China’s Local Bond Market Goes Global

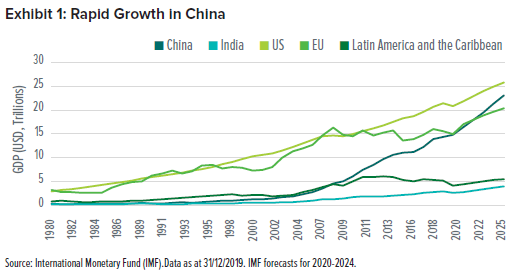

China has made a rapid ascent to become the one of the largest global economies as measured by gross domestic product (GDP). The country is forecast to surpass the size of the entire European Union in 2020 or 2021, and to reduce the gap between itself and the US to $2 trillion by 2025 given China’s higher growth rates. While classified as an emerging economy, its size eclipses any other emerging market and most other regions.

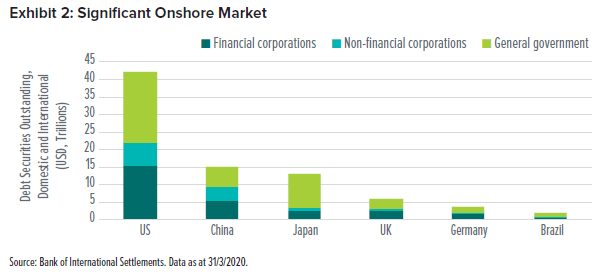

China’s debt market is currently around $15 trillion, slightly less than one-third of the size of the debt market in the US. More than $13 trillion of public Chinese debt securities are onshore, issued in the local currency. Despite the market’s large size, however, local-currency-denominated Chinese bonds have only recently seen a significant increase in foreign ownership and begun to be included in major global bond indexes. It is this large onshore market that has been historically difficult to access.

Exhibit 2 charts the value of domestic (local currency) and international (hard currency) outstanding debt.

It is noteworthy that the size of outstanding debt in China equates to about the size of the entire Chinese economy. Debt sustainability must be discussed from a multitude of angles, although the size of debt relative to the size of the Chinese economy is not concerning by itself. At the issuer level, pockets across corporate and state-owned sectors will have varying challenges and tailwinds, presenting opportunities where we believe active management will likely be best suited.

Accessing the local market

Operating under a quota system, investors have historically had to apply for the ability to trade Chinese debt as a Qualified Foreign Institutional Investor or RMB Qualified Foreign Institutional Investor. The Chinese government’s 1997 introduction of the China Interbank Bond Market (which required commercial banks to move bond trading to an electronic trading system) and the 2017 launch of Bond Connect (a platform that enables investors from China to trade in foreign bond markets and enables foreign investors to access China’s bond market) avoid several of the operational barriers, remove the quota limits and help improve access to liquidity for trading onshore Chinese fixed-income instruments.

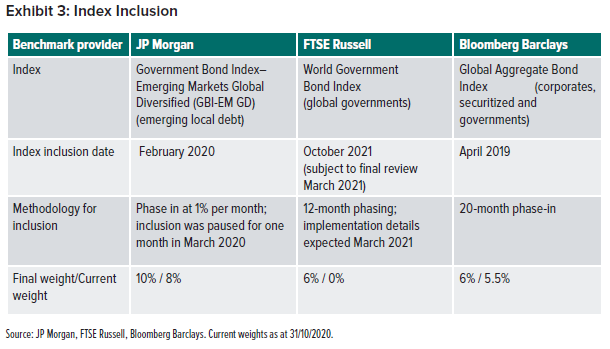

Bond Connect helps to bring a greater alignment for best trading practices typically required by foreign investors. Block trading, which was already available to onshore foreign investors, became accessible to offshore foreign investors in 20182. The Chinese government also removed a 20% repatriation cap and cancelled its three-month lock-up period in 20183. In 2019, a less frequent auction schedule for new benchmark bonds (important for ease of inclusion to bond indexes) was adopted, and Irish regulators approved access to Bond Connect for UCITS funds4. The lifting of these restrictions has improved the transparency and liquidity of the onshore bond market, subsequently attracting the confidence of major index providers to begin including them in their benchmarks. The primary indexes commonly used as bond portfolio benchmarks are shown in Exhibit 3.

The first major benchmark to include Chinese local-currency bonds was the Bloomberg Barclays Global Aggregate Index, which began a 20-month phased inclusion of government and policy bank securities in April 2019. It was originally projected that Chinese securities would represent around 6% of the more than $54 trillion index5; and appeared to be heading toward that level as of October 31, 2020, with a weight of 5.5%. The phase-in is scheduled to be complete at the end of November.

JP Morgan began adding Chinese government bonds to its indexes—including the GBI-EM GD index, which SEI uses as a benchmark for its local-currency emerging-market debt sub-advisors in our SGMF Emerging Market Debt Fund—in a 10-month phased inclusion beginning February 2020. Bonds entering the GBI-EM GD index were originally expected to have an average yield of 3.13% and average duration of 5.19 years as of October 31, 20206. Inclusion was projected to lower the index yield by 18 basis points but have no material impact on duration7. At full implementation by the end of 2020, China will represent 10% of the index’s market weight and give the Asia region the largest share of the total index.

