted carefully. Simply using quotas to meet targets can lead to improper hires—both in terms of team compatibility and investment skill—while overlooking more qualified non-minority individuals.

The CFA Institute’s DEI Code highlights a wide number of potential initiatives to promote change and advancement, some as early as at the high school level, which we view as more effective alternatives to quota-setting.

At SEI, we believe disclosure and transparency are key supports to effective due diligence, be it diversity and ESG assessment, or portfolio holdings analysis. As such, we intend to continue promoting broader disclosure within the investment community—and position managers on our platform to the extent that they align with SEI’s core investment tenets, which are intended to help achieve our goal of obtaining optimal risk-adjusted returns to meet our clients’ financial objectives.

Seeking greater diversity need not inherently conflict with this goal. However, based on the current state of disclosure and alignment, the opportunity set is not well stocked to widen our platform of recommended managers to any notable degree today.

We plan to address these challenges in our manager engagement program, encouraging greater disclosure and promoting initiations or enhancements of programs that support improving DEI.

Finally, we will continue to meet with minority and women-owned firms as part of our manager due-diligence engagement and, more importantly (given our belief that diversity at the execution level is more crucial than at the ownership level), further our efforts with women- or minority-led portfolio management teams.

Definitions

An alpha source is a term used by SEI as part of our internal classification system to categorize and evaluate investment managers in order to build diversified fund portfolios. An alpha source is the investment approach taken by an active investment manager in an effort to generate excess returns. Another way to define an alpha source is that it is the inefficiency that an active investment manager seeks to exploit in order to add value.

Appendix

EXHIBIT 1

Equity products<sup>7</sup> reporting portfolio management team representation

EXHIBIT 2

Fixed-income products<sup>8</sup> reporting portfolio management team representation

EXHIBIT 3

Firm-level example analysis – Equity (shown here is U.S. all/large cap<sup>9</sup>)

EXHIBIT 4

Firm-level example analysis – Fixed income (shown here is Global Fixed)

EXHIBIT 5

Product-level example analysis - All asset classes (shown here is U.S. all/large cap<sup>10</sup>)

EXHIBIT 6

Product-level example analysis - All asset classes (shown here is U.S. all/large cap<sup>10</sup>)

EXHIBIT 7

Universe details

All equity classes (U.S. large, mid, and small cap; global; developed markets excluding U.S.; and emerging markets)

- Primary investment approach: combined; discretionary; fundamental; quantitative; technical analysts (exclude passive and unlabeled)

- Investment focus: long-only; extended equity; real estate investment trusts (REITs); specialty

- Primary universe: must be classified by eVestment (exclude passive13 and sector)

- Product offered: all vehicles

- Base currency: all

- Status: active

Global fixed income

- Primary investment approach: combined; discretionary; fundamental; quantitative14 (exclude passive and unlabeled)

- Investment focus: aggregate; credit; government; leveraged/bank loans; high yield15; multi-asset fixed income; and securitized

- Primary universe: must be classified by eVestment (exclude passive, money market, convertibles)

- Product offered: all vehicles

- Base currency: all

- Status: active

U.S. fixed income

- Primary investment approach: combined; discretionary; fundamental; quantitative (exclude passive and unlabeled)

- Investment focus: aggregate; credit; government; leveraged16/bank loans; high yield; multi-asset fixed income; securitized

- Primary universe: must be classified by eVestment (exclude passive, money market, convertibles, U.S. Treasury inflation-protected securities, municipal, stable value)

- Product offered: all vehicles

- Base currency: all

- Status: active

Emerging-markets debt

- Primary investment approach: combined; discretionary; fundamental; quantitative (exclude passive and unlabeled)

- Investment focus: local; hard; blend; corporate

- Primary universe: must be classified by eVestment (exclude passive)

- Product offered: all vehicles

- Base currency: all

- Status: active

Municipals

- Primary investment approach: combined; discretionary; fundamental; quantitative (exclude passive and unlabeled)

- Investment focus: all durations; high yield; taxable

- Primary universe: must be classified by eVestment (exclude passive)

- Product offered: all vehicles

- Base currency: all

- Status: active

Important Information

SEI considers DEI factors as part of its Portfolio Manager Research and due diligence process including an evaluation of each Portfolio Manager’s approach to integrating sustainability risk in its investment process; however, no minimum threshold has been established with respect to these capabilities in order for a firm to be hired as a Portfolio Manager.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI). For those SEI products that employ a multi-manager structure, SIMC is responsible for overseeing the managers and recommending their hiring, termination, and replacement.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.