A challenging road ahead for expensive stocks

Inflation is here…

Higher inflation is here. In the U.S., the Consumer Price Index (CPI) was up 5.3% for the 12 months ending August 31, 2021. When stripping out the volatile food and energy components, the core CPI shows that prices still rose 4.0% over the same period. Needless to say, this is well above the U.S. Federal Reserve’s (Fed) target of around 2% for stable inflation. Even the Fed’s preferred measure of inflation—the less widely reported Personal Consumption Expenditures Price Index (PCE), which tends to run a little lower than the CPI— was up 4.3% for the 12 months to August 31, 2021.

Some of this inflation is likely transitory due to base-level effects. Year-ago prices were significantly lower, and in some cases even deflationary, due to COVID-19-related lockdowns. The fact that August’s CPI report was slightly lower than July’s lends some credence to the notion that a portion of this inflation may well be transitory. However, price pressures due to supply-chain disruptions could easily continue into 2022 or beyond. Unprecedented economic stimulus, both monetary and fiscal, may also contribute to inflation being stickier than initially thought. Per the U.S. Bureau of Labor Statistics, we have seen significant upward wage pressure, especially for lower-income earners, although total wages are still below pre-pandemic levels as dramatically fewer people are employed versus 18 months ago. The bottom line is that inflation—when observing either the CPI or the PCE—has been below average for over a decade. We believe that trend is part of history and investors should expect higher inflation over the near- and medium-term.

…And SEI expects higher rates to follow

With inflation comes the expectation for higher interest rates. We’ve already seen this with the 10-year U.S. Treasury bond exceeding 1.7% earlier this year when an optimistic outlook for robust economic growth and inflation was more prevalent. Interest rates then settled into a lower range as optimism wavered before ticking back above 1.5% as it appears the Fed may be rethinking their ‘transitory’ view of inflation. While yields remain incredibly low from a historical perspective, they’re generally two-to-three times the lows of 2020 when the yield dipped to around 0.5% before edging up.

The Fed seems content with leaving short-term rates near zero for now, but the timeline for hikes may be shortening. While previously indicating that it would not raise rates until late 2023, the Fed has more recently signaled that the first hike could now come in early 2023 or even late 2022. Continued strong growth, employment and inflation reports could potentially shorten that timeframe even more.

How does SEI expect stocks to perform in this environment?

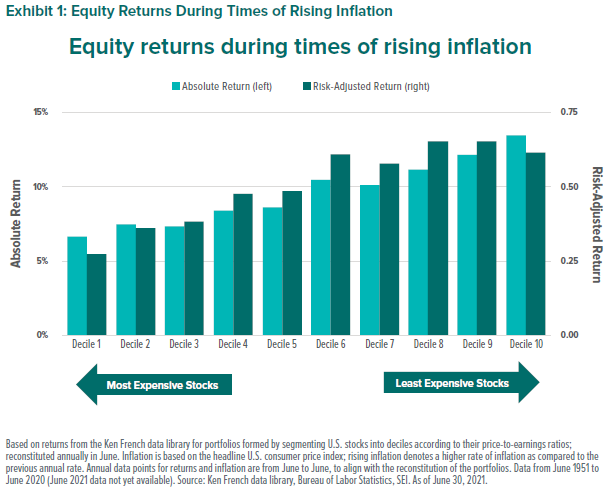

Given the extremely elevated valuations of certain segments of the stock market, it is worthwhile to examine how expensive stocks may be expected to perform versus inexpensive stocks in times of rising inflation. Looking at Exhibit 1, we can clearly see that cheaper stocks tend to perform better than expensive stocks in times of rising inflation—especially when looking at a Sharpe Ratio to adjust for risk.

At SEI, we view valuation as a significant factor in determining long-term excess returns. Therefore, while we are not exclusively value investors, our investment philosophy and process has a valuation component. Given this, and the emphasis on valuation in our current active positioning, we would expect our portfolios to perform well in an environment of rising inflation.