Chinese Government bonds

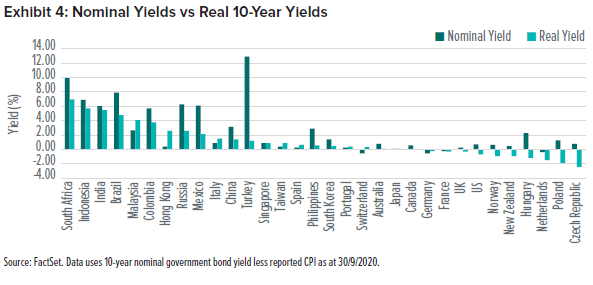

Chinese government bonds have seen a reduction in nominal yield as global bond yields have fallen. The reported yield at the end of September 2020 remained notably more positive at 3.16%8, compared to near-zero nominal yields for the majority of developed-market government bonds. We also compare the inflation-adjusted yield, known as real yield. Chinese government bonds remained marginally positive, sitting broadly in the middle of classic emerging markets and G7 countries9. This means China’s inclusion in mainstream FTSE Russell and Bloomberg Barclays indexes should likely lift the benchmark yields higher, while it will simultaneously decrease reported yields on emerging-market indexes.

Portfolio impact

Local Chinese bonds have exhibited a low correlation with major risk asset classes such as other locally-denominated emerging-market bonds, USD-denominated emerging-market bonds, global developed-market bonds, global developed-market equities, and global emerging-market equities. This low correlation is partially explained by China’s growth and inflation dynamics being driven primarily by domestic factors, whereas smaller emerging-market countries can be more influenced by global trends.

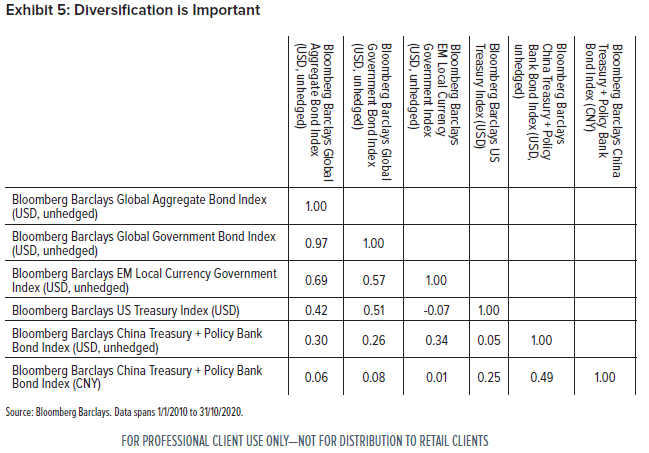

These properties of Chinese government bonds mean they typically behave as a diversifying asset to global fixed-income portfolios. The correlation matrix in Exhibit 5 looks at a 10-year history for several mainstream bond indexes. We have included the Bloomberg Barclays Treasury and Policy Bank Bond Index reported in USD, unhedged, as well as local-currency CNY. The latter removes the currency risk and effectively looks at interest-rate volatility. Whether analysing the currency component within a portfolio, or looking purely at rates, we can observe that a global investor will acquire an asset that diversifies from the current allocation.

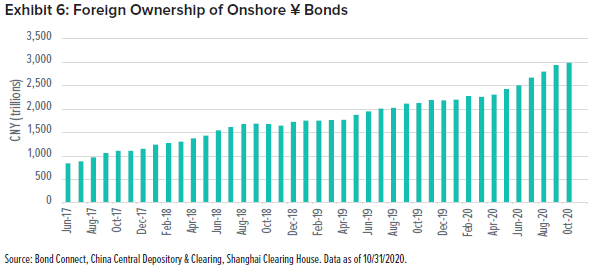

As seen in Exhibit 6, offshore holdings have more than tripled to over $450 billion (at a rate of ¥6.58/USD as at 30/11/2020) during the last three years, but foreign ownership is still relatively low in global bond portfolios, and the inclusion of CNY-denominated bonds in major global indexes only began in 2019. Learning the size of this market (but the relative lack of foreign ownership) might cause one to wonder why global bond index inclusion is only a recent phenomenon. The answer lies in the onshore bond market’s improved ease of access for foreign investors. Should liquidity and access of onshore bonds continue to gravitate toward global standards, we believe there is an almost certainty that China debt will increase its footprint in portfolios.

Closing thoughts

The exposure to currency fluctuations will be a significant driver of returns in onshore government bonds and present risks for a long-term investor. The CNY is managed by state-owned banks on behalf of the People’s Bank of China. Given possible government intervention, the CNY is less likely to freely adjust to a long-term fair value; thus, the cost to hedging this exposure may be unrewarded.

The quality of reported data has also historically been poor in comparison to that available for developed-market investors and presents a possible challenge to onshore investments in China. SEI funds will take long and short views on the currency depending on such factors as the competitiveness of the economy at a given time.

Onshore Chinese debt now qualifies for inclusion in mainstream indexes, after having improved the standards for trading local securities. As one of the largest economies in the world, this opens up a public fixed-income market in excess of $15 trillion to overseas investors. Barriers to accessing onshore investments have been reduced but remain burdensome. Here at SEI, we are operationally ready to trade onshore Chinese bonds within the SGMF Emerging Market Debt Fund and are prepared to utilise this growing bond market as it continues to develop.

Important Information

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc,and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITSRegulations. The SEI Funds are managed by SEI Investments,Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all of the risks applicable to our funds, please refer to the fund’s Prospectus. Please contact you fund adviser (South Africa contact details provided above) for this information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.