Diversification: The Boring Winner

In a world where the best- and worst-performing asset classes tend to dominate the headlines, it’s easy to lose sight of the fact that a diversified investment portfolio is generally the most reliable approach for meeting long-term investment objectives. Diversification is a time-tested component of portfolio construction, especially through the lens of risk-adjusted returns in terms of Sharpe ratios. Historically, the result is a less volatile portfolio that tends to produce something close to middle-of-the-road performance year in and year out. This is in contrast to the best- and worst-performing asset classes, which often generate significant media attention despite volatility in returns and market leadership—hence the sentiment that diversification is rather boring.

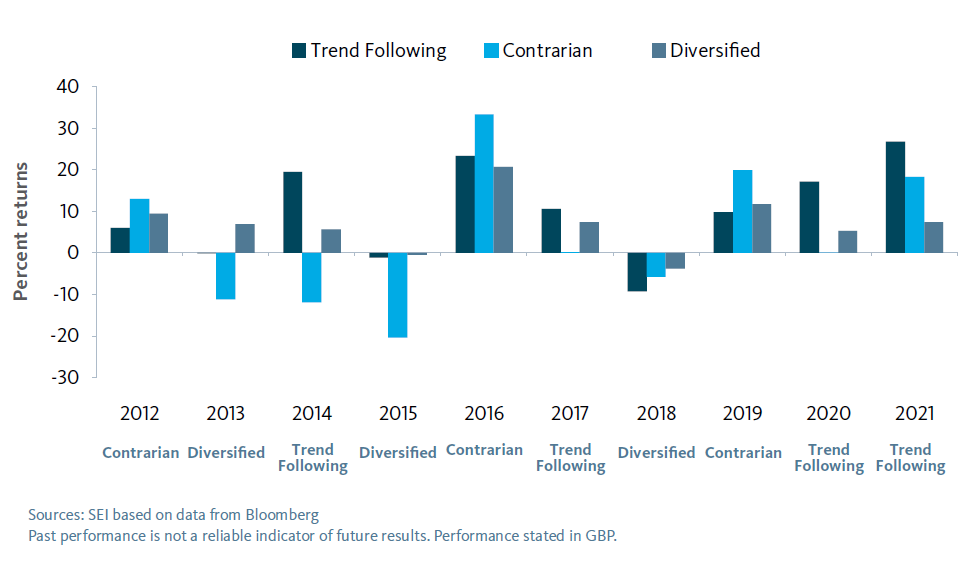

Diversification rarely wins in any given year…

By design, diversified portfolios hold a mix of asset classes, some of which outperform and some of which underperform in a given year. As a result, diversified portfolios will never beat the top-performing asset class in any given year. However, it’s notoriously difficult for investors to consistently pick top-performing asset classes. Nevertheless, to some investors, more-stable diversified strategies lack the appeal of flavour-of-the-month champions like the high-flying technology stocks or rapidly rising emerging markets. This point of view arises from some well-known cognitive and emotional biases, which we have covered at length in our series of Behavioural Finance papers.

To counter these biases, we developed a framework based on our analysis of three highly simplified investment strategy types (described below)—which has demonstrated the power of diversification.

Trend-Following Strategy: Invests in the top-performing asset class of the prior year

Contrarian Strategy: Invests in the worst-performing asset class of the prior year

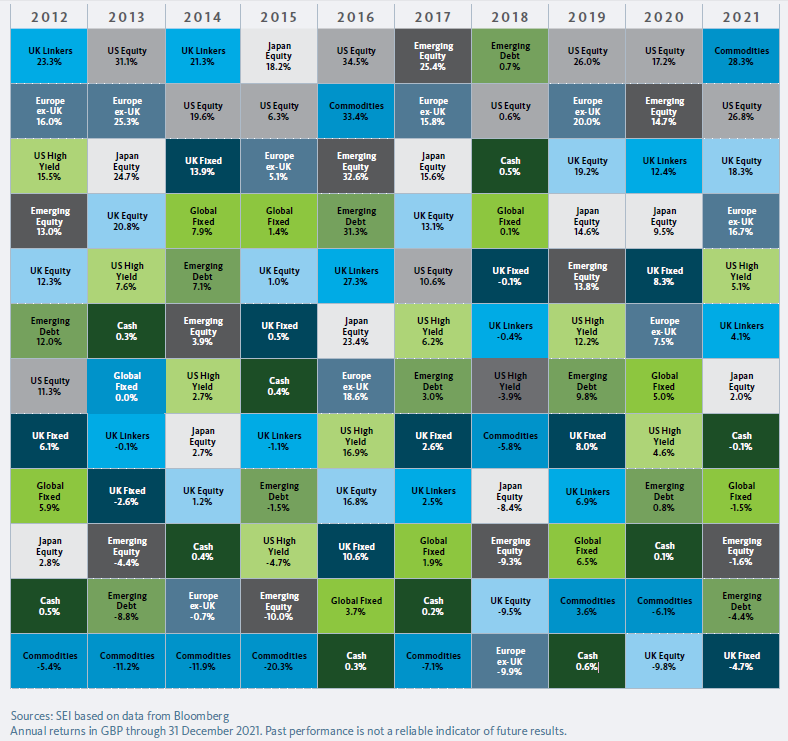

Diversified Strategy: Invests equally in all available asset classes (listed on page 3)

We found that over the last 10 years, the trend-following strategy was the top performer 40% of the time. Meanwhile, the contrarian and diversified strategies each came out on top in three of those 10 years.

