A different way to look at equity diversification.

Inevitably, there will be single stocks, sectors, styles, and factors that outperform a well-diversified equity portfolio in any given year. Yet outperformance of any single investment is notoriously difficult to predict— and a diversified portfolio will tend to outperform over the long run, especially in risk-adjusted terms. This is the essence of diversification—by balancing risk across multiple sources, investors can expect less expected volatility for any given level of expected return.

Many ways to invest in equities

A wide range of strategies are available to investors in the equity market. Investors of all kinds can allocate to single stocks, sectors, styles, factors, and the list goes on. Some of these approaches are fairly simplified, such as sector investing, while some approaches are more traditional versions of equity market segmentation, such as style investing. Still other approaches are more discerning with a focus on key return drivers, like factors.

One of the longest-standing approaches is to divide a universe of stocks into “growth” and “value” styles. Practitioners of this basic segmentation tend to use only a few rules for classification and some methodologies attempt to give every stock in a specific universe of stocks a style home. But not all stocks will fully adhere to either style. In some cases, a stock can be categorized as growth, not because of its inherent growth characteristics, but because it scores negatively on the value characteristics. In fact, depending on the methodology, some stocks might be included in both growth and value classifications.

On the other hand, factor investing focuses on measuring specific characteristics that can help explain the relative price movements of a given stock universe. By this definition, there are many different factors, and not every factor is attractive or alpha generating—that is producing excess returns over a benchmark, while considering risk. Nevertheless, when it comes to SEI's investment and portfolio construction process, we primarily focus on the factors that have empirical evidence of alpha generation and/or risk reduction and those we expect to be rewarded going forward.

The exercise of segmenting stocks into various approaches is not mutually exclusive. As we noted, not every stock fits perfectly into a single category, and many stocks might be favored by multiple approaches simultaneously—a health care stock in a value style index might also be included in a momentum factor index. It is all dependent on the methodology and rules of each approach.

