The Changing of Lagarde

The small club of major central bankers welcomed a familiar face into their fold on 1 November. Christine Lagarde began her tenure as President of the European Central Bank (ECB) following her nomination by the European Council in July and subsequent election by the European Parliament in September.

From the World to the Continent

As Managing Director of the International Monetary Fund (IMF) since 2011, Lagarde earned plenty of first-hand experience collaborating with heads of government and economic policymakers around the world. The IMF’s focus on facilitating global economic stability means that it has regularly been called upon to intervene at the national level as a lender of last resort for countries during periods of protracted financial strain.

Formal training in law and politics served as the foundation of Lagarde’s remarkable trajectory through the private sector and French government, ascending to lead France’s Ministry of Economic Affairs, before moving to the IMF.

As President of the ECB, however, Lagarde’s lack of deep academic grounding in economics means she will be highly dependent on the bank’s staff. Her latest act mirrors that of her US counterpart, Federal Reserve Chairman Jerome Powell: He had a similar background, as a lawyer with a successful career in business and government, and succeeded a long line of central bankers with traditional academic and professional economic backgrounds.

After the Sturm und Draghi

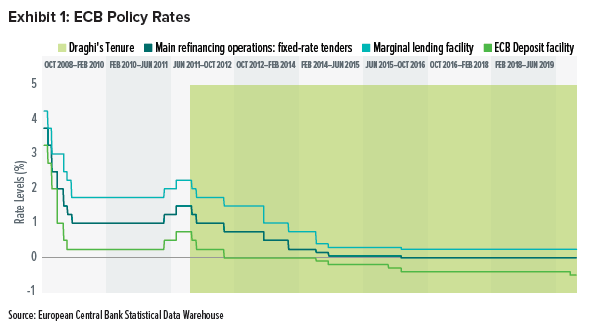

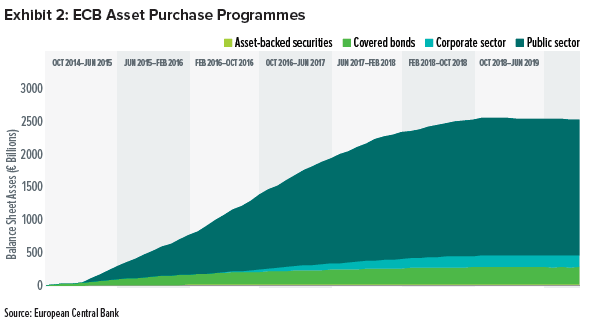

Mario Draghi—Lagarde’s predecessor—oversaw a dramatic easing of monetary policy from his perch in Frankfurt, Germany. He was elected ECB President in 2011 as swelling government budget shortfalls created a European debt crisis, stoking fears that the eurozone could splinter. Over the following years, a combination of lower interest rates, asset-purchase programmes, and bailout loans (often in coordination with the IMF) brought Europe back from the brink.

As his last act, in an effort to stimulate the once-again soft eurozone economy, Draghi introduced a new round of asset purchases (at €20 billion per month to continue indefinitely) and lowered policy rates so that banks could access cheaper lending. Economic policymakers in Germany, France and the Netherlands expressed dissatisfaction with these maneuvers and preference for a more restrained approach.

Change (Across) the Channel

Among the many factors dependent on the UK’s 12 December general election—including if, when and how it will relinquish its EU membership—the victor must appoint the successor of Bank of England (BOE) Governor Mark Carney. While sterling accounts for a much smaller share of global reserves than the euro (at about 4% and 20%, respectively, as of June 2019 according to the IMF), the UK economy is the world’s fifth largest (as measured by 2018 gross domestic product data from the World Bank).

The BOE has been nominally biased toward tighter monetary policy for a long time, but in reality has abstained from taking action out of deference to the Brexit outcome. Elevated inflation in a tight labour market would normally compel central bankers to increase interest rates, but business investment has sagged and overall economic growth has been sluggish amid the enduring Brexit-induced uncertainty.

SEI’s View

Lagarde is widely expected to retain Draghi’s accommodative approach to monetary policymaking. But there are legitimate, if uncomfortable, questions about the efficacy of these once-extraordinary measures now that they’ve been universally adopted. A growing chorus of sceptics say the ECB’s monetary policy ammunition is all but exhausted, and will soon be pushing on a string (if it’s not already doing so).

With this in mind, Lagarde—like her predecessor—has already hinted that fiscal policy needs to play a more supportive role in igniting economic growth. Investors will likely watch closely to see if she successfully convinces German policymakers, who are traditionally fiscally restrained, to increase public spending.

Important Information

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information. Data refers to past performance. Past performance is not a reliable indicator of future results.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice. This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).