… But diversification also rarely loses, and wins over time

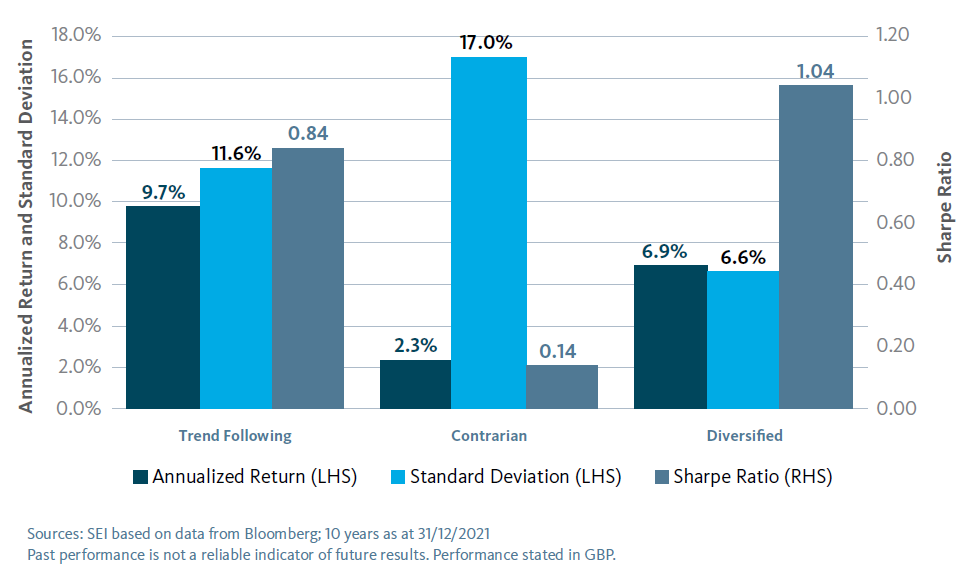

We’ve already established that a diversified strategy can’t beat the top-performing asset class in a given year; but, by definition, it can’t be the worst performer either.

In terms of risk-adjusted returns, despite rarely beating the two other strategies in a single year, the diversified approach has won, hands down, over the past decade. The contrarian strategy produced moderate returns overall, and with much higher volatility. The trend-following strategy also had relatively high volatility , but produced a strong positive return over the 10-year period. The diversified approach provided a respectable overall return with far less volatility and, as a result, much higher risk-adjusted returns.

It’s not always easy to do the right thing

This tells us that trend-following and contrarian strategies are double-edged swords; while they may offer a better chance of outperforming many asset classes and diversified portfolios, they also impose a higher probability of significantly underperforming. Meanwhile, the relative stability conferred by a diversified strategy may help to avoid significant losses while reducing the overall volatility of the investment experience. And portfolios that can avoid extreme losses while enjoying lower volatility tend to outperform in the long run. This is why we continue to preach diversification: it may seem boring, but the past 10 years of performance illustrate that diversified strategies have offered benefits that the other approaches have failed to provide

Chart disclosures

Asset-class returns are based on the same indexes as indicated below. Performance begins 1/1/2012 and continues through 31/12/2021. In each of these years, “Trend Following” uses the current-year return of the best-performing asset class of the previous year. “Contrarian” uses the current year return of the worst-performing asset class of the previous year. “Diversified” uses a return equal to the return of a portfolio of equally weighted asset-class returns in each year.

Asset Class Indices

UK Equity = FTSE UK Series All Share Index (GBP), Emerging Debt = 50/50 JPM EMBI Global Div & JPM GBI EM Global Div (GBP), US Equity = Russell 3000 Index (GBP), Emerging Equity = MSCI Emerging Markets Index (Net) (GBP), Global Fixed = Bloomberg Barclays Global Aggregate Index, Hedged (GBP), UK Fixed = ICE BofAML Sterling Broad Market Index (GBP), UK Linkers = ICE BofAML UK Gilts Inflation Linked 5+ Yrs Index (GBP), US High Yield = ICE BofAML US High Yield Constrained Index, Hedged (GBP), Japan Equity = Tokyo Stock Exchange TOPIX (GBP), Europe ex-UK = MSCI Europe ex UK Index (Net) (GBP)’ Commodities = Bloomberg Commodity Total Return Index (GBP), Cash = ICE BofAML British Pound 1-Month Deposit Bid Rate Average Index (GBP).

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document, Summary of UCITS Shareholder rights (which includes a summary of the rights that shareholders of our funds have) and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents. And you should read the terms and conditions contained in the Prospectus (including the risk factors) before making any investment decision.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the “SFO”). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices ad can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all the risks applicable to our funds, please refer to the fund’s Prospectus which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents. Please contact you fund adviser (South Africa contact details provided above) for this information

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.