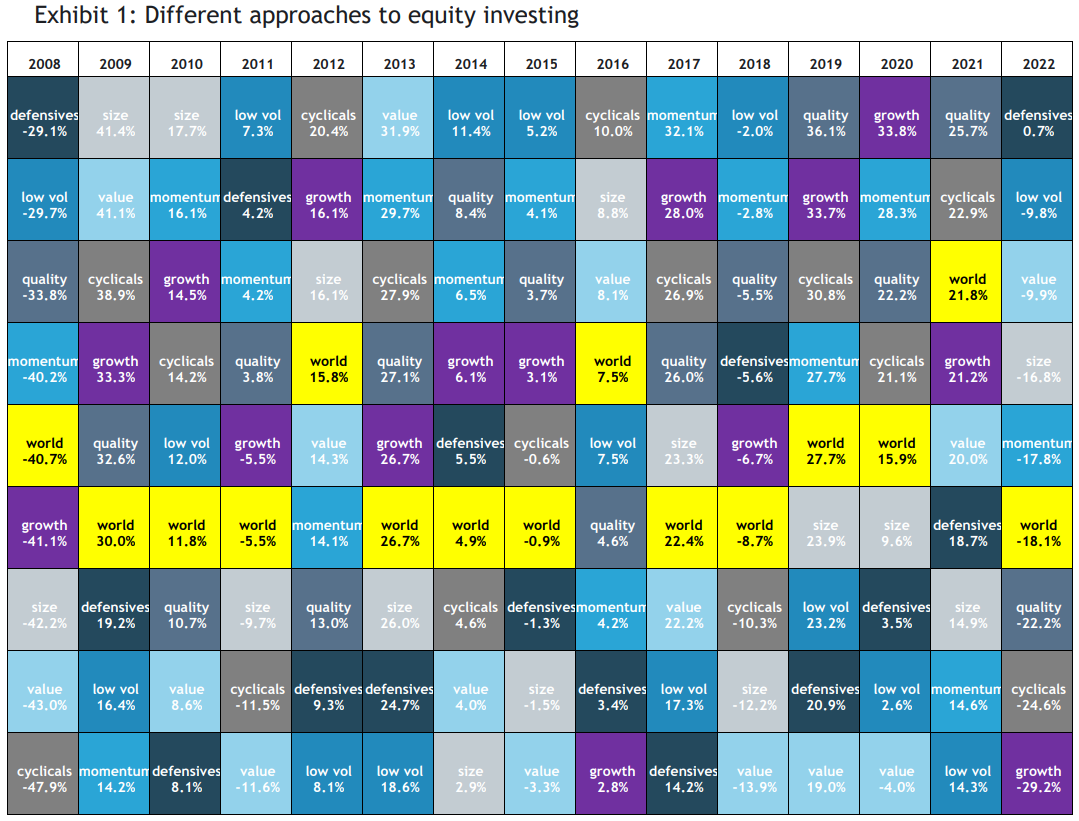

No matter which approach an equity investor prefers, it is important to understand there will be winners and losers in any given period. As demonstrated in Exhibit 1, different approaches constantly go in and out of favor—this means the volatility of any given narrowly-focused approach can be significant and potentially unnerving.

Annual performance from 1/1/2008 to 12/31/2022. Source: FactSet, MSCI, SEI. Performance is presented in total return net USD terms. Equity approach proxies: world – MSCI World Index, momentum – MSCI World Momentum Index, value – MSCI World Enhanced Value Index, quality – MSCI World Quality Index, size – MSCI World Equal Weighted Index, growth – MSCI World Growth Index, low vol – MSCI World Minimum Volatility Index, cyclicals – MSCI World Cyclical Sectors Index, defensives – MSCI World Defensive Sectors Index. Index returns are for illustrative purposes only and do not represent actual investment performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Suppose an investor 15 years ago had correctly chosen the approach that would eventually provide the highest return. How likely is it that the investor would have held that investment through the entire 15-year period? We posit: very unlikely. The considerable volatility of any single approach coupled with its relative performance variation would surely test even the strongest-willed to stick with it year in and year out. Most importantly, even if we assume a high degree of investor discipline, the chance of selecting a single approach that will perform best over a subsequent 15-year period—or any period—is very low.

Diversification helps investors deal with the volatility of any singular approach as well as the random and hard-to-predict nature of market returns. Diversification is a time-tested component of portfolio construction, especially through the lens of risk-adjusted returns (returns adjusted for the volatility of those returns) such as the Sharpe ratio. Historically, the result is a less volatile portfolio which, by definition, is unlikely to occupy either the top or the bottom of the chart in any given year. This is in contrast to the best- and worst- performers, which often generate significant media attention despite – or perhaps because of – their volatility. In contrast, the diversified approach may appear rather boring – and that is precisely what makes it valuable.

