Debt ceiling Q&A.

Political brinksmanship is back in full force, thanks to the U.S. debt ceiling. While most observers expect some sort of deal (or series of deals) that will allow the Treasury to avoid a default, missteps are possible. While it’s anyone’s guess how the details of such an event would unfold, it poses multiple risks to economies and investors.

What is the debt ceiling?

The U.S. debt ceiling, which dates back to legislation passed in 1917, sets a Congressionally-determined limit on the total amount of federal debt outstanding. When the U.S. Treasury’s outstanding debt approaches the current limit, it requires Congress to raise that limit in order to clear space for further debt issuance. In recent decades, what used to be a fairly mechanical exercise has become a convenient negotiating lever if not an outright political cudgel.

Why is it a concern?

While past debt ceiling episodes have ultimately been resolved, the 21st century-habit of taking them down to the wire creates unwelcome uncertainty, not just for the U.S. Treasury market but for financial markets in general, as well as economic agents that depend on payments from the federal government, such as pensioners and contractors. The actual “x date” for running into the debt ceiling is always hard to pin down, as the Treasury is able to take certain steps to postpone the day of reckoning, and quarterly tax collections can help replenish the government’s available funds. Unfortunately, federal tax collections were disappointing in April 2023. This was attributable in large part to the fact that taxpayers in California have until October 2023 to pay remaining liabilities from 2022 and the first three quarters of 2023 as a result of federal weather-related disaster declarations.1 Treasury Secretary Janet Yellen has warned that the U.S. could begin missing financial obligations in early June,

while prevailing consensus holds that the x date could occur sometime between then and late summer. President Biden, House Speaker McCarthy and other Congressional leaders have begun to discuss a resolution to the impasse.

While there’s some uncertainty around how a default would be managed. There’s no denying that it would have significant and potentially severe effects. These range from missed payments to Social Security beneficiaries, Medicare providers, military service members and other federal employees, contractors, etc. to missed interest and principal payments to holders of Treasury securities. There’s also some disagreement over how quickly the most negative effects might take hold. There is near-universal agreement that a default would constitute a severe policy error (perhaps all the more so because, unlike a typical government default, this could have been avoided). A down-to-the-wire episode or worse is also likely to aggravate concerns about the state of the U.S. government’s full faith and credit and the trustworthiness of its financial obligations.

Is it different this time?

