China Flexes Regulatory Muscle. What Does That Mean For Investors?

Titans of e-commerce have become the corporate equivalent of rock stars. These companies (and often their founders) are known all over the world. This fame has invited scrutiny from politicians of all stripes around the globe. Most political figures seem to agree that these online platforms present a host of perceived threats—from concerns about data privacy to disinformation distribution (even if definitions of these threats are wildly varied).

While elected leaders in many countries regularly express concerns about e-commerce companies, little actual action to address them has taken place. In the People’s Republic of China (PROC), the situation is different.

More action than talk

The Chinese government has been flexing its regulatory muscle against publically traded social media companies, ride-hailing providers, financial services firms and others. Examples of recent actions taken by the PROC include:

- Limited the number of hours players under age 18 can engage in online gaming as of August 2021.

- Imposed new regulations on companies operating “sharing” business, include ride, home and bike sharing in August 2021.

- Forced for-profit after-school tutoring (AST) companies in July to convert their businesses to non-profit entities.

- Required Tencent (a leading internet technology company) to cancel licensing deals with an array of record labels around the world in July 2021, putting pressure on the company’s entertainment businesses.

- Mandated that Ant Group restructure, adhere to more stringent regulations and capital reserve requirements, and sever its relationship with Alipay (a widely adopted digital payment app) in April 2021.

- Fined Alibaba Group (founded by Jack Ma, China’s most well-known billionaire) a record $2.75 billion in April 2021 for antitrust violations

- Summoned Ant Group and Tencent to collaborate with China’s central bank to develop and distribute a digital yuan (Digital Currency Electronic Payment, or e-CNY)—which was announced in April 2021 in arguably the most prominent state-led move toward digital currencies to date.

- Prevented Ant Group (major financial technology conglomerate and Alibaba affiliate) from following through with its anticipated initial public offering in November 2020.

Social stability over profits

Unlike economies that place a high priority on profits, the PROC operates in a communist system where social stability (maintenance of the status quo) is paramount. Emerging power centers (including corporations) fall under the political and economic primacy of the Chinese Communist Party and are likely to be regulated accordingly.

Some regulations reflect the government’s desire to deploy resources. Advances in consumer-oriented technology (such as social media and video games) have highlighted an opportunity to refocus China’s best and brightest minds, concentrating their talents on the technologies that will advance the nation’s industrial and military strength.

Other regulations are driven by more complex themes. In the fast-growing e-commerce industry with global giants such as Tencent and Alibaba and scores of smaller companies, data security has risen in importance. The PROC wants to protect the vast amount of data that firms gather as they expand their international footprints—particularly those with overseas operations in the U.S. and other nations with strained China relations.

The competitive landscape is another area that the PROC and other governments around the world believe needs to be re-balanced. Access to the global equity market has allowed China’s leading companies to pursue market share, often at the expense of profits. This has resulted in the closure of a vast number of medium- and smaller- sized companies—an outcome that, if left unchecked, could potentially undermine social stability.

Lastly, the for-profit AST industry has ballooned into a giant over the past two decades. A small number of people made billions in profits, which added to the social imbalance for hundreds of millions of Chinese citizens—a situation the government found to be intolerable.

The PROC’s stated motivation for the crackdown on for-profit AST companies was to protect working-class families. The wealth disparity in China isn’t too different from that in the U.S., according to the World Bank’s Gini coefficient (a summary measure of income inequality developed by Italian statistician and sociologist Corrado Gini), with the affluent in both countries seeking to give their children advantages not available to the less fortunate. Addressing the disparity supports equality in access to education and reduces stress on children. It also lowers the financial burden associated with raising a child, which not only helps parents but also reflects the government’s effort to encourage child birth—and stem the tide of shrinking demographics that could impede the nation’s future economic growth.

Why should investors care?

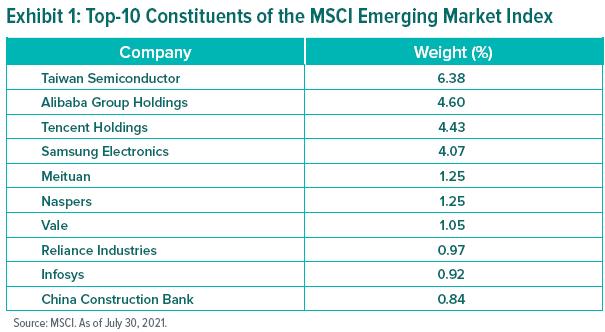

Major Chinese e-commerce companies such as Alibaba, Baidu, Didi and Tencent are big players on the world stage that offer appealing business propositions for investors seeking growth opportunities. Several firms based in China boast outsized weights in the MSCI Emerging Market Index1, as shown in Exhibit 1.

Government intervention introduces uncertainty, which can result in stock price volatility. For investors with exposure to these stocks, this can lead to declining portfolio values.

These interventions can also lead to less access to Chinese investment opportunities for investors in other countries. As it stands, many Chinese companies are only available to U.S. investors as American Depositary Receipts (ADRs), which are certificates issued by U.S. banks that primarily represent ownership in shares of foreign companies. However, given rising tensions between the U.S. and China—due to their ongoing negotiations about financials disclosure, the obscure legal structure called variable interest entity (VIE) that many Chinese companies use, and China’s data-security concerns—there may be a decline in Chinese ADRs over the next few years.

While Chinese companies will still have access to international capital through whichever exchanges host their securities, less of that capital will likely belong to U.S. investors if ADRs do in fact become unavailable.

Over the past year, sanctions introduced by the U.S. government have already promoted this effect. For instance, global index providers S&P Dow Jones Indices and FTSE Russell have removed some Chinese companies from their indexes following a U.S. executive order barring domestic investment in companies with alleged ties to China’s military.