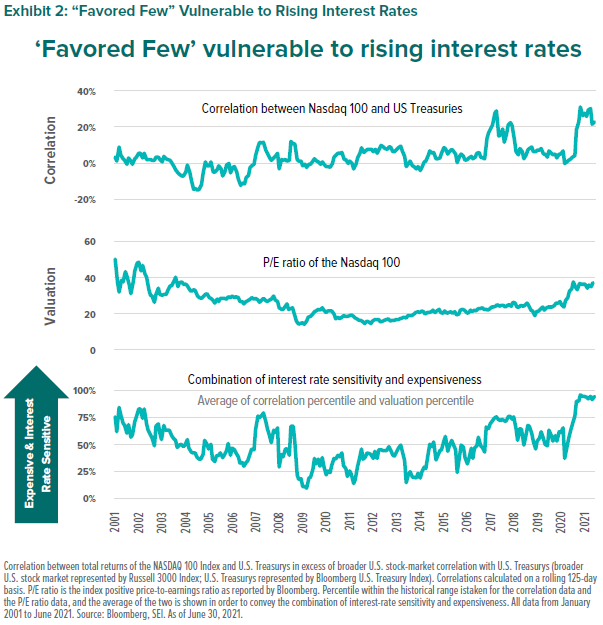

Perhaps more interesting is how the expensive “glamor stocks” of today may be particularly vulnerable to rising interest rates. Call them what you will—“the favored few,” “FAANGs,” or “big tech stocks”—they represent a group of exceptionally expensive stocks whose valuations can only be justified by lofty earnings expectations extending far into the future. Using the NASDAQ 100 Index as a proxy for these types of stocks, Exhibit 2 illustrates that they are currently more interest-rate sensitive compared to the broader equity market than they have been in the last 20 years. Exhibit 2 also shows that the NASDAQ 100 Index is historically expensive. Many investors are expecting higher future earnings to justify these values—making their valuations naturally more interest-rate sensitive. If rates begin to rise, the value of those future earnings will decrease since the value of future cash flows is determined by discounting them using prevailing interest rates. Higher discount rates obviously would lower the present value of the future cash flows and hence stock valuations. These types of stocks—more expensive than average, justified by above-average earnings growth—are often generically labeled “growth stocks” and tend to be more negatively impacted by higher interest rates as compared to the rest of the market. Rising interest rates could also dampen lofty expectations for earnings growth if overall economic growth moderates in response to higher rates.

While the expensiveness of the NASDAQ 100 Index may not be completely unique even at historically elevated levels, the combination of how expensive it is, and its current, high degree of interest-rate sensitivity is unique to today’s environment. As such, we believe this segment of the market is particularly vulnerable to rising rates going forward.

SEI’s positioning

As previously noted, SEI is not exclusively a value investor; rather we diversify across multiple strategies and drivers of excess return—with value being one of those drivers. We generally have a meaningful exposure to value, and currently that exposure is overweight in most of our equity funds. Expensive stocks appear particularly vulnerable to the changing inflation and interest-rate environment. We believe that our active positioning, underweighting the most expensive areas of the market and emphasizing value—is poised to benefit.

In our view, it is always prudent to remain well diversified across an investment portfolio; the current environment also provides the opportunity to take advantage of our expectation that value should see a significant period of outperformance versus growth. More broadly, active management may also benefit from the shifting inflation and interest-rate environments. Passive investing is historically expensive as it generally seeks to imitate a chosen index—most of which are market-capitalization weighted and therefore have increased exposure to the overpriced “favored few.” We believe that as bull markets age, passive strategies inherently suffer from high valuation and inefficient concentration of holdings. Active strategies can still invest using valuation metrics and potentially better allocate their capital than passive strategies.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

Diversification may not protect against market risk. Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance does not reflect management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments),

Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the “SFO”). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all the risks applicable to our funds, please refer to the fund’s Prospectus. Please contact you fund adviser (South Africa contact details provided above) for this information.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.