Diversification rarely wins in any given year…

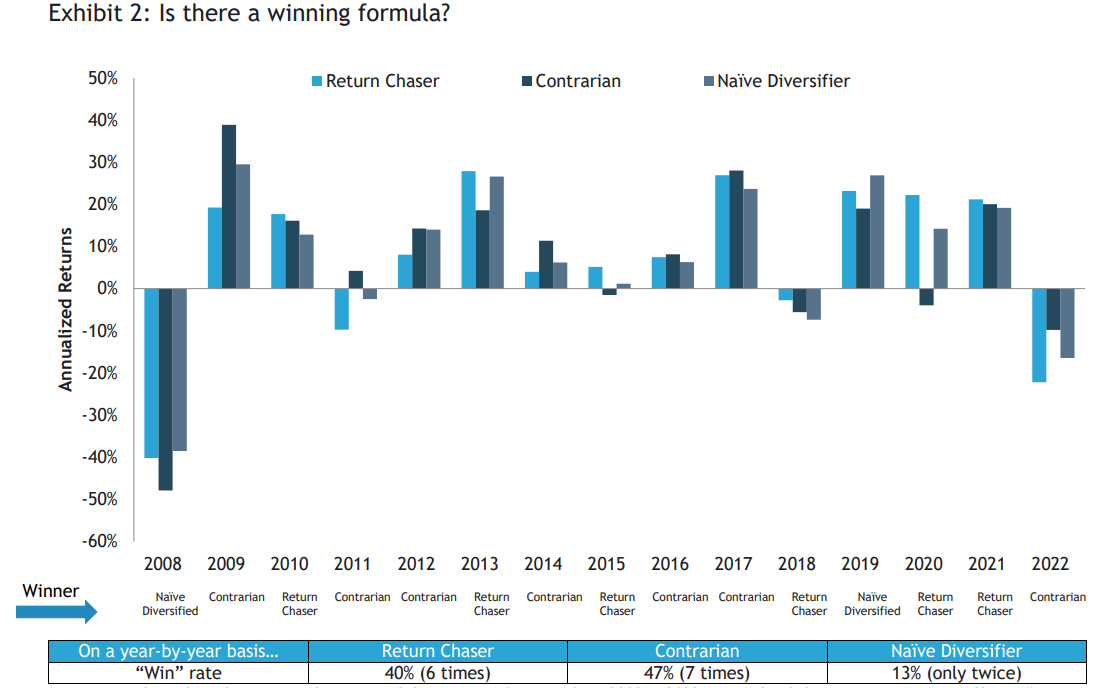

By design, SEI’s equity portfolios deliver exposure to multiple factors that have been researched and tested for significance in historically generating excess return or reducing risk. The resulting portfolios are well-diversified, but by definition a diversified equity portfolio will never beat the top-performing approach in any given year. However, it’s unlikely to be the worst-performing approach either. For some investors, the relatively-more-stable diversified approach may lack the appeal of flavor-of-the-month champions like high-flying growth stocks or defensive stocks when markets gyrate. This point of view arises from some well-known cognitive and emotional biases, which we have covered at length in our series of Behavioral Finance papers. This brings us to the “how” investment strategies are implemented. Take, for example, a few highly simplified types of investors:

- Return-Chaser Strategy: Invests in the top-performing approach of the prior year

- Contrarian Strategy: Invests in the worst-performing approach of the prior year

- Diversified Strategy: Invests equally across a wide range of approach (detailed in Exhibit 2)

We found that over the last 15 calendar years through the end of 2022, the return-chaser strategy would have led the other two six times, while the contrarian strategy would have been the top performer seven times. Meanwhile, the diversified strategy would have outpaced the other two in only two of those years.

Returns are based on the same indexes as Exhibit 1. Annual returns from 2008 to 2022. In each of these years, “Return Chaser” uses the current-year return of the best-performing equity approach of the previous year. “Contrarian” uses the current-year return of the worst-performing equity approach of the previous year. “Naïve Diversifier” uses a return equal to the return of a portfolio which invests equally in all equity approaches excluding the MSCI World Index. Source: FactSet, MSCI, SEI. Index returns are for illustrative purposes only and do not represent actual investment performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

…but diversification also rarely loses, and tends to win over time

We have already established that a diversified equity strategy can’t beat its top-performing component in a given year, but, by definition, it can’t be the worst performer either. Further, with it being notoriously difficult, if not impossible, to identify top performers in advance, a diversifying, volatility-lowering approach should offer a smoother investment experience, and thus greater likelihood of long-term success.