Our view

Although the PROC’s regulatory intervention has weighed on foreign equity investors, we think it is unlikely that China’s economy itself will be severely constrained. China is a huge country with tremendous internal capital upon which to draw.

We expect most e-commerce companies will make adjustments to their business models and continue their growth strategies, both domestically and abroad. There is no apparent incentive for the Chinese government to cripple an important industry that employs hundreds of thousands of people and contributes to economic growth. However, in the near future (at least), while regulators sort out the details, we expect to see notably fewer initial public offerings from China’s e-commerce industry and potentially slower growth than previously expected.

As for the AST industry, changes will be clearly structural as Chinese President Xi Jinping wants the government to take over control of education as it relates to school-aged children. The companies in this space will be fighting for survival and seeking loopholes in regulations that may still allow them to make profits. They will be further challenged by a lack of access to foreign capital, which had helped propel their growth. In the long-run, unless the government addresses the huge demand for AST, much of the activities may eventually find their way underground.

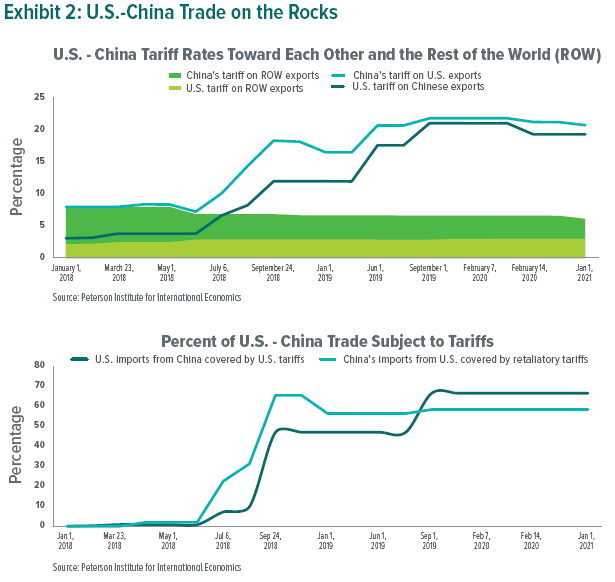

From a broader perspective, the economic relationship between China and the U.S. will no longer be characterized only by a symbiotic trade structure—in which China’s low manufacturing costs (which brought in cash and raised the standard of living) met the seemingly endless demand of U.S. consumers for inexpensive imported goods.

Rhetoric about the China-U.S. trade relationship is vastly different today compared to 2001, when China was admitted to the World Trade Organization and U.S. firms made substantial investments in Chinese factories. Current U.S. President Joe Biden issued new sanctions on China, adding to those imposed by his predecessor; China retaliated once again with its own sanctions, as the business leaders find themselves increasingly focused on supply-chain diversification. Exhibit 2 highlights the changing relationship.

The U.S.-China trade relationship now seems characterized by concerns about intellectual property theft, human-rights abuses, and competition over global influence. The EU, Great Britain and Canada have also placed sanctions on China, while Australia and China have imposed tariffs on each other over trade disputes.

Still, China is too big, too efficient and too important a manufacturer for the world to turn its back on. As such, U.S. companies have been placing strong pressure on the Biden administration to eliminate tariffs.

At the margin, we expect to see further diversification of supply chains. We think the U.S. would be wise to bring some semiconductor production back to the United States and to be more self-sufficient regarding personal protective equipment and other critical products. With that said, U.S. firms will continue to operate in China—albeit firmly under China’s rules.

China’s government, like those in other major economies, is wrestling with proper regulation of fast-growing industries like e-commerce. With a keen eye on maintaining social stability, we will not be surprised if more regulatory changes come in the future. If history is any guide, transparency, or the lack thereof, will always be an issue with investors. The timing and magnitude of changes can be abrupt, as we have witnessed.

The type risk that naturally comes with investing in such an environment is not limited to Chinese equities. Other countries that are less developed carry similar characteristics but have lower profiles since they often represent smaller portions of the equity markets. Therefore, as always, we strongly believe in a diversified investment approach to help mitigate such risks.

Our strategies

We have been underweight Chinese e-commerce and AST stocks for some time due to valuation concerns. These underweights show up in the consumer discretionary and telecommunication services sectors, even though the media often loosely refers to them as technology and education stocks.

Specifically regarding the technology sector, we are biased toward selective companies that specialize in semiconductors, software, and computer hardware because we consider the trade-off between risks and potential returns to be more attractive.

At the country level, our exposure to China is also less than that of the index, primarily through underweight positions in internet-related stocks in consumer discretionary and telecommunication services and a moderate underweight to health care.

The recent regulatory changes in China serve as a reminder that emerging-market stocks can be highly volatile. We have no doubt there will be other shocks in the future. However, the return potential and diversification benefits as a part of global investment strategy remain intact. Through our actively managed, multi-manager approach, we continue to believe we are favorably positioned given the market inefficiencies over the longer term.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

For those SEI products which employ a multi-manager structure, the manager of such products is responsible for overseeing the sub-advisers and recommending their hiring, termination and replacement. References to specific securities, if any, are provide solely to illustrate the manager’s investment advisory services and do not constitute an offer or recommendation to buy, sell or hold such securities.

There is no assurance that the objectives of any strategy or fund will be achieved or will be successful. No investment strategy, including diversification, can protect against market risk or loss. Current and future portfolio holdings are subject to risk. Not all strategies discussed may be available for your investment.

Information provided in the U.S. by SEI Investments Management Corporation, a federally registered investment adviser and wholly owned subsidiary of SEI Investments Company.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments and the use of an asset allocation service. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the “SFO”). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all the risks applicable to our funds, please refer to the fund’s Prospectus. Please contact you fund adviser (South Africa contact details provided above) for this information.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.