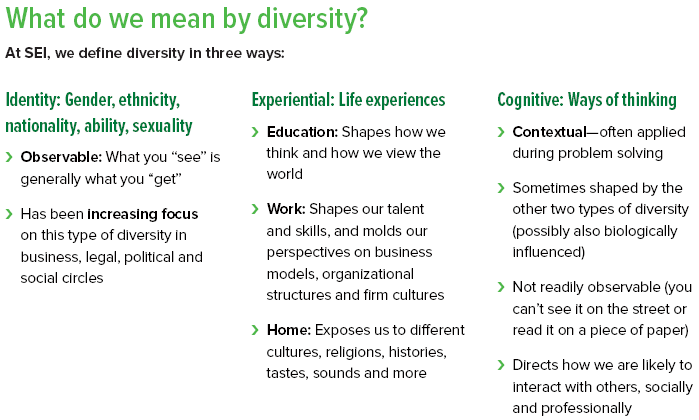

Diversity and Inclusion in SEI’s Manager Research Process

At the core of SEI’s investment offerings is the hiring and monitoring of specialist investment managers that are known for their expertise in specific markets or with specific investment styles. Our Manager Research Team evaluates and selects these managers through a combination of both qualitative and quantitative analyses—giving special consideration to team diversity.

Why consider diversity? As you’ll learn in this paper, diversity within a group has been shown over the past several decades to be a key component of effective decision-making, which is crucial to successful investment management.

It is commonly thought that identity diversity begets cognitive diversity. After all, people with differing identities tend to have differing ways of seeing the world.

But this is not always the case.

Research by Morningstar published in 2016 showed that mixed-gender investment teams performed better than all-male investment teams1. A survey published in 2014 by Harvard Business Review found that companies across industries whose leaders exhibited at least three “identity diversity” traits and three “experiential diversity” traits out-innovated and out-performed others2. And McKinsey & Company’s 2020 research showed that companies in the top quartile for gender diversity are 15% more likely to outperform; while the top quartile of racially and ethnically diverse companies are 35% more likely to outperform3.

How we evaluate diversity at SEI

In our Manager Research team’s due-diligence process, we try to capture the many elements of diversity within an investment team using several methods:›

- Observation—evaluating the mosaic of information that we gathered and the analysis that we conducted

- Documentation—encouraging investment teams to complete evaluations, such as the Predictive Index of Gallup Strengths Assessment

- Quantitative (or computer-driven) analysis—dissecting the various inputs investment teams use to arrive at their decisions. For example, a team may apply both quantitative and fundamental inputs. In this instance, the team may share with us those scores and how they are combined.

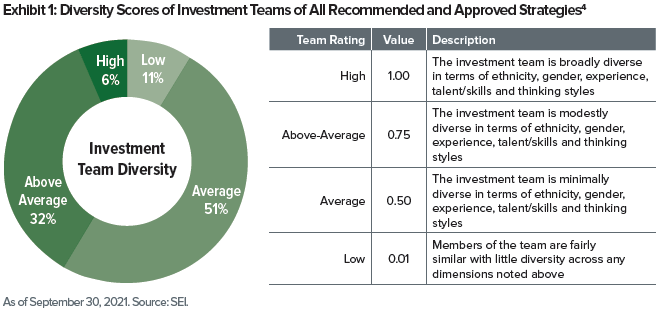

We then compile the results of these insights to assign a diversity score to each strategy’s investment team.

The diversity scores of the investment teams that manage the Recommended and Approved strategies on SEI’s Manager Research platform are shown in Exhibit 1.

Why considering diversity is important in selecting managers

All three types of diversity can offer a variety of benefits, which is why we include diversity as part of our larger manager due diligence process. However, in terms of decision-making, research indicates that cognitive diversity is the most influential

of the three5.

Uncertainty about the future requires that investment professionals gather information, and then analyze it, weigh it and make prudent judgments.

In gathering information, some people take a scholarly approach; others are perceptive and use intuitive skills to draw conclusions. The type and amount of information gathered may be determined by one’s personality (as indicated by measures such as the Predictive Index or enneagram—both of which are gender- and ethnic-neutral).

In analyzing that information, different approaches can be taken. For example, social scientist Philip Tetlock referred to the insider versus outsider view in his book Superforecasting: The Art and Science of Prediction. According to Tetlock, intelligence and knowledge are important resources in investing, but they are not sufficient; how they are used is what separates good investors from superior investors. Such knowledge and information can take two general forms: outsider and insider. Outsider knowledge refers to that intelligence that has broader applicability than the investment decision at hand. Insider knowledge refers to intelligence about the specific investment under consideration. Applied together, both views provide balance in making informed investment decisions and help combat behavioral biases.

When it comes to weighing that information to finally make an investment decision, how is it assessed? Is the minority view given credence? Is there proper devil’s advocacy and constructive debate? In all stages essential to decision-making, diversity may help shape better outcomes.

A last word

Diversity alone does not guarantee successful decision-making.

Instead, making good decisions requires careful and thoughtful input solicitation, open and transparent communication, orchestration of constructive debate and leadership to weigh disparate views into a cohesive thesis. All of these elements are evaluated in SEI’s due-diligence process, forming the mosaic of insights that shape our manager due-diligence decisions.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

Glossary of Terms

- An enneagram is a personality assessment that measures dominant behaviors and patterns across nine basic personality types.

- Fundamental input refers to basic investment research in which the fundamentals of the investment and the expectations about the future ofthose fundamentals are valued and assessed.

- The Gallup Strengths Assessment measures individual talents and patterns of thinking, feeling and behaving, to identify key strengths.

- A non-alpha mandate is one whose primary goal is not to outperform an index or whose success is not defined by relative performance alone.Examples include passive mandates, money markets, or managed volatility mandates.

- The Predictive Index is a behavioral assessment that measures workplace behaviors, or the way an individual thinks and works.

- Qualitative analysis is based on analyst research and subjective views.

- Quantitative analysis is based on computer-driven models.