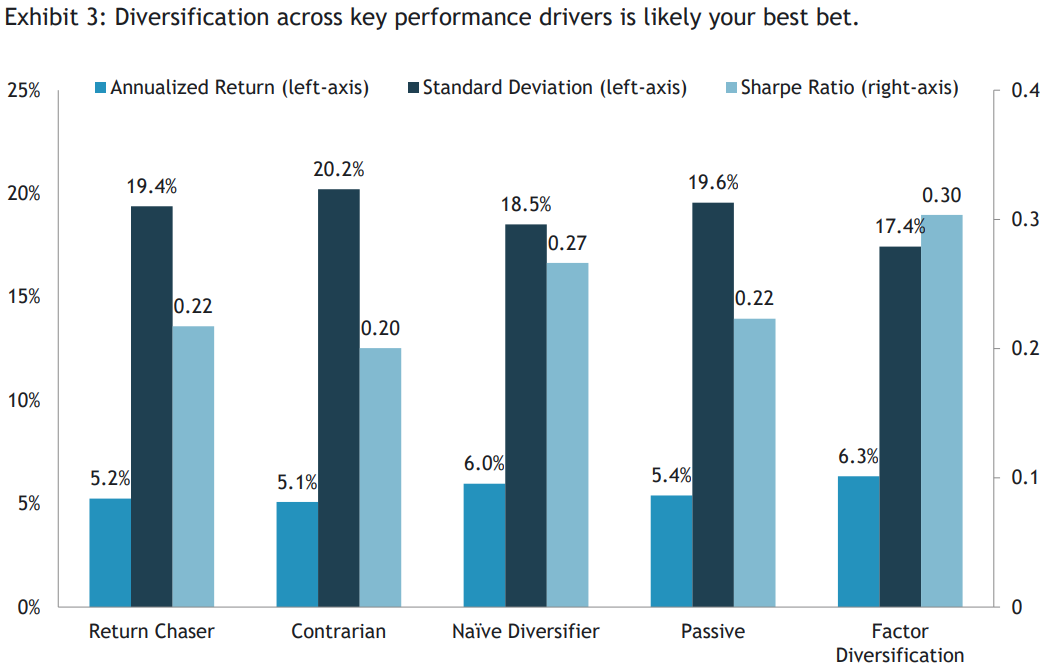

Despite rarely beating the other two hypothetical strategies in a single year, the diversified strategy would have produced the highest risk-adjusted return over the past 15 years (Exhibit 3). While the return-chaser and contrarian strategies would have produced positive returns overall, they would have trailed the diversified strategy and with much greater volatility. The diversified strategy would have provided a better overall return with far less volatility and, as a result, a more attractive risk-adjusted return.

This tells us that narrow strategies like the hypothetical return-chaser and contrarian strategies are double-edged swords: while they offer a chance at outperforming, they also offer a higher probability of underperforming long-term and higher expected volatility. With a wider distribution of potential outcomes, these strategies are also more likely to elicit emotional responses and irrational behavior in making future investment decisions.

Meanwhile, diversification offers mathematical and practical benefits to investors. The relative stability conferred by a diversified strategy may help to cushion against severe losses while reducing the overall volatility of the investment experience. By reducing the probability of extreme outcomes, diversification can offer investors greater confidence in achieving their financial goals. Additionally, a diversified strategy may also help investors to remain invested through difficult environments and to curb poor and otherwise costly investing behaviors. This is why we continue to preach diversification.

You can do better than naïve diversification

The hypothetical strategies in Exhibit 2 are purposefully oversimplified in order to demonstrate the virtues of diversification. In the real world, we believe you can do even better than naively diversifying across a wide range of equity approaches. Consider two additional hypothetical investment strategies:

- Passive: Invests in a market-cap weighted index.

- Factor Diversifier: Invests equally in four factor approaches (Momentum, Quality, Value, and Low Volatility) that serve as generic representations of what SEI believes are long-term return drivers.

Annualized returns, standard deviations, and Sharpe Ratios measured from 1/1/2008 to 12/31/2022. At the start of each year, the hypothetical Return Chaser invests 100% in the best-performing equity approach of the prior year (quality in 2022), the hypothetical Contrarian invests 100% in the worst-performing equity approach of the prior year (low vol in 2022), the Naïve Diversifier, or 1/N strategy, invests equally in all equity approaches excluding the MSCI World Index, the Passive invests 100% in the MSCI World Index, and the Factor Diversifier invests equally in MSCI World Enhanced Value, MSCI World Momentum, MSCI World Quality, and MSCI World Minimum Volatility. The cash return used for the calculation of Sharpe Ratios is equal to the return of the ICE BofA US Dollar 3-Month Deposit Offered Rate Constant Maturity Index. Source: FactSet, MSCI, SEI. Index returns are for illustrative purposes only and do not represent actual investment performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

While the equal-weight of the four factor indexes is not meant to precisely reflect any particular fund or strategy, it serves to generalize our core philosophy of constructing equity portfolios with a focus on proven excess return and risk-reduction drivers and maintaining diversification and discipline through various market environments. We demonstrate in Exhibit 3 that by focusing a strategy on just those key factors, investors have historically been able to both increase returns and reduce volatility relative to more naive approaches.

A final thought

What you choose to invest in is important. The equity market has been and continues to be segmented for investors in a variety of ways and there is an abundance of products targeting those segments. We believe investors are better served by allocating to proven return drivers.

Equally important is the combination and ongoing management of those drivers. While investing in a singular approach or a concentrated strategy might offer the chance for outsized returns, it increases the potential for significantly poor outcomes as well. This increased relative performance variation is more likely to introduce emotions or irrational behaviors into future investment decisions. Diversification can help investors to stay invested and to quell their emotional responses to market events. This is a real-world, practical benefit for investors as they are much more likely to experience a smoother ride and remain invested in their journey to meet their investment goals. In equity markets and across the broader portfolio, we believe investors are better served by allocating to diversified strategies.

Important information

Diversification may not protect against market risk. There is no assurance the goals of the strategies discussed will be met.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. Diversification may not protect against market risk.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.