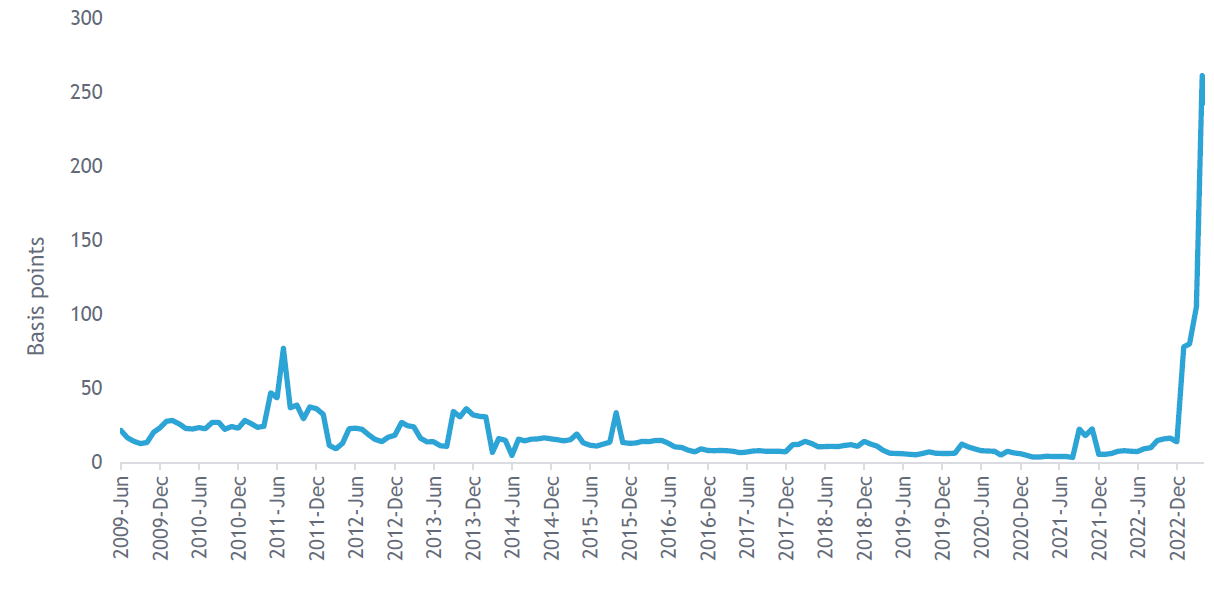

If U.S. political dysfunction seemed high in the 2011 and 2013 debt ceiling episodes, it’s even worse today, and markets seem to be expressing a greater degree of concern this time around. For example, yields on Treasury securities maturing this summer have varied quite a bit by maturity, reflecting varying degrees of confidence in whether holders will be made whole on schedule. The cost to insure against a Treasury default has also risen well above levels seen in prior debt ceiling episodes, as shown in Exhibit 1.2

Month-end cost for six-month U.S. Credit Default Swaps (CDS) from June 2009 through April 2023 and including closing value on May 3, 2023. May 3 value of 243 implies CDS holders were paying $243 to insure each $10,000 of Treasury securities. Source: Bloomberg.

What could it mean for investors?

With only a small number of similar episodes in U.S. history, it’s anyone’s guess how various asset classes will perform as this ongoing drama unfolds. It’s reasonable to assume a default would cause varying degrees of risk aversion across many financial markets, and that this could intensify the more remote a timely resolution appears to be. While it appears little was resolved in the May 9 meeting between Speaker McCarthy and President Biden, perhaps investors can take some comfort in the assumption that most politicians are fully aware of the gravity of the situation. As SEI’s Chief Markets Strategist Jim Solloway recently quipped, “This isn’t the Cuban Missile Crisis. All parties will be in constant contact with each other and everyone will be aware of each party’s needs and red lines. House Speaker McCarthy could find his leadership in a tenuous position if a compromise upsets enough members of his caucus.”

While it’s always risky to think “this time is different,” there are some other unique features to the current standoff, both positive and negative. Encouragingly, the U.S. labor market was still quite healthy as of April, whereas in 2011 and 2013 unemployment remained well above its pre-global financial crisis level. Among potential concerns, there’s been persistent pressure on bank reserves since the Fed started tightening policy, due to quantitative tightening (the Fed shrinking the size of its asset holdings) and competition from short-term, non-bank alternatives (such as money market funds) offering higher yields. If and when the debt ceiling is resolved, even temporarily, the Treasury is likely to rebuild its cash holdings, a dynamic that could cause bank reserves to fall further, potentially exacerbating the stresses that have been affecting U.S. regional banks.3 Of course, this assumes no further policy measures are taken to ease the funding and balance sheet pressures banks have been experiencing.

While predictions about the future are often wrong, it seems safe to say the debt ceiling drama could get even more dramatic. A diversified portfolio with appropriate expected risk characteristics remains appropriate in our view.

Glossary

Alternatives: An investment that is not one of the three traditional asset types (stocks, bonds and cash). Alternative investment strategies typically operate in private, unlisted markets, or have the ability to use leverage, shorting, and active risk management in pursuit of returns that are lowly correlated with traditional asset types.

Asset classes: A group of securities that share similar characteristics and behave similarly in the marketplace. The most common asset classes are stocks, bonds and cash equivalents. Asset classes are generally governed by the same rules and regulations.

Balance sheet: A financial statement that reports assets, liabilities, equity. It provides a snapshot of an entities financials (e.g. what it owns, and what it owes).

Credit Default Swaps: A financial derivative instrument that allows an investor to swap or offset their credit risk with that of another investor.

Debt Issuance: An approach used by both the government and public companies to raise funds by selling bonds to external investors.

Treasury securities: Often simply called Treasuries, are debt obligations issued by the United States Government and secured by the full faith and credit (the power to tax and borrow) of the United States.

Quantitative tightening: Policies taken by a central bank to shrink its monetary reserves by either selling government bonds or letting them mature. This effectively removes money from financial markets.

Yield: Annual percentage rate of return on capital. The dividend or interest paid by a company expressed as a percentage of the current price.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.