COVID-19 Recovery: Does the Black Swan’s Flight Path Run Through China?

Does the Black Swan’s Flight Path Run Through China?

- The COVID-19 crisis has been a catastrophic “Black Swan” event that caused an exogenous shock to global markets.

- The financial pain and human toll has been very real, but we encourage investors to remain calm and patient.

- We’re starting to see improvement in China and it’s not unreasonable to believe that western countries can follow a similar virus-containment path and start to recover economically. (Statements as of 24 March 2020.)

As of 24 March 2020, these are our thoughts. With that said, markets are moving quickly and our perspective may evolve with them.

We often talk about the potential of catastrophic “Black Swan” events that have the power to completely derail financial markets. Sometimes those events are largely contained within financial markets—as was the case in 2008. Other times they are exogenous shocks—as was the case with the 9/11 terrorist attacks. The current COVID-19 crisis certainly counts as an exogenous black swan.

Financial Pain is Real, but be Patient

The pain in financial markets is palpable. We have seen bigger one day declines—“Black Monday” on 19 October 1987 (measured by the S&P 500 Index)—and we’ve seen numerous declines exceeding these total current losses. But we’ve never seen declines of this magnitude, over this short a time period. This, of course, engenders strong feelings in investors with many feeling the urge toward “loss aversion.”

While it may seem like a great idea to sell now and avoid further losses, this would create another problem of when to buy again to participate in the gains that have always historically followed these types of losses. If you’re an SEI client you know that we always preach against the pitfalls of market timing. In fact, with the losses we’ve suffered during the COVID-19 crisis, we’re probably closer to the bottom then the market top. And the closer we are to the bottom, the closer we are to the possibility of a sustained market rally. As SEI’s own Jim Solloway recently and colorfully put it, “I believe we’re more likely to see a face-ripping rally than another 30% decline.”

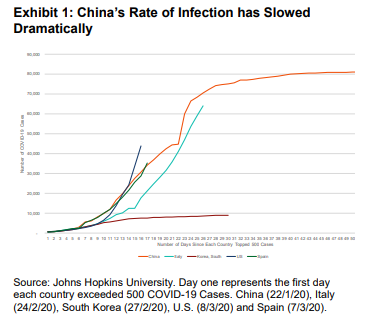

Now, it’s fair for investors to wonder how we can be optimistic about a rally when credit markets have all but seized up at the same time oil and equity markets tumble amid massively volatile price swings. But we’ve seen thorough action on the monetary front from central banks that provides significant support across the range of credit markets, and we’re now starting to see a massive fiscal response in the form of government legislation. Perhaps, though, the most important change we are seeing is in the infection rates of the COVID-19 virus (see Exhibit 1) and what comes after those infections start to decline in countries like China.

The West Begins the Virus Fight

The Western world, including the U.S. and Europe, are surely in the early stages of combating COVID-19 and will see much higher numbers of infections, and unfortunately higher corresponding death tolls.

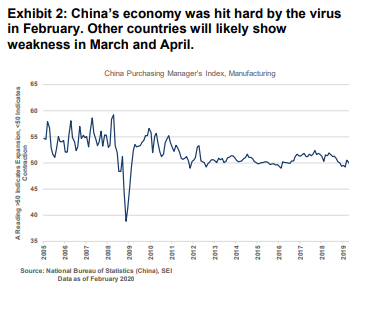

However, we can look to China for clues about what comes next. As the epicenter for the disease, China is much further along in this brutal fight. Early indicators have shown Chinese economic activity plunged into recessionary territory (see Exhibit 2) as the country was forced to take draconian actions to stem the infection rate.

Similar situations are beginning to take shape in the West, although quarantines and lockdowns are being imposed less stringently than in China. After taking dramatic action, China has seen its infection rate slow dramatically and economic activity has begun to come back as the situation improved. It seems likely that the West may follow a similar course if appropriate actions are taken, with Italy serving as a cautionary tale.

China is Recovering

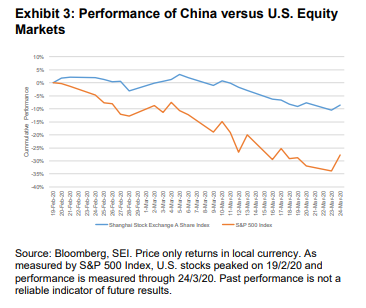

While growth in much of the developed world is grinding to a halt, China seems to be revving back up. China has been the world’s growth engine for a while now, so it’s not unreasonable to think that a return to growth there can help stave off some of the impacts of tightening conditions elsewhere. It’s difficult to get timely and accurate data on the Chinese economy, but by all accounts the situation seem to be improving. On 1 March, about five weeks after massive quarantine efforts started, China reported that over 90% of its state-owned firms were back to business (per South China Morning Post). Smaller firms, albeit, appear to be operating at a lower capacity. On a more anecdotal level, we saw Apple reopen all 42 of its stores in mainland China on 13 March, even as it maintained indefinite closures at all its stores outside of China.

SEI’s John Lau, Portfolio Manager for Asian and Emerging-Markets Equities, has a closer view from our Hong Kong office. He notes the situation is akin to a mosaic: you put little snippets of information together to create a full picture. While the situation is far from normal for both retail and manufacturing, the general consensus is that it’s getting better fairly quickly. If the rest of the world follows China’s path, the coming global recession could potentially be relatively short.

Our View

To reiterate, this has been painful. The human toll, along with the destruction of value and demand, have all been very real. At least in terms of value destruction, however, we believe that we’re closer to a rally off the bottom than another 30% drop. As always, we encourage investors to review their goals and practice disciplined, globally diversified investing. These words are especially true in times of crisis.

Important